DS Healthcare (DSKX): Look For 60-70% Drop On Equity Offering, Accounting Problems, And Solvency Concerns

DSKX has risen by 500% in 2015 due to overly promotional press releases touting "profitability" as well as appearances on microcap promotion networks.

Auditors raised "going concern" warning and multiple weaknesses in accounting internal controls.

Company is out of cash and desperately needs to raise money in the near term.

Recent resignation of audit committee head.

Despite promotional press releases, business is stagnating and continues to lose money.

Background

Microcap stock promotions (mostly targeting retail investors) have the potential for explosive stock price appreciation. But when they finally implode, the drop can be swift and brutal. The last micro-cap stock promotion I exposed was Chanticleer Holdings (HOTR), which owns the rights to several Hooters franchises in the US and abroad. That stock had more than doubled to over $4.00 on the back of numerous promotional articles and press releases, which all ignored the company's poor underlying financial condition and prospects. Following my article on Chanticleer, the stock is now down by more than 50% and is closing in on 52-week lows. Despite its previous highs of over $4.00, the stock is likely to fall below $1.00 by year-end.

Even after I exposed this promotion, we can see numerous comments from small retail investors who refuse to believe that they have been caught up in a stock promotion. I would encourage readers to view the comments posted below my article on Chanticleer to see just how "taken in" retail investors can be with these stock promotions.

DS Healthcare (OTC:DSKX) bears many similarities to Chanticleer. Like Chanticleer, we are almost certain to see rapid declines in DSKX of 60-70%. DSKX was trading at well below $1.00 for the earlier part of 2015, and the company was quick to sell new shares at a price of just 50 cents in April. As shown below, DSKX is likely to fall back to below $1.00 by year-end based on multiple negative catalysts.

Much of this increase has been driven by an endless stream of promotional press releases as well as numerous appearances on promotional interview websites such as "Corporate Profile" and "Newtothestreet TV." Corporate Profile is a quasi-IR firm that describes itself as "a broadcasting website where Fashion meets Finance; merging two mainstream industries and creating a unique platform for investors to stay up-to-date on today's news, tips, interesting companies, and market info."

It covers mainly crummy microcap companies that appear to be in need of financing, much like DSKX.

Company Overview

DS Healthcare is a South Florida based marketing company which sells skin creams and hair growth products. DSKX sells its products through distributors in the US and abroad. Around 60% of its revenues come from international distributors. Looking into these distributors raises questions about how DSKX can be generating this revenue.

DSKX has consistently tried to portray itself as "profitable" by focusing on a made-up accounting term called adjusted EBITDAS which basically excludes nearly all expenses from the bottom line. The reality is that DSKX continues to lose money and burn cash.

Exploring the distributor issues takes some digging and will be addressed below. But first, there are many more obvious problems which show why DSKX is set for a rapid and steep decline.

DSKX Is Out of Cash And Needs Money Now, Going Concern Warning

After years of burning through money, DSKX is desperately in need of cash. As of June 30th, DS is down to less than $1 million in cash. For reference, the company burned nearly $800,000 in just the past 6 months from cash flow from operations. DSKX has a budget of over $200,000 per year for investor relations alone.

DSKX has been burning through cash since inception, and has never turned a profit, let alone been cash flow positive. Keep the fact that DSKX desperately needs cash in mind throughout the rest of the article, as that will be the key catalyst for the drop. In 2015, the company has already demonstrated that it is willing to issue new shares for as little as 50 cents. When the larger equity offering hits, it will send the stock dramatically lower.

As explicitly noted in the most recent 10-Q, "The Company cannot predict how long it will continue to incur further losses or whether it will ever achieve profitability as this is dependent upon the continued reduction of certain operating expenses, success of new and existing products and increase in overall revenue among other things. These conditions raise substantial doubt about the entity's ability to continue as a going concern." The "substantial doubt" about the company's ability to continue as a going concern was raised specifically by the company's auditor in the most recent 10-K filing.

There are two points here. First, DSKX's financial condition is so precarious that the company cannot even be assumed to continue on as a going concern. According to the auditor, there is a very high likelihood that the company could simply go out of business. Second, the company is in desperate need of cash and a highly dilutive equity offering is the only realistic alternative. Such an offering can be expected to push the share price immediately sharply lower.

Yet despite these two obvious problems, the stock price has risen as much as 500% due to DSKX's misleading press releases describing "profitability."

DSKX is a one-man show

DS Healthcare is run entirely by one person, Daniel Khesin. He acts as Chairman, CEO, CFO and Principal Accounting Officer.

Given the shortage of manpower, DSKX has repeatedly been delinquent in getting its SEC financials filed on time, resulting in "NT" status on its filings for its 10K and 10Q filings.

It has also lead to a potential Sarbanes-Oxley violation and material weaknesses, which all stem from not having enough supervision or trained people on staff to check financial transactions.

Accounting Problems and SEC Violations

Given that DSKX is a one-man show, it is also not surprising that material weaknesses could come up in their financial reporting. From DSKX's 10-K:

"As of December 31, 2014, our Chief Executive Officer and Chief Financial Officer [Same person, Daniel Khesin] concluded that our internal controls over financial reporting were not effective in providing reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with U.S. generally accepted accounting principles. We are in the process of remediating the material weaknesses, but we have not yet been able to complete our remediation efforts."

These deficiencies are in the following areas:

Not having necessary staffing to review and supervise analytical and review procedures.

Not having a sufficient number of employees with accounting and financial reporting backgrounds

Not having personnel on staff with experience with US GAAP to deal with complex transactions

Not obtaining adequate documentation to support credit card transactions

These deficiencies have lead to several issues in the past and could lead to more in the future. One example is that Mr. Khesin has potentially violated the Sarbanes-Oxley Act. Again. These potential violations arose from Mr. Khesin accepting payment for his services in 2014 that were to be payable in DSKX stock. These payments required the approval of the compensation committee beforehand, which had not reviewed the transaction. From the 10-K:

"Throughout year ended 2014 and through the three months ended March 31, 2015, Daniel Khesin, the Company's chief executive officer and chief financial officer, received in addition to base compensation, reimbursement of expenses of approximately $82,000 which were for non-business related goods and services. Furthermore, Mr. Khesin received cash payments of approximately $50,000 during 2014 that, pursuant to his executive employment agreement, were to be payable in shares of the Company's common stock at fiscal year end. While Mr. Khesin believed that these payments were received as satisfaction of certain bonus or other perquisites earned by him on a monthly basis under his employment agreement, such payments, if any, required approval of our compensation committee, which approval was not received until subsequent to the year ended December 31, 2014. Section 402 of the Sarbanes Oxley Act of 2002 prohibits advances or loans to a director or executive officer of a public company."

Deals with "Consultants" and Distributors Raise More Questions

DSKX has a history of diluting shareholders. The number of shares outstanding is up over 30% since the end of 2012, but it is the manner of this dilution that is troubling. There have been many deals where the company issues stock to "consultants" for vague services, these shares hit the market soon after they are issued. One recent example is particularly egregious.

On June 2nd, DSKX filed a S-3 announcing the registration of 200,000 shares for sale. The selling shareholder was a company called "RP Innovative Consulting." In the filing, DSKX noted that they had contracted with RP stating, "RP Consulting will provide services to the Company by introducing the Company to distributors, retailers and medical professionals, providing marketing contacts and international contacts for distribution and marketing, assistance in acquiring internet retail customers and other mutually agreed upon advisory services." DSKX entered into this agreement on May 12th, 2015. So what is strange about this?

Well, it appears RP Innovative Consulting is run out of a shack in Bay Shore, New York and was only incorporated as an LLC 7 days before the deal with DSKX was signed.

Related Party Transactions

Despite the company's dire financial condition, Mr. Khesin is clearly generous to those close to him. Over the past two years, Mr. Khesin has paid his father over $200,000 over the last two years for his consulting services.

Additionally, DSKX has lavishly paid a consultant $415,000 for outsourced COO services, reimbursements for materials purchased, and for investor relations services.

The Business? It's Not Good

All of these issues and the rapid increase in price could be justified if the business was firing on all cylinders, generating free cash flow, and growing revenues quickly. But, unfortunately for DSKX, none of that is true. Almost every aspect of what you would like to see going on in a business is going in the wrong direction.

Revenues have stagnated and the company has lost money each of the last three years.

The increase in inventory compared to revenue suggests that DSKX is having trouble selling its products.

Who Is Selling DSKX Products?

DSKX sells its products through distributors both in the US and internationally. DSKX has historically generated around 60% of its revenues from its international segments. However, looking at the international distributors raises questions about how these groups are doing business.

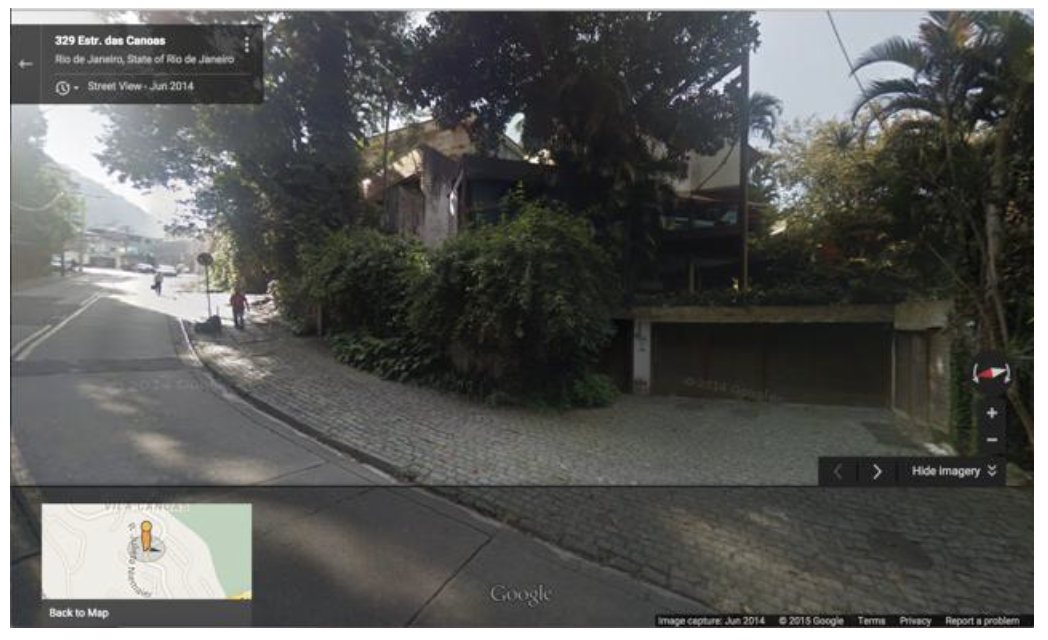

One of these distributors is a company called Gamma Investors. According to DSKX filings, Gamma Investors is located in the following dilapidated building.

Conclusion

DSKX has risen by as much as 500% this year as the company touts its supposed "profitability." The reality is that the company continues to lose money and burn cash. There is simply no reason for this stock to be trading above $1.00.

At present, the company has less than $1 million in cash on its books, even as it burned $480,000 in the first quarter alone. Again, this is a company that is out of cash and desperately needs to raise money via a stock sale.

So far in 2015, the company has only been able to raise around $200,000 from selling stock at a price of just 50 cents.

The reason that there is very little demand for the stock is that the company has received a "going concern" warning from its auditors, suggesting a high likelihood that the company will go out of business completely. These concerns are also exacerbated by the fact that DSKX is a "one man show" which is run entirely by one man filling the roles of Chairman, CEO, CFO and Principal Accounting Officer. The company suffers from multiple material weaknesses in its accounting internal controls and has repeatedly been delinquent in making its SEC filings on time. DSKX is nearly out of cash and has been promoting the stock endlessly. Investors have bitten at the promotion. But with the business now stagnating, and DSKX running out of options and in need of cash, look for the stock to drop 60-70% on an equity offering and the stagnation of the business becomes clear.

Note: I have contacted DSKX investor relations with some of the issues raised in this article and have not received a response.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.