Retractable Technologies (RVP): Insider Enrichment Schemes, Operation Warp Speed Contracts, and a $54 million Technology Investment Agreeement

RVP has seen its market cap inflate $300 million on the back of an $83.7 million Operation Warp Speed contract to distribute needles for the Covid-19 vaccine program, as well as an ensuing $54 million Technology Investment Agreement “TIA,” which has been presented as an investment in the company by the government to help RVP expand capacity. But there is another story which investors have not been told or are not aware of, we will tell it below.

It appears RVP’s second largest shareholder and the sister of RVP’s Director of Operations played a role in RVP getting the aforementioned Operation Warp Speed contract. The potential related party nature of this transaction has never been disclosed.

RVP has a long history over-promising and under-delivering. RVP has never been able to make meaningful traction in the commercial market. History should inform investors as to how things could play out for RVP this time around.

RVP doesn’t own the patent for the product which makes up 85% of their revenue. Instead, they license it from their founder and CEO, paying him 5% royalties on gross sales. This has led to him extracting $57.5 million from the company since inception, while shareholders have been saddled with continual losses.

RVP’s $54 million TIA is not as advertised. We have found covered up evidence that RVP is on the hook for half of the funds that they presented as an “investment.” So far, the government has only contributed 11% of the publicly stated total. RVP saw its market cap rise $200 million in the month following the announcement of the TIA, yet only $XYZ million in investments have been made.

RVP’s 2020 numbers are a one-time thing, and we will show you why. RVP’s critical government contract will roll off, and revenue will turn sharply negative. This has happened before to RVP, and Bleecker Street Research believes history will repeat itself.

Retractable Technologies (RVP) has seen its shares rise nearly 1,500% over the last two years. This has been in part due to an $83.7 million Operation Warp Speed contract and a $54 million government “investment” which has gotten investors excited about the prospects of the previously long-struggling RVP. Why was a company that was apparently unable to fulfill an order with existing infrastructure given a critical contract to distribute needles for the U.S. vaccine roll-out? When is a $54 million investment not really a $54 million investment? How can the history of RVP’s performance with federal contracts inform us as to how this one might play out? These questions will be answered in the following sections with an uncomfortable truth in our minds: RVP has seemingly been exaggerating many claims, and the key driver of the stock over the last year may have played out not because of quality of the product or RVP’s ability to meet demand, but due to family relationships.

RVP’s History of Failure and Litigation

RVP is the creation of a former engineer named Thomas Shaw. In the late 1980’s he designed a retractable needle that would address the problem of “needle sticks” contaminating health care workers. Apparently inspired by the story of a Doctor contracting HIV from a needle stick, he invented and patented the “VanishPoint” syringe, a syringe that would automatically retract after the injection, thus preventing the spread of diseases among health care workers.

Almost from day one, RVP turned into an “over-promise, under deliver” story. The company was initially funded by $650,000 in grants from the National Institute of Health, which at the time was encouraging the U.S. production of health care supplies. RVP ended up in Little Elm, Texas (a suburb about 80 miles north of Dallas) because of a $300,000 grant from the city after RVP promised they would bring 600 jobs to fill the 22,000 square foot facility they built there.

Today the company employs 182 people in Little Elm and in 2020 RVP “used Chinese manufacturers to produce 85.2% of our products.” (2020 10-K, page 4 and page 5).

After Shaw patented the VanishPoint syringe in 1991, RVP was formed in 1995 and began to immediately try and commercialize the needle by selling it to hospitals. However, they found themselves boxed out by larger competitors. RVP’s competitors claimed it was because RVP’s needle was substantially more expensive, but RVP argued it was due to unfair competition. But it gets you to the same place, hospitals weren’t buying RVP’s needles

One example of early commercial struggles came in 1999. RVP announced soon after the passage of a California law regarding safety needle usage, that Kaiser Permanente had signed a one-year deal that allowed all Kaiser Permanente facilities to purchase RVP’s VanishPoint syringe.

According to a Dallas Magazine article, the deal was a disaster for RVP.

“Before the year was up, however, Kaiser was complaining about the Little Elm’s company’s [RVP] reliability as a supplier as well as the quality of the product. As a Kaiser spokesman explained later, Kaiser ordered 2,239 boxes of syringes but received only 343. There were also instances of product failure, Kaiser reported, including one in which the needle detached from the syringe and remained in the thigh of a 7-month-old baby.”

RVP disputed that version of the story, claiming that a competitor (who they would soon sue) gave Kaiser a $30 million grant for a safety needle study. Locked out or unable to sell into hospitals, RVP instead turned to the government. From a 2010 profile on RVP in “Washington Monthly”:

“[RVP] landed a number of contracts with government agencies, including the VA, that negotiated directly with vendors for supplies. Or he sold his wares to systems so small and poor that they weren’t on the GPO’s [group purchasing organization] radar – prisons, nursing homes, Indian reservations, and the like.”

While selling their wares to whoever in the government would buy them RVP would simultaneously turn to the legal system to fight their competitors, arguing that they had been unfairly boxed out from a having a fair fight. RVP would win several of these lawsuits, including one in which Becton Dickerson (BD) settled for $150 million on the eve of the trial. The first lawsuit was settled in 2004, but RVP would sue them again just three years later. In a long-running case in which the appeals would finally be settled in 2019, the courts ended up siding with BD and this time RVP was awarded no damages.

But if one is to strip out the impacts of these large settlements, a clearer picture of RVP as an operating entity emerges. It is not pretty.

Before 2020, RVP would only have two years when they generated positive free cash flow, adjusted for the impact of litigation settlements.

From 2004 through 2019 RVP would lose $98 million in normalized earnings, adjusted for litigation settlements. Without the litigation settlements, RVP would have an approximately $125 million accumulated deficit. RVP’s stock price and fundamental results reflect this reality, and shareholders historically have not been rewarded.

A Government Contract, and a Covid-19 Bailout

As shown above, 2020 was the best financial year ever for RVP. The Covid-19 pandemic created a one-time demand event for needles. Aided by the aforementioned government contract, RVP reported $83 million of revenue in 2020, and net income of $27 million. This compares to $42 million of revenue and $2 million of net income in 2019.

$32 million of their 2020 revenue came from the U.S. government, when this revenue source goes away (and it will), RVP revenue will be sharply negative. Investors either don’t realize or don’t care, but insiders sure seem to be aware.

On May 4, 2020 RVP would file an 8-K announcing they had been awarded an $83.7 million contract from the Department of Health and Human Services. On May 1, RVP had a stock price of $3.00 per share, by the end of the month shares would double to $6 per share on the back of this contract. Seen one way, an $83 million contract added $100 million in value to the company over a month. The rise would not be over.

The 8-K filed read simply:

Retractable Technologies, Inc. (“Retractable”) announces that on May 1, 2020, it was awarded a delivery order under an existing contract by the Department of Health and Human Services to supply automated retraction safety syringes. The total fixed price under the delivery order is $83,788,439.80.

No other details were provided at the time.

How did RVP win this contract? Why did a tiny Little Elm, Texas-based needle licensor win a contract so critical to the literal health of the country? Bleecker Street Research is not the only one to wonder, so has a member of the House of Representatives.

Both the Los Angeles Times and NBC News have wondered why RVP was awarded such a critical contract. Further raising eyebrows was that RVP was not the only company that won a large needle contract. A Colorado firm named Marathon Medical Corp. was awarded a $27.4 million contract with a government option to raise it to $54 million.

According to the Los Angeles Times, “Marathon has a long track record of filling substantial purchasing agreements with the Department of Veterans Affairs and other agencies,” but adding crucially that it was “never tasked with filling a federal contract larger than $3.1 million, according to a review of federal contract data.”

U.S. House of Representatives member Josh Gottheimer was quoted as in the NBC News report saying “The administration gave a multi-million contract to a business who can’t produce the necessary supplies... It’s left a lot of us scratching our heads.”

NBC News also cited Columbia University professor Irwin Redlender who expressed concern about the contracts. “Retractable and Marathon could prove to be “grossly inadequate” to respond to the challenges ahead” and that they had “very insufficient-looking manufacturing and distribution capabilities.”

Just two weeks before the Operation Warp Speed contract, RVP received a $1.36 million PPP loan to help cover payroll. Just two weeks later it was being relied upon as a critical part of the U.S. Covid-19 response. Why?

Is RVP’s second largest shareholder distributing Operation Warp Speed money? Would that inflate her own shares and is this potentially a conflict of interest?

RVP’s second largest shareholder seems to have overseen the distribution of Operation Warp Speed money, which could have potentially landed RVP the contract.

From 2005 to 2010 RVP had an “oral consulting agreement” with their current second largest shareholder. This was Lillian Salerno, who would end up attesting several SEC filings where she was listed as the “Secretary.” She continues to be involved with the company as its current second largest shareholder. But back in 2005-2007 RVP would pay MediTrade International Corporation $7,500 per month plus expenses, MediTrade International was controlled by Lillian Salerno. Prior to 2005 Salerno was being paid $16,667 per month for consulting services. (2005 10-K, page 32)

From 2005-2007 RVP would lease four office suites as well as several storage units from Mill Street Enterprises for $2,900 per month. Mill Street Enterprises was a “sole proprietorship” of Lillian Salerno. (2005 10-K, page 11)

It seemed like a family affair, Salerno’s brother is Lawrence Salerno, who according to their 2020 10-K has been employed by the company since 1995, serving as their Director of Operations since 1998. RVP and the Salerno’s seem to go together like two peas in a pod.

Lillian Salerno is still closely linked to RVP today; she is currently their second largest shareholder.

Salerno has run for the House of Representatives and been involved with Washington seemingly since leaving the company. Salerno’s LinkedIn profile currently lists her as a Senior Strategist at “LES Development,” (one might assume LES stands for Lillian E. Salerno) which “provided innovative solutions to ensure that essential supplies for a Covid-19 vaccine are manufactured in the US and while meeting an expedited timeline for successful delivery of health supplies as part of [sic] Operation Warpspeed.”

While is it unclear exactly what role LES Development had in distributing the Operation Warp Speed money, it should not be overlooked that she could have had a critical role in ensuring RVP received this money.

In large part due to this Operation Warp Speed Contract, Salerno has seen the value of her holdings in RVP rise $13.1 million since RVP was awarded the contract. And that does not include the 120,000 shares Salerno sold in November and December, around $14/ share.

Salerno is not the only insider selling. Seemingly not satisfied with his 5% royalty on gross sales, Shaw has been selling down his stake in the company throughout 2020. Entering 2020 Shaw owned 18.8 million shares in RVP. As it currently stands, Shaw owns 15.6 million shares, having sold nearly 20% of his holdings in the company in the last year. Is this fair?

CEO Paid Millions, Shareholders Pay the Price

Despite the lackluster results for shareholders, RVP has created fantastic results for insiders. RVP doesn’t own the VanishPoint syringe. Instead, they license it from Shaw, and pay him royalties on gross sales. Shaw has been paid $45.9 million on this license over RVP’s corporate life, while shareholders are stuck with losses.

RVP has a unique arrangement with their CEO. Despite their saying they ‘design, develop, manufacture, and market innovative patented safety needle devices,’ they don’t actually own the patent. Shaw does, but they license it from him. This isn’t that unusual. What is unusual is how much money Shaw has gotten from the company from this license.

So, for those keeping track at home, RVP has lost $100 million over its lifetime in losses from operations. Thomas Shaw has received $45.9 million over the same time frame.

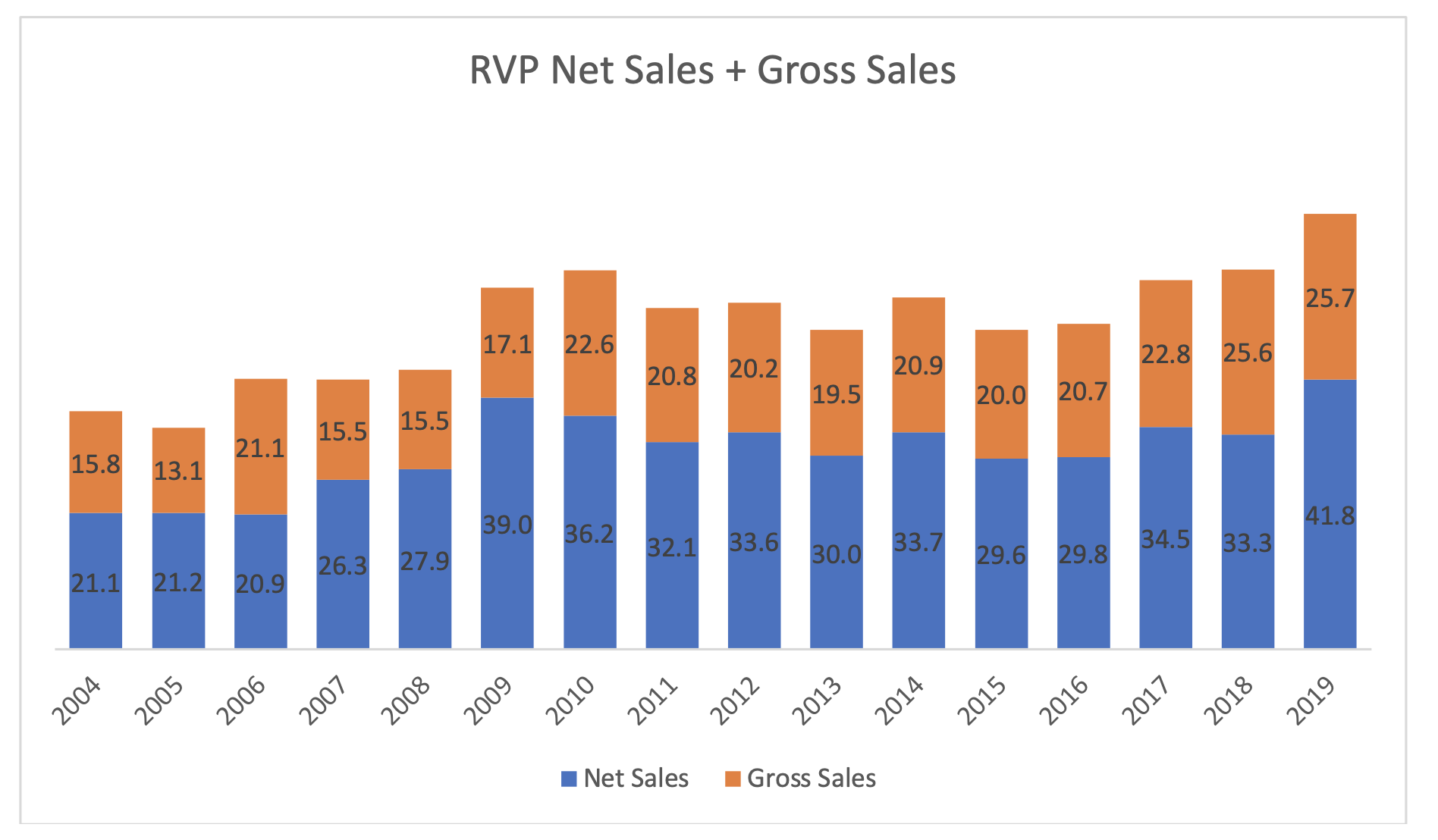

As you can see in the chart below, there is a large variance between gross and net revenue.

This has maximized the amount of money Shaw has been able to extract from the company. Since 2004 he has been paid $45.9 million under the terms of the license.

Perhaps the Government was aware of the fears expressed by those in the House of Representatives. Through the Biomedical Advanced Research and Development Authority (“BARDA”) the government invested $53.4 million in RVP through a TIA. Sometimes though a $53.4 million investment isn’t a $53.4 million investment, but only sometimes. Is this one of those times? Given that this announcement added over $225 million to RVP’s market cap, it seems like a crucial part of the bull case.

After rising 150% following the announcement of the Operation Warp Speed contract, RVP shares would fall after reporting only $1.4 million in orders from the government under the contract in the second quarter. Perhaps investors believed the past was playing out again, and RVP had said one number, only to report a much smaller number.

RVP receives a $53.4 million investment, that adds $225 million in market cap. But that $53.4 million “investment” is not what it seems to be.

On July 8, 2020, RVP filed an 8-K announcing that BARDA had invested $53.4 million into RVP through a TIA, a fairly infrequently used device used to “stimulate or support commercial firm involvement in pursuing best technologies for defense research. TIA’s are appropriate when research objectives are unlikely to be achieved using other types of contract instruments.” Over the last five years, technology investment agreements have only been used by eight public companies.

According to RVP “the principal purpose of the TIA is for Government investment to fund increasing [RVP’s] manufacturing capacity for hypodermic safety needles and corresponding syringes in response to the worldwide Covid-19 pandemic.”

They would describe the award in the 10-Q as:

“The Government award is an expenditure-type TIA, whereby the Government will make payments to the Company for the Company’s expenditures for equipment and supplies in carrying out the expansion of the Company’s domestic production.”

Nearly a full year later RVP would again seem to present the TIA as an investment, from their 8- K reporting full year 2020 financials.

“In July 2020, we entered into the Technology Investment Agreement (“TIA”) with the U.S. government for approximately $54 million in government funding for expanding our domestic production of needles and syringes. Pursuant to the terms of the TIA, we are expecting to make significant additions to our facilities which should allow us to increase domestic production.”

As previously said, in 2019 RVP had outsourced 85% production to China. So domestic expansion would obviously be necessary. But also, at least to us, it seems like the language above implies that RVP would get $54 million from the Government.

The $54 million “investment” that added $225 million to RVP’s market cap, was not really an investment. According to improperly redacted contract documents, RVP would have to pay for half of all investments made under the TIA, and so far, the government has only contributed $6.4 million to RVP.

When RVP filed their 10-Q for the third quarter on November 16, 2020, the details of the TIA contract were attached as an exhibit to their 10-Q for the third quarter of 2020. Some of the details of the contract were redacted.

In Section 8 “Cost Sharing” RVP disclosed that “the recipient must provide at least [redacted] of the costs of the project.” (Exhibit 10.1 to Q3’20 10-Q, “Cost Sharing”)

But wait, “Cost sharing” implies that the company was going to have to bear some brunt of the expansion of facilities, and not the free money that their language seemed to imply. But RVP failed to properly redact the document, and by copying the language, you can see what was redacted.

The unredacted contract:

Now you can clearly see that RVP would have to pay half of all contract costs. This doesn’t seem like free money. Perhaps this truth is why not much progress has been made by RVP in terms of expanding domestic production.

“We have substantially completed construction of new controlled environment facilities and have begun construction of additional warehousing facilities which should be completed within the second quarter of 2021. The estimated cost of the controlled environment within existing properties is $6.4 million, and construction of the new warehouse is estimated to be $5.8 million. The cost of the controlled environment will be funded by the U.S. government under the TIA, while the cost of the new warehouse will be our financial obligation.” (Source: 2020 10-K, page F-28)

Ah, now we see. Despite the TIA being touted as a $53.4 million investment, it appears the Government has only contributed $5.8 million under the deal, a mere 11% of the total that was initially touted.

Let’s say you were running a fashion brand. You buy sweaters, store them in a warehouse, and ship them out when customers want a sweater. Let’s say there was a yearlong event that created twice as much demand as normal (perhaps we had an entire year of chilly evenings). You might drastically expand warehouse space if you expected the demand to maintain elevated in the future, but if you thought the demand was a one-time thing, you wouldn’t expand your infrastructure.

RVP is either taking the latter route, or the Government doesn’t have confidence in the company. Either way, the news of the TIA helped add $225 million in market value yet has only resulted in $6.4 million in infrastructure expansion that RVP did not pay for.

This is yet another example of RVP touting a big number, and then reporting a much smaller number in the footnotes.

Past is prologue: The Swine Flu epidemic is a “one-time revenue” case study similar to the recent Covid-19 contract – investors should be aware of the significant drop in revenue and ensuing stock price collapse

Investors might want to look into what happened to RVP during the Swine Flu crisis. On August 31, 2009 RVP announced that they had been awarded a contract by the Department of Health and Human Services to supply a portion of the syringes that were expected to be used to vaccinate the U.S. population against the swine flu. After this announcement RVP would see its shares rise 150% in the ensuing months.

In their 10-Q from Q3 2009, RVP would say:

“We expect our revenues and the percentage of revenues attributable to the H1N1 program to increase significantly in the fourth quarter of 2009 and the first quarter of 2010.”

Yet it was not meant to be. When RVP reported in April 2010, they included news that the Department of Health and Human Services Contract would now roll-off in December, early than expected.

“The DHHS program, which was estimated to run from August 2009 through March 2010, ended in December 2009. Our revenue increased 142.1% in the fourth quarter principally due to the DHHS contract.”

As you can see investors initially were very excited about the short-term results, only to sell RVP shares once the contract rolled off and revenue growth turned sharply negative. Bleecker Street Research believes this is an excellent bellwether of things to come today.

As you can see, once revenue growth turned sharply negative, so did the stock price and it soon returned to pre-swine flu contract levels. We believe investors should examine RVP today with the framework of past swine flu needle contracts.

We have explored RVP’s past and current in the preceding pages. What does RVP’s future look like.

Bleecker Street Research believes that the swine flu example provides an excellent benchmark for how to think about RVP over the next 18-24 months. In 2020 the U.S. government accounted for 39% of revenue, or $32.4 million. Previously RVP said that the government orders would keep increasing through May 2020. In February of this year, the government awarded RVP an additional $54 million contract for low-dead space syringes, it is unclear why this contract was awarded when the full amount of the first contract was not yet used, but it was likely done in the government’s favor. This contract will now expire on September 14th, 2021. Bleecker Street Research believes that revenue will begin declining in Q3 or Q4 of this year and will continue into next year, likely falling 40-60% year-over-year. As RVP’s performance during the swine flu has shown, investors don’t like owning stocks that have substantially declining revenues. RVP was granted a once in a lifetime windfall, perhaps by an insider, but once on the other side the true prospects of the business will be shown. Just like when RVP won settlements in lawsuits, these one-time events don’t create good investments, and RVP will soon return to where it came from.