Rocket Lab (RKLB): We Think It’s Gonna Be a Long, Long Time

Initial Disclosure: Funds managed by Bleecker Street are short Rocket Lab (RKLB). Please see the full disclosure at the end of this report.

Key Points:

Rocket Lab (RKLB) is a rocket development and space systems company that has seen shares rise 485% over the last year to a $11.2 billion valuation, propelled by investor and analyst excitement over the upcoming launch of Neutron, a medium-lift rocket that RKLB hopes will compete with SpaceX’s Falcon 9.

We believe that RKLB has materially misled investors about the likelihood that its Neutron rocket will launch in mid-2025, a timeline the company has repeatedly claimed in media interviews and on earnings calls. In fact, rocket experts we spoke to put the timeline of a rocket launch from mid-2026 to mid-2027, a one to two year delay.

Many aspects of RKLB’s Neutron program remain far behind where they need to be: from engine development, to engine and structure production, to launch pad construction, to rocket transport to the launch site, per documents we reviewed and 23 interviews with industry experts, including former Rocket Lab engineers and executives.

With a 2026 or 2027 Neutron launch, it appears RKLB won’t be able to onboard for a year or more to its most lucrative single source of potential contracts, National Security Space Launch’s (NSSL’s) Phase 3 Lane 1 program.

At the same time, Neutron’s sole announced launch contract looks to be with an unproven, questionably capitalized startup called E-Space, which two experts called a subpar customer that may run out of money or pull the launch entirely.

RKLB appears to be willing to sell Neutron launch slots well below its stated launch price of $50-$55 million, despite management’s claim that its recently announced contract was “in line” with that price.

A revenue shortfall in the face of continued cash burn is a liquidity threat for Rocket Lab, which had $504 million in the bank as of September. Three aerospace executives with rocket development experience estimated it will cost RKLB between $300-$600 million to finish and launch Neutron to profitability, meaning RKLB will need to raise money to fund Neutron and survive.

Without Neutron, RKLB’s revenue goals for space don’t add up. SpaceX took a huge bite out of the market for RKLB’s small Electron rocket by offering cheaper satellite rideshare aboard Falcon 9. Electron and Space Systems alone don’t come close to supporting the company’s current valuation.

Rocket Lab and The Space Economy

Rocket Lab was founded in 2006 by Peter Beck (now Sir Peter Beck), back when commercial space was in its infancy. Beck had a lifelong interest in rocketry and a civil engineering background. Beck’s first investor in the venture was Mark Rocket, and with a small team, Beck bootstrapped Rocket Lab, which launched its first rocket, the Atea-1, into space just three years after the company was founded.

In 2013, Rocket Lab completed its Series A in a round led by Khosla Ventures, which invested $5.5 million in the deal. Alongside the fundraise, the company headquarters moved from New Zealand to California to begin to develop the Electron rocket. Rocket Lab saw a small satellite market that was rapidly expanding, but underserved by the larger launch vehicles. Rocket Lab launched the Electron rocket for the first time in 2017, and it has succeeded 56 times since then. However, SpaceX’s Falcon 9 offers payload capacities well beyond Electron’s 300 kg at a much cheaper cost to launch under its Transporter/Bandwagon rideshare missions. And low-earth orbit (LEO) satellites are getting larger: Electron is now incapable of carrying 80% of spacecraft upmass.

In 2021, the year SpaceX launched its first rideshare mission, Rocket Lab decided to develop and launch a new rocket, Neutron, to compete with SpaceX’s near-monopoly in medium and heavy launch rockets. The reason to aim bigger is clear, since SpaceX launched roughly 86% of global upmass in 2024, whereas Rocket Lab was in 9th place among launch providers with less than .1%. Neutron is Rocket Lab’s bid to compete with the Falcon 9, a medium-lift rocket capable of delivering 13,000 kg payloads to LEO. According to Rocket Lab, Neutron will generate $55 million in revenue per launch, compared to the $5.5-$8.5 million in revenue per launch Electron has been generating.

In August 2021, Rocket Lab raised $777 million in a SPAC, using these funds primarily to help fund the development of the Neutron rocket as well as acquiring four space services companies. Over the next several years, Rocket Lab continued to launch Electron while focusing on developing Neutron.

Then, in early 2024, Rocket Lab pushed back the target first launch of the Neutron rocket to mid-2025. The company has stuck with this revised target on earnings calls and media interviews, and investors have taken it for granted.

We first began researching Rocket Lab in September 2024, when the results of a Freedom of Information Act (FOIA) request began circulating in niche space-focused online forums. We reviewed the document, which included memos from congressional offices and suggested that NASA employees considered Rocket Lab unlikely to launch Neutron in 2025, and that even 2026 was in doubt.

Rocket Lab had concluded the initial hot fire test of its Archimedes rocket engine in August, and we decided to dig in. The first analyst we spoke with, who gave the stock a buy rating, told us that “Neutron launching in mid-2025 is a sure thing” when we asked about the timeline. In the ensuing months, we reviewed dozens of federal, state,and local filings, analyzed thousands of pages of technical documentation, and spoke with 23 industry experts.

Our conclusion after this process is that the analyst community and retail investors are offside on launch expectations. We think Rocket Lab has continued to assert the mid-2025 launch date because if Rocket Lab misses this date, it will endanger Rocket Lab’s ability to obtain and fulfill lucrative National Security Space Launch (NSSL) contracts. contracts that have helped support its lofty valuation, and the company will have to come clean about 1-3 years of further development and production costs that will require a major capital raise.

We are short shares of Rocket Lab. We think that Rocket Lab will have to push back the Neutron launch date significantly in the coming months, which will mean that the company won’t be able to bid for valuable NSSL contracts. We think that the analyst community is offside not only on revenue and margin expectations, but on future Neutron CapEx requirements stemming from the delayed timeline that will amount to hundreds of millions of dollars. As Neutron development and testing drags on for years without a profit-producing launch, which we believe is likely, RKLB will have to raise equity or debt to stay afloat.

Bull Case: Rocket Lab is challenging SpaceX’s US monopoly on medium-lift launch, and the mid-2025 launch of the Neutron rocket will help revenue inflect over the next several years.

Rocket Lab pitches itself as an “end-to-end” space company. This means that, in addition to rockets, it also designs and manufactures spacecraft components for other space companies.

Rocket Lab’s Electron rocket has launched 60 times since its first launch in May 2017, making it the second most frequently launched rocket in the U.S., behind SpaceX’s Falcon 9. While undersized, the Electron rocket is a reliable launch vehicle for satellite operators with smaller payloads. Electron has delivered payloads that include a NASA orbiter, geospatial imaging satellites, and numerous academic and research projects. It has other things going for it as well: Rocket Lab has the ability to launch a satellite in mere days, and has many launch slots available.

Rocket Lab has seen revenue inflect over the last several years, both in Launch Services and in its Space Systems business, which makes satellite components.

The $777 million raised in the SPAC was for the development of the Neutron rocket, but Rocket Lab also used ~$180 million of it to acquire three companies: ASI, PSC, and SolAero, which make up the company's space systems business now.

According to the company, bullish investors, and the sell-side, Rocket Lab will soon launch its first Neutron rocket, a much larger rocket that will begin to command $55 million in revenue per launch, up from the $8.5 million the Electron rocket is currently generating per launch.

Neutron is massive for Rocket Lab’s future success. The larger rocket will allow Rocket Lab to compete for valuable NSSL contracts, amid other medium-launch contracts. Rocket Lab will launch its Neutron rocket for the first time in mid-2025, which will allow it to compete with SpaceX, Blue Origin, and ULA for valuable government launch contracts.

These launches will cause revenue to inflect, helping bring the company to cash-flow breakeven by 2026, according to one analyst with a buy rating. Between 2025 and 2026, the sell-side consensus is that Neutron will generate $50 to $250 million of revenue for Rocket Lab.

Rocket Lab, The Bear Case

Analyst A, Q3 2024 Earnings Call: “The target for the first launch is unchanged for mid-2025?”

Peter Beck: “So obviously, one test flight in the following year, three and then five and then seven, and beyond.”

Analyst B: “And then you stated that the ASPs, you're going to be pretty firm on pricing. Is that the $50 million to $55 million that you initially talked about… where things have settled maybe for these two dedicated missions?”

Peter Beck: “This contract is in-line with our previously discussed ASP for Neutron”

Contrary to what RKLB management says, Neutron appears set to miss widely on two key milestones: launching on time and profitably. SpaceX has put significant competitive pressure on Electron through its satellite rideshare service, which has put Rocket Lab in a do-or-die situation to try to get bigger. This is why Rocket Lab is coming up on $250 million plowed into Neutron development. In 2021, SpaceX began launching small satellites on rideshare missions that cost a fraction of Electron’s, elbowing into the small launch market at the expense of Electron market share, which has fallen to just .07% of upmass:

According to experts including a former Rocket Lab senior engineer, SpaceX’s move “decimated” the market for small launch and limited Rocket Lab to bespoke launches without a way to appeal to a broader orbital market, which we believe fuels the need to show unrealistic Neutron timelines.

While the company has stuck to plans to conduct a test launch of Neutron in mid-2025, with 3 commercial launches in 2026 and 5 in 2027, regulatory filings and our interviews with industry experts indicate that a first launch of Neutron isn’t possible until mid-2026 at the earliest.

Industry experts told us Rocket Lab’s timelines “are probably off by 12 to 24 months, maybe even 36 months” and “they’re probably a year and a half to two years out from flying.”

The Neutron rocket is critical to Rocket Lab’s future. “Neutron really needs to get to market, needs to be flying,” said a former Rocket Lab manager. Another former employee we spoke with said that Neutron “probably accounts for 90% of their long-term revenue over the next ten years.”

Despite all of Rocket Lab’s spending to date, experts told us the company still has hundreds of millions of dollars of costs remaining in the Neutron program until it reaches profitability. One expert said, “I think their first 5 vehicles, they’re going to cost $50-$100 million each. They’re going to get down to a recurring cost of $30-$50 million on Stage 1 and probably $3-5 million on Stage 2… They have one-time costs over 5 years that are probably approaching $400-$600 million in facilities and development until they get profitability with Neutron as a product.”

While analysts tout an annual Neutron revenue opportunity in the hundreds of millions of dollars after the initial launch, industry experts told us that the contracts for the first few missions from this kind of new-build rocket will be well under the $50-55 million advertised average selling price–including for Neutron’s already announced customer. One former Rocket Lab employee speculated revenue would be around half that, or roughly $25 million, for the first 3-5 missions. We don’t think sales from Neutron will be meaningful until 2029, at the earliest. This puts Rocket Lab in a difficult position financially. Economics of early launches are exceedingly poor, as no one wants to risk losing their satellite on the launch pad because of an unproven rocket. And yet, RKLB and sell-side analysts cling to a $55 million per launch number.

Neutron’s deeply funded competitor also made many experts wary of Rocket Lab’s prospects. “If SpaceX decides to kill Neutron, they can drop their prices on Falcon 9 and just kill it,” one former Blue Origin senior manager said. Neutron will also have to contend with higher insurance costs, estimated at 8-10% per launch versus 1-2% for SpaceX, which would turn the $55 million Neutron price tag into $60 million. Neutron, meanwhile, is only capable of sending up 57% of the payload mass that Falcon 9 can to the most desirable orbital locations.

There is a litany of schedule issues and apparent delays that add up to a significant setback for Neutron. From engine development, to qualification tests, to production, to transportation, to regulatory approvals, Neutron appears to be at least 12-18 months behind schedule.

We believe Rocket Lab is entering a very difficult period as it struggles to get Neutron out the door and fund unprofitable initial launches. As one aerospace executive remarked, “They shouldn’t be a public company, and I wouldn't want to be doing [rocket development] publicly.”

“We’re looking to try and fly the Neutron vehicle by the middle of the year, and get that first successful flight, and then the following year we’ll do another three flights, and the following year another five.”

–CEO Peter Beck, January 2025

“So we've gone to R&D, now into production mode, and we're always going to be continuing to test and improve and iterate the engine, but that's the long pole. And that's -- we pretty much got that behind us… I don't think there's any one long pole right now that would say that's really kind of a big risk factor for hitting that mid-next year kind of initial launch.

–CFO Adam Spice, December 2024

“We do expect a pickup in cash consumption in the next few quarters, owing to an expected increase in Neutron spending ahead of our mid-2025 launch”

–CFO Adam Spice, November 2024

“You saw us do that [$355 million] convertible note, and that was really to put some powder in the barrels for acquisitions. As far as Neutron goes, we don’t need to raise any capital for that program.”

–Peter Beck, October 2024

“No chance” Rocket Lab launches a Neutron rocket in 2025, according to numerous industry insiders. Key setbacks with the launch pad, engine and structure development, production facilities, and rocket transportation

“So if they’re launching in 2025, there has to be a flight vehicle, there has to be structural qualification, an engine qualification, a stage that is delivered to the launch pad months in advance for payload integration, and these steps will tell you where they’re at. These steps are, for the employees, such big steps, that you will either hear a public release or a lot of chatter when they happen, and I haven’t heard them.”

–Former Senior Executive at Firefly Aerospace

“When you see his numbers and his launch dates, it’s like, “yeah you’re not launching in 2025. You’d be lucky to get through QTP [Qualification Test Procedure] for all those systems.”

–Senior Launch Engineer at SpaceX

“For Neutron… to get to a first launch is probably no earlier than two years out. It’s complicated and it’s unlikely to reach commercial service for at least 2 to 3 years.”

–Aerospace Engineering Executive

“The original launch date they had put forward was 2024, and recently, Pete came out and said mid-2025 is more realistic. But I don’t really think that tracks with what I’ve seen in the news. I’d say the long pole things for Rocket Lab are Archimedes development and Wallops readiness. Neither of those from what I’ve seen seem like they’d be able to support a mid-2025 launch. I think there’s a lot more work to do there.”

–Former RKLB Employee

Rocket Transportation Delays Put a Launch in 2026 at Best

As part of our investigation, Bleecker Street reviewed thousands of pages of technical documents and permitting information at the local, state, and federal levels. In this review, a clear picture emerges that Rocket Lab will not be able to launch in 2025.

Below are the steps still necessary to launch Neutron in 2025, per Rocket Lab’s website. Experts we spoke to said that together, these milestones, which include structural qualification, engine qualification, vehicle integration, and wet dress rehearsal, will require 12-18 months from today to accomplish even in the absence of catastrophic setbacks. The 2025 timeline appears entirely unworkable, and 2026 is also in doubt. In the words of a former senior SpaceX executive we interviewed in February:

“Just to get a flight-ready set of engines, from where they stand today, for a first-time design, that could be 3-6 months of production, and I would add 3 months of testing onto that. And then assume they’re building the stages in parallel. Engines are probably the critical path, but once you have the full set of engines completed and installed into the stage, which is another month or two… that’s 8-12 months. Then full stage testing on both stages adds another couple months, depending on what they find, then you go to the launch site, you probably have another 2-3 months there of doing final assembly of the vehicle, pad, wet dress rehearsals, static fire, and then launch. If you sum it up… it could easily be 12-18 months away from a launch-ready state.”

“A very aggressive and miraculously successful test campaign would be about 18 months for all of this.”

–Senior Aerospace Executive

Rocket Lab’s launch facility is in Wallops, Virginia, a NASA site that also hosts Electron launches at a separate pad. Because of Neutron’s size, which is much bigger than anything currently launching from Wallops, there has been a lengthy and complex planning process about how to transport the large Neutron rocket components from where they are being constructed outside Baltimore. Complicating the back-and-forth is the fact that there is no permanent dock infrastructure on Wallops Island itself. While NASA’s Spaceport management team has a long-term plan to build a dock at Wallops, that is a 2027 and beyond plan currently. In our review, we noticed things move slowly at Wallops, with one bridge replacement taking 3 years to complete, for example.

Initially, Rocket Lab and NASA staff had settled on a direct beach landing of a barge from Baltimore. The sand dunes on the barrier would have to be flattened with earth movers, and a temporary platform erected to carry the massive rocket stages from the barge into the facility by mobile cranes. This plan had been formalized as a temporary solution in late 2023, and NASA applied for a permit from the Virginia Marine Resource Commission (VMRC) in July 2024. The permit application indicated that the three landings needed for an initial launch would occur between 1 September 2024 and 14 March 2025:

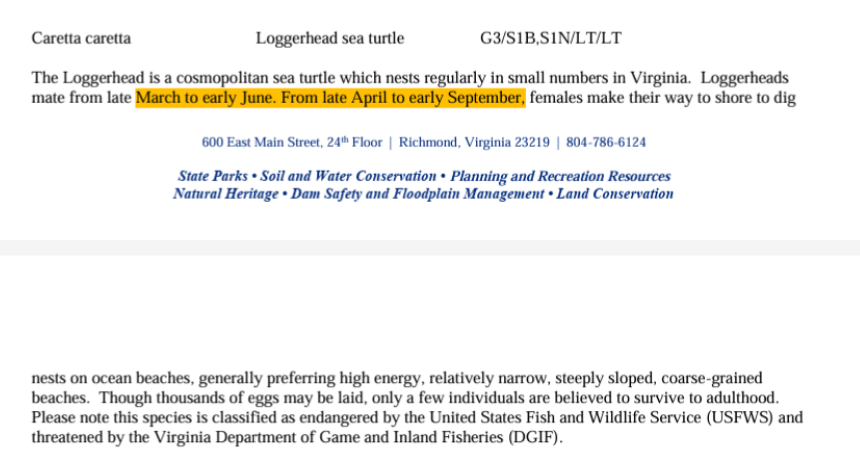

The time of year for this landing is critical because after March, disturbance of Wallops Island is strictly prohibited due to the nesting season for the loggerhead sea turtle, an endangered species protected by federal and state laws, as the state National Heritage Agency noted in subsequent reviews:

NASA and Rocket Lab initially viewed a beach landing as the sole path for rocket delivery, since other infrastructure like a new bridge would require 1-2 years of additional analysis under the National Environmental Policy Act (NEPA) before construction could even begin.

However, timelines only deteriorated from there. Whereas in July, a September 2024 - March 2025 window was proposed, by October 2024, these plans had changed. An October 15 document submission to NOAA for compliance with Essential Fish Habitat (EFH) assessments showed that Rocket Lab and NASA had opened a new window for landings, now moved back an entire year and starting in September 2025:

Conversations we’ve had with aerospace industry experts, including NASA program specialists, indicate that assembly, integration, and testing of a rocket would require a minimum of several months from delivery.

“Usually seeing a stage hot fire, a large system rehearsal out on the launchpad, where they’ll bring it back down and everything works, then you’re close to launch. Then you’re probably conservatively a year away, aggressively 3 months away, but usually 6 months away when you get to all of those. I have not seen those things on Neutron, so I wouldn’t say they’re a year away from launch, compared to the best aerospace company in the world, SpaceX, which did not work any faster than that either. I’ve seen somewhat of a single engine fire, but I haven’t seen a full stage fire for any long duration with a cluster of engines, or a full stage completed that’s actually flight-like. So then we’re definitely 12+ months away, closer to 18.”

–Senior Aerospace Executive, February 2025

Rocket Lab’s delivery delay of an entire year has been in the public record since October. It should have been clear then that Rocket Lab’s mid-2025 first launch guidance was no longer valid, even as an optimistic stretch goal, which is why we were shocked to see the company keep this guidance in the Q3 2024 earnings report in November.

Wallops Launch Pad Is Behind Schedule, Alternate Transportation Options Won’t Help Delay

While Rocket Lab shows pictures of development on the Wallops launch pad, experts told us the pad looked many months away from being complete. We found local filings corroborate this, and also imply Neutron can’t launch before 2026.

“The last picture [of Wallops] I saw, I’d be surprised if they were going to be done by the end of year and have everything good to go from a regulatory perspective… there was a lot more dirt to be dug and structures to be installed.”

–Former Rocket Lab Executive, January 2025

The space and rocket infrastructure at Wallops, officially named the Mid Atlantic Regional Spaceport (MARS), is supported by NASA, but the funding and contract management runs through the State of Virginia-managed Virginia Spaceport Authority. This unique arrangement forces all work at the facility to be managed in compliance with Virginia State appropriation and funding law.

In particular, construction at the launch pad can be tracked via Virginia’s Procurement system (https://eva.virginia.gov/). We have been following progress at MARS for hints about where Rocket Lab stands on this front, and our research shows that numerous projects required for Rocket Lab to begin Neutron operations are well behind schedule. In fact, the entire island has a potable water problem that won’t get fixed until early 2026. Potable water is a requirement for launch.

Recent inspections of the Wallops utility water system in connection with a bridge widening project show a “catastrophic deterioration” of the water supply. This problem will not be fixed until January 2, 2026:

One NASA range engineer currently stationed at Kennedy Space Center told us that the availability of water was mission critical for deluge suppression systems and that its availability would dictate not only launches, but forms a prerequisite for construction of the final portion of the Neutron pad itself.

“Having all of the piping, emergency infrastructure to support some catastrophic event, all of the software demonstrated and proven, is all another piece. Getting a picture of a pad and a stand? Great. But there is a lot behind that that is less interesting from a picture perspective, but is very important, and that all takes time… And if one thing is off, you have to take multiple steps backward and prove that everything you just changed still works the way that you did when you tested and qualified it weeks or months prior.”

–Aerospace Executive

We confirmed that the critical issues in the potable water system were well known prior to Rocket Lab’s November earnings call. Certified plans for the reconstruction of potable water lines were dated the first week of November 2024. As with the rocket transportation setbacks, Rocket Lab did not address any of these issues to investors, instead remarking airily that on the regulatory front, “there's nothing that's kind of out of bed at the moment.”

As far as transportation methods for Neutron, the alternatives to a beach landing are even slower. During a November 20, 2024 Accomack County Board meeting, a Rocket Lab manager stated that a beach landing was no longer in consideration and Rocket Lab would pursue an alternate method to deliver Neutron.

This new option for rocket delivery appears to be dredging, which is even slower and will take years. A VMRC permitting application submitted December 23, 2024 asked for a permit to extract test samples at the Wallops NASA Ferry Dock. That dock is a dilapidated landing site that had been out of commission for well over a decade, and the sampling permit was to be used for a later application to dredge the inland channel and bay for ship transit operations.

As part of our investigation, we interviewed a permitting consultant with extensive experience in coastal permitting with VMRC and other Atlantic states. The consultant told us that based on the description in the preliminary sampling permit, the subsequent application for the dredging itself would take an additional 12-24 months from application to completion. As of the publication date of this report, Rocket Lab and NASA have yet to start the clock by submitting the dredging application for the channel shown below:

In addition to the costs and timing of such a significant project, these major civil engineering works would be subject to further review under NEPA. NASA policy explicitly demands a 2 year review for the sort of permitted dredging Rocket Lab is seeking, with no exceptions, per our review of documentation and expert interviews. It is important to note here that though the Trump administration is seeking to vacate all Council on Environmental Quality regulations relating to NEPA, NEPA itself is still in force.

Based on these findings, Neutron’s initial launch will drag well into 2026 because of rocket transportation issues and launch pad readiness alone.

It Would Take A Miracle: Neutron’s Engine Is Likely Behind Schedule

“If you don’t already have your qualified vehicle done, your engine mission duty cycles done, you’re not launching this year… you need to have that vehicle fully tested out, you have to have it to the pad, you’ve got to online your pad, which generally costs many times the value of the vehicle itself… They’re two years out at least. If they make magic, they could do it in 18 months. I don’t see a way that they could launch and launch successfully. They could fake it ‘til you make it, they could go launch the thing and have it blow up, or put it into the wrong orbit, or have it come apart and not be able to accomplish its primary mission, but doing that, I think, is far worse.”

–Former Senior Executive at Firefly Aerospace

The development of the rocket itself also appears delayed. Experts we spoke to underscored that the Neutron’s Archimedes engine still seems to be in the middle of the testing phase, despite Rocket Lab’s claims that the main hurdle left is production. While it would seem normal that a company about to launch a new rocket continues tweaking the design, rocket engine experts suggested that Rocket Lab’s continued adjustments to Archimedes mean the engines have a ways to go yet before they pass qualification tests and enter production.

In January, Rocket Lab released an image of the V2 Archimedes engine (below, left), which it stated was 200 kg lighter and offered “reliability and improved manufacturability” compared to the V1 engine (right). However, experts who reviewed the photos indicated that this was likely one of several iterations that Archimedes will need to go through to pass the qualification tests required for launch:

“If they could have used the engine from May, and it was maybe 200 kg heavier, but it worked really well, I’d guess they would have done that instead of taking the time to revamp that and potentially drag your launch schedule. ‘Simplified for reliability’ is the hint that the previous version maybe had something wrong with it, maybe wasn’t functioning quite as they expected. If you’re racing to get your first mission to orbit, you’re not going to fuck around with relatively small mass savings on the first stage and drive a multi-month schedule delay to do that. That just doesn’t make any sense. If it works as expected, you would use it, especially if engines are driving your rocket timeline.”

–Former Manager at SpaceX

“They did rotate some of their fluid lines, so I’m guessing they didn’t have enough flow on the first one. They were able to run it, but they didn’t have enough efficiency. That cryo line that’s poking right towards you? The first version had a stronger elbow, whereas this other one has more of a gradual elbow in the turn of it. They’re trying to get more flow to the pump, so they may have been cavitating on that. A lot of the connectors are now perpendicular to the engine access, so I think they had a vibration in it… I would hope to see V5, not V2… There are so many tweaks that will have to happen. The engine that flies will probably be extremely different from these. They need to make sure that they get the flow modeling correct, that they don’t get any hard starts or accidentally detonate inside the engine… they will inevitably happen.”

–Former Senior Executive at Firefly Aerospace

Rocket Lab portrayed the Archimedes hot fire videos it published last year as proof that the engine was nearing readiness in advance of the mid-2025 launch date, but the lack of data suggests that there are big performance gaps to close, as well as ongoing issues with combustion:

“You have to be wary of what the engine consists of. I see a pump on it, but I don’t see a flight-like package of all of its avionics working together on a single system. It says hot fire… but it doesn’t talk about duration, it doesn’t talk about performance. It said it received full thrust, but you can have full thrust with really shit efficiency, and you can be dealing with that for years. Then the payload performance is going to be shit commensurately. So yeah, I see that they have a hot fire at full thrust, but no duration and no communication that all of the engine components were in a flight-like configuration.”

–Senior Aerospace Executive

“The most recent hot fires are still showing a little bit of orange-yellow in the engine plume. If these are fully optimized, the flame should be all blue–see the Blue Origin engine’s hot firing.”

–Former Senior Executive at Firefly Aerospace

It appears the engine qualification and production timeline will stretch out months, if not a year or more from now.

“Late 2025… I would be very surprised if they hit that timeline. I think that’s probably off by 12 to 24 months, maybe even 36 months. I would anticipate that they’re going to deal with some struggles on the test stand with the Archimedes engine, that’s going to set the schedule back, and there’s going to be a market reaction… I envision that at one of the upcoming earnings calls, they’re going to have to communicate that there have been delays on Neutron, largely driven by the complexity of the engine and results that they’re getting from testing.”

–Aerospace Executive

“Without seeing an integrated stage, without seeing a fully qualified single engine, I wouldn’t put them [Rocket Lab] at more than 50% progress.”

–Senior Aerospace Executive

Neutron Structures are also Delayed with no Observable Progress

Rocket Lab has failed to show progress in critical Neutron components required for structural qualification and Stage 1 and Stage 2 tests, which presents a separate set of problems for the launch timeline.

Rocket Lab’s updated materials are missing qualification-ready components for Neutron’s Stage 1. The delay seems to be a resource and facility issue, as Rocket Lab struggles with engineering and know-how challenges it didn’t encounter with the much smaller Electron:

“I’d imagine given that they’re just now standing up the facility in Baltimore where they’re going to do production and doing some of that structural stuff, that’s probably slowing things down a little bit before they can get it to a full test regime… Stage 1 is much larger, so you can’t build that by hand.”

–Former RKLB Executive

"There hasn't been a huge amount of information, how well is that factory coming together... The real test is you want to actually see some detail on that rocket body, some harnessing being run, some equipment being bolted to it. When you just see a shell, that's pretty easy to put together, just a cylinder."

–Former RKLB Senior Engineer

There appears to be no shortcut to qualifying Stage 1 structures, either. RKLB will likely be unable to slipstream qualification of Stage 1 and Stage 2 together due to their differing designs, so delays in Stage 1 push Neutron’s launch back further:

“I think they have more complexity than most of the other rockets. Falcon 9’s Stage 2 is a squat Stage 1. When you qualify your structures, you have a lot you can qualify by similarity, and a lot you can learn from Stage 1 you can apply directly to Stage 2. Neutron has an entirely different Stage 2 design than its Stage 1 design. The lessons learned on one won’t necessarily relate to the other… There is no sign of Stage 1. I have seen a lot of PowerPoints and simulations, but for someone who’s very eager to show they have a tank being fabricated and tested, I haven’t seen a lot of concrete steps that matter in the world of rocket technology.”

–Former Senior Executive at Firefly Aerospace

“I haven’t seen any [Stage 1] tanks… first launch spring or summer 2026 would be my best guess.”

–Former RKLB Employee

A Delayed Neutron Will Hurt Rocket Lab’s Ability to Get NSSL Contracts

The largest opportunity for Neutron would be Lane 1 of the National Security Space Launch program, which spans at least 30 launches worth $5.6 billion. To onboard to the program this year and become eligible to bid for contracts, Rocket Lab needs to demonstrate that it can credibly launch by December 2025. With no 2025 launch, Rocket Lab’s Lane 1 onboarding will come no earlier than mid-2026, and further delays would put Rocket Lab at a 2027 onboard date.

Lane 1 launches are scheduled for 2025-2029 and SpaceX, Blue Origin, and ULA are already onboarded. The contract dollars are not hanging around: last October, SpaceX already won $734 million for Lane 1.

Of the process, a former Rocket Lab executive told us, “in order to become a bidder, you have to show a credible path to launch in the next year. They have tried to on-ramp, and in order to do so you have to do two to three launches within a year… the problem for Neutron is schedule.”

It looks to us like Rocket Lab will be late to the Lane 1 party, and it’s unclear what the leftovers are going to look like. Experts familiar with the launch contract process agreed:

“He’s [Peter Beck’s] telling the Street they’re going to make this [timeline] for this exact reason, for Lane 1, for NSSL, and my perspective on this is they’re not going to get there.”

–Aerospace Executive

“The NSSL program provides on-ramps for people to get in, but it requires them to at least have demonstrated the rocket… they have to be launching by 2025 to be eligible for this go-around.”

–Aerospace Engineering Executive

“They’re pretty smart people over there [at Space Systems Command] and you have to call a spade a spade. There’s no integrated stage test, there’s no operational launch pad. Hard to see that launching into orbit in 9.5 months. They’d have to wait another 12 months [to potentially onramp].”

–Senior Aerospace Executive

Rocket Lab Appears to Have Misled About Neutron Launch Contract Pricing; We Believe its Unnamed Customer is E-Space, A Startup with Questionable Ability to Pay For and Deliver a Constellation to the Pad

“They will 100% be [selling launches] at a loss. No one’s going to pay you a list price with profit on a vehicle on your first launch that has no guarantee to make it to space. I don’t see them making positive dollars until they have been able to demonstrate 3 to 5 launches.”

–Former Senior Executive at Firefly Aerospace

We believe that Rocket Lab’s first and so far only Neutron contract is not a full-price deal, contrary to what Rocket Lab’s has said, and the unnamed customer is an unreliable startup named E-Space. In November 2024, Rocket Lab announced it had signed a two-launch contract with a “confidential commercial satellite constellation operator” slated for mid-2026. On the Q3 2024 earnings call that month, Peter Beck insisted that the contract was “in line” with standard Neutron pricing of $50-$55 million:

Analyst: “And then you stated that the ASPs, you're going to be pretty firm on pricing. Is that the $50 million to $55 million that you initially talked about, and that's sort of where things have settled maybe for these 2 dedicated missions?

Peter Beck: “Yes. I mean the launch pricing, as we pointed out, is -- that was a really important thing for us. And I think as I've said, I made -- well, I kind of had to, but with Electron, it took us years to flush out bad contracts with respect to ASP. So no, this contract is in line with our previously discussed ASP for Neutron.”

However, it is unheard of for a launch vehicle with no reliability track record to charge full-freight pricing, so this statement appears to be a lie or at best, a misdirection. Industry experts, including former Rocket Lab employees, were skeptical of the value of the contract and the wording used to describe it, and they suspected that Rocket Lab was discounting the contract significantly:

"It would be pretty typical to be flying the first few flights at a discount, because as a customer you're taking so much risk on something that hasn't been proven yet... If you're a commercial customer and you're spending $40 or $50 million, you're going to go with the most reliable vehicle unless you were offered a significant discount."

–Former Senior RKLB Engineer

In fact, significantly discounted contract pricing may reflect Rocket Lab’s acknowledgement that Neutron performance will fall short of its advertised 13,000 kg payload capacity:

“[If] you’re not sure if you can hit the full performance that you’re out there talking about publicly, and you have this vehicle where you’re going to do a first test flight… you can’t exactly go out and sign a contract where you’re signing up to that full performance… They’re not coming out and saying ‘hey, this customer paid standard pricing’, they’re saying it’s ‘in line’, because lesser performance is going to be indicative of a lesser price tag, and so I think where that type of diction comes from.”

“If it were me writing this contract… I would basically say if we’re at this performance level, it’s going to be X dollars, if we can hit higher than that, it’s going to be this [higher] amount of dollars, and if we can hit what we’re saying publicly, the 13,000 kg [of payload to LEO], if we can hit that performance curve, in this case I would assume they would try to push the standard pricing. All the payment terms would be baselined at the very lowest level that was discussed and can be signed up to, and that’s going to be the one that’s planned for.”

–Former RKLB Executive

The background of the mystery customer lines up with someone willing to accept a deeply discounted flight on a rocket with no track record. We believe it is a startup called E-Space, run by entrepreneur Greg Wyler, who has a colorful and promotional history. We arrive at that conclusion in the following way: last November, Electron launched a satellite, Protosat-1, for a confidential customer. E-Space, for its part, had received clearance to send a payload to New Zealand in September (permit 2425-0903). September is just after RKLB’s confidential customer would have signed the launch contract, which carried a tight two-month turnaround from agreement to launch. As a final clue, Protosat-1 was registered under the flag of Rwanda, to which E-Space and Wyler have business ties.

A person we spoke to with knowledge of the industry agreed with our assessment:

“Rocket Lab has come out and said it’s a secretive first customer, which boils the population down to a handful in the space industry, because if people are going to launch their constellation, they want to be public about it because they’re raising more money. So there’s no point being secretive. Now you’re down to AST [Spacemobile], Apple, and Greg Wyler, basically. But Pete [Beck] actually came out and said that Neutron could potentially launch the entire constellation, whereas Apple’s already signed up with other launch providers, so that kind of discounts them if we’re to take Pete at his word.”

We believe E-Space is a lot more bluff than substance when it comes to actually getting things done. Wyler is a serial entrepreneur who founded the constellation OneWeb but left in 2017, before it had launched a single satellite; OneWeb went bankrupt in 2020. There is an odd information vacuum surrounding E-Space: there isn’t even a coherent description of their service on their website, which is laden with buzzwords. Where Wyler has made public pronouncements about E-Space, they have tended to be extreme, claiming that E-Space would put 100,000 or 327,000 satellites in orbit, making them by far the largest constellation in the world. Several senior executives and a board member have all churned out of the young company, while the satellite network is still unlaunched despite promises to hit mass production in 2023. There are only two recorded rounds of funding for E-Space since founding. At its core, E-Space appears to be a promotional and self-enrichment vehicle for Wyler:

“The other angle [to view E-Space from] is that Greg has gone from ship to ship basically trying to extract as much personal value as he can, and as soon as he does that he’s on to his next venture. This is kind of just the next one, where he’s very secretive, so he has people guessing, he’s trying to raise money, he’s trying to be in more unique places where investments in space aren’t as fruitful, like Africa, and trying to extract as much value [as he can]. And meanwhile he’ll just do the same thing and move on again. On a personal level, I wish him success, but I can also understand the school of thought of him just coming in, burning the ships, taking as much loot as he can, and moving on to the next venture before people realize what happened.”

–Person with knowledge of the industry

We asked the same person, “Is Greg Wyler money-good for the Neutron launches?”

Person with knowledge of the industry: “I consider that a risk item, quite frankly, because I don't know who's backing him, I don’t know how much they’re backing him for… he’s going to need hundreds of millions of dollars to get things even initially off the ground. The other risk item is schedule… like, who’s building these satellites? He’s got this one pathfinder [satellite] up there… I don’t think he has the operational size to do a number of these. How is this all going to work out? From the perspective of him getting close to that [Rocket Lab] launch date and going ‘Well, we’re quite frankly just not ready’ and having that [first commercial launch of Neutron] push out, I think that is also a factor there… I’ve got to wonder where Greg is going to get all his funds from… It’s not a great first [Neutron][ customer, and that’s because Pete [Beck]… thinks he can hold on price, and people are kind of sitting there and going, ‘This is a new launch vehicle, it’s fraught with risk. I’m not paying standard price.’”

A senior aerospace executive agreed that the company is a poor get for Rocket Lab:

“They [E-Space] haven’t even made it past [Series A] and it’s been four years… They’re probably not going to build a multi-100 satellite constellation with that size and that funding raised. I don’t see much progress to say that’s a real customer today. Rocket Lab need to show a more real customer than that.”

To the extent Neutron’s sole existing launch customer can’t pay or walks away from the launch, that will further hurt cash flow in an already cash-constrained business. For all the foregoing reasons, It appears that Rocket Lab’s cash flow needs are going to be extreme as a result of delays and profitability challenges with Neutron.

The Future of Rocket Lab is Neutron, and Delays and Unprofitable Launches Threaten a Cash Crunch

Neutron represents the lion’s share of Rocket Lab’s forecasted revenues, so significant rocket delays coupled with money-losing early launches threaten to push losses into the hundreds of millions of dollars. Three experts we spoke to forecast cash outflows will range from $300-$600 million before Neutron can reach profitability, which will force Rocket Lab to raise additional capital.

These estimated costs are split roughly evenly between 12-24 months of delays and 3+ years afterward, during which Neutron will be flying as an unproven, unprofitable, and single-use rocket (likely for the first several launches, per experts). The drag from delayed development and lossmaking launches will mean sizable labor charges, as Rocket Lab’s employee count has swelled to 2,000. Experts agreed customers will be unwilling to pay market rates while Neutron launches its first missions and attempts reusability. According to an aerospace executive, achieving reusability will take an estimated 3-5 years:

“Management are saying two years… I don’t believe that… They don’t have as much capital to burn as SpaceX did, and SpaceX was able to get really aggressive, experience a lot of failures, learn from those failures, and iterate. You need those failures to iterate quickly, and in order to fail a lot, you need tremendous amounts of capital. It won’t be two years. If I were a betting man, I’d say 3-5 years from first flight to the point where they’re recoverable.”

Even a reusable Neutron will lose money until Rocket Lab is able to turn around the rockets efficiently, something the company has not shown with Electron:

“The reusability case for Electron is not proven. The only way Neutron is going to be successful against SpaceX is to be successful with reusability. Not just an architecture that looks good and that works a few times… Even if the launch vehicle comes back successfully, the company still has to demonstrate a logistics turnaround, a recovery turnaround that is economically viable. That takes a number of launches in a row on a certain vehicle. The magic number with SpaceX ended up being around ten. Even if you had a reusable launch vehicle that launched 2 or 5 times, you really have to get to a much higher flight rate before you can say that’s economically reusable.”

–Senior Aerospace Executive

These ongoing costs mean Rocket Lab’s cash bleed is unlikely to stop for years. Rocket Lab had $504 million in cash, cash equivalents, and investments as of September 31, 2024. Rocket Lab’s existing business lines, Space Systems and Electron, have the potential to be moderately profitable at some point. Gross profits will be around $115 million for 2024 before overhead. However, these segments cannot finance hundreds of millions of dollars of cash losses, nor can they support a multibillion-dollar Rocket Lab’s market cap on their own.

“They’re going to have to do something to raise more money… I think they’re going to need a cash infusion before they’re profitable on Neutron. I think that’s what they’re fighting right now. They have a runway that is decreasing that’s saying they have to launch, and they’re trying to keep the stock price [up]… they have to be honest about where their schedule’s at.”

–Former Senior Executive at Firefly Aerospace

Rocket Lab’s Competitive Position For Neutron is Challenged

Rocket Lab’s medium-launch value proposition is also in question.

There is the matter of Rocket Lab’s foreign ownership and employee base amid Rocket Lab’s desire to perform bigger national security projects with Neutron. A senior aerospace executive with extensive DoD experience noted:

“There’s always that connection to New Zealand, both from their personnel and in the leadership and the ownership. You don’t have full control, and as a defense contractor that’s an issue. The CEO represents a whole cadre of foreign nationals to begin with, several hundred New Zealanders… When you’re launching a 5,000 kg satellite and it’s in the hundreds of millions, close to a billion dollars in value, they’re really going to take issue with it not being totally US-controlled and not being totally US-based employees that are working to assemble the launch vehicle and run launch service across that program.”

The former senior executive at Firefly Aerospace added, “Unless Peter Beck moves to the US full time, I think that’s going to continue to be a visibility issue.”

Then, there is Elon Musk. A former Rocket Lab executive said, “There’s not a whole lot of love lost between Elon and Pete Beck… He [Elon] is not shy about trying to screw over competitors.”

Elon has made his views on at least some of Rocket Lab’s claims clear.

The risk remains that history will repeat itself, and as with Electron, Neutron’s market will get eviscerated by SpaceX pricing, with the added kicker of years-long high insurance rates that will make competition even more difficult. A senior aerospace executive said:

“Falcon 9 really just picks its own price… If Neutron comes in at $50 million, I would say with confidence that SpaceX just lowers Falcon 9 to $50 million and it still continues to make money, still continues to drive market share… If you’re looking at the two launch vehicles at the same price, you’re competing with 400 launches vs. a first launch or even 10th launch vehicle with tons of risk still there. That risk manifests itself at a higher insurance rate. For Falcon 9, the customers pay 1-2%, but a new launch vehicle that comes online from a non-derived launch vehicle class, their rates are probably going to be 10-12%. So their customer is going to pay another $5 million to insure their launch in the earlier days of Neutron. Neutron has to price that in. Not only do you have to beat Falcon 9, you have to beat Falcon 9 plus a higher insurance price [as a commercial customer].”

A former Rocket Lab senior executive stated that even looking beyond Neutron development delays, the rocket’s small size will make it difficult to find a commercially viable niche amid current and emerging competition.

“My personal thesis is that Neutron is not going to be able to hold their pricing, just because they’re a bit of an odd fit in the market… Falcon 9 is the baseline, because everyone knows it’s going to be there for the foreseeable future. Anything below that, and you’re kind of a square peg in a round hole type of situation. That’s why you see New Glenn, and Vulcan, and Terran if it ever makes it to the pad, all these guys are higher performance. They’re trying to hit them [SpaceX] in terms of being at cost parity, but higher performance so you can fit a few more satellites, do a higher injection orbit… constellation providers are going to want to put up as many satellites in one go as possible so they can fill their orbital plane, do everything, and Neutron is going to be sitting here not being able to put up as much as Falcon 9, and now you need more launches just to fill your orbital plane, and so you have to space them out.”

As LEO constellation providers choose rocket vendors for their satellites, “a normal constellation is probably going to make a cut that leaves Neutron on the cutting room floor.”

Conclusion

Rocket Lab has captivated investors with the promise of Neutron, but our research shows that promise is built on shaky ground. With significant delays, unproven economics, and looming capital needs, we believe Rocket Lab’s bullish narrative will soon collide with reality. A Neutron launch in 2025 looks impossible, pushing back critical revenue opportunities and making the company’s financial position even more precarious. As expectations reset and the market wakes up to the long road ahead, we think Rocket Lab’s lofty valuation will come back to Earth.

Terms of Use

Use of reports prepared by Bleecker Street Research LLC (“BSR”) and this website is subject to and governed by the below Terms of Use (the “Terms”). The Terms govern all reports published by BSR (each a “BSR Report”) and supersede any prior Terms of Use governing the access and use of this website and BSR Reports, which you may download from this website. By downloading, accessing, or viewing any materials on this website, you hereby agree to the following Terms.

Bleecker Street and Its Related Parties

BSR is under common control and affiliated with Bleecker Street Capital LLC (“BSC”), Bleecker Street Capital Management LLC (“BSCM”), and affiliated funds, including but not limited to Bleecker Street Minerva LP (“Minerva”) and Bleecker Street Partners LP (“BSP”) (collectively, BSC, BSCM, and affiliated funds, including Minerva and BSP, are referred to herein as “BSC”). BSR is an online research publication that produces due diligence-based reports on publicly traded securities, and BSC and BSCM are investment advisers registered with the U.S. Securities and Exchange Commission. The reports on this website are the property of BSR. BSR and BSC, collectively with their respective affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, consultants and agents, are referred herein to as “Bleecker Street”, “us”, or “we”.

BSR is a for-profit journalistic organization that researches and provides opinion journalism about issues of concern to the general public, including about the securities of public issuers. BSR finances its journalism through a non-traditional revenue model where it earns revenue from positions that BSC takes in the securities of issuers on which BSR reports. This business model requires Bleecker Street to take material financial risk, which our partners have exposure to. To manage risk, we must close open positions as we deem prudent. We do not provide “price targets” for securities, although we may express our subjective opinion of the value of a security, which differs from a price target in that we neither know nor claim to know how the market might value such security. We therefore typically do not hold, and provide no assurance that we will hold, a position in a reported-on security until it reaches a price target, nor do we necessarily hold, or provide any assurance that we will hold, positions in securities until such securities reach the price that reflects our opinion of value. Many factors enter into investment decisions aside from opinions of the value of the security, including without limitation, borrow cost, “short squeeze” potential, risk sizing relative to capital and volatility, reduced information asymmetry, the opportunity cost of capital, client expectations, the ability to hedge market risk, our perception of the efficacy of market regulators and gatekeepers, our perception of the resource imbalance between us and any Covered Issuer (defined below), and our subjective perceptions. Therefore, you should assume that upon publication of a report, we will, or have begun to, close a substantial portion – possibly the entirety – of our positions in the Covered Issuer’s securities.

Reports Are Solely Attributable to BSR

The BSR Reports on this website are opinion journalism. On this website and through the BSR Reports, BSR is providing its journalistic opinions about issues of concern to the general public. You understand and agree that the opinions, information, and reports set forth on this website are attributable only to BSR, which bears sole responsibility for the information on this website and content of the BSR Reports; provided, however, that persons affiliated with Bleecker Street have provided BSR with publicly available information that BSR has included in the BSR Reports and on this website, following BSR’s independent due diligence.

Website and Report Use Is at Your Own Risk

Any and all use of BSR’s research and BSR Reports is entirely at your own risk. Neither BSR nor BSC is liable for any losses or damages you may incur as a result of your use of this website, including but not limited to any direct or indirect trading losses you may incur as a result of any information on this website, any BSR research, or any BSR Report. You agree to do your own research and due diligence with respect to any information on this website, and to consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities of an issuer discussed on this website (a “Covered Issuer”).

BSC’s Trading Practices and Positioning with Respect to Covered Issuers

As of the time and date of each report, BSC (defined below) is short the securities of, or derivatives linked to, the securities of the Covered Issuer, unless otherwise stated in the report. BSC therefore will realize significant gains in the event that the prices of a Covered Issuer’s securities decline. Upon the publication of each report, we may cover, and typically will cover, a substantial majority of our short positions. BSC’s covering its short positions upon the publication of a report is not a reflection of a lack of conviction in any opinions or the facts presented on this website or in any BSR Report. Rather, the act of covering BSC’s short positions upon the publication of a BSR Report is intended solely to manage risk in a prudent manner, consistent with the obligations of a fiduciary of our investors’ money. BSC are likely to continue transacting in the securities of Covered Issuer for an indefinite period after a report on a Covered Issuer, and we may be net short, net long or neutral positions in the Covered Issuer’s securities after the initial publication of a report, regardless of our initial position and views herein.

Notice to UK Residents

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO (each a “Permitted Recipient”). In relation to the United Kingdom, the research and materials on this website are being issued only to, and are directed only at, persons who are Permitted Recipients and, without prejudice to any other restrictions or warnings set out in these Terms of Use, persons who are not Permitted Recipients must not act or rely on the information contained in any of the research or materials on this website.

No Recommendation or Solicitation; No Warranties

All information and opinions on this website and in BSR Reports are for informational purposes only. You understand and agree that no information on this website or in any BSR Report is investment advice or a recommendation or solicitation to buy securities. In any given BSR Report, BSR is solely articulating its reasons at the time of publication for the positions it may have in the securities of a Covered Issuer. To the best of BSR’s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities of a Covered Issuer or who may otherwise owe any fiduciary duty or duty of confidentiality to the Covered Issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied. BSR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition, and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets, and liabilities. Such statements, estimates, projections, and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond BSR’s control. All expressions of opinion are subject to change without notice, and BSR does not commit to update or supplement any BSR Report or any of the information contained therein.

All Materials Copyrighted; Permitted Sharing

The information on this website, including but not limited to BSR Reports, are copyrighted and the intellectual property of BSR. You agree not to distribute any of the information on this website, whether as a downloaded file, a copy, an image, a reproduction, or a hyperlink to such file, in any manner other than by providing the following hyperlink: bleeckerstreetresearch.com. If you have obtained research published by BSR in any manner other than by downloading a file from the foregoing link, you hereby are on notice of these Terms, agree to these Terms, and agree not to use such research in a manner inconsistent with these Terms.

You further agree that you will not communicate or distribute the contents of BSR Reports and any other information on this site to any other person unless that person has agreed in writing to be bound by these Terms. You understand and agree that if you access this website, download or receive the contents of BSR Reports or other materials on this website as an agent for any other person, you are binding your principal to these Terms.

Limitation of Liability; No Special Damages

Bleecker Street shall not be liable for any claims, losses, costs, or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or consequential damages, arising out of or in any way connected with this website or the BSR Reports. This limitation of liability applies regardless of any negligence or gross negligence of Bleecker Street. You accept all risks in relying on the information and opinions in any report on this website.

Governing Law; Jurisdiction; Arbitration

You agree that any dispute between you and Bleecker Street arising from or related to these Terms, the information on this website, or any BSR Report shall be governed by the laws of the State of New York, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the state and federal courts located in New York, New York and waive your right to any other jurisdiction or applicable law. You agree that any dispute between you and Bleecker Street arising from or related to these Terms, the information on this website, or any BSR Report shall be brought exclusively in binding arbitration conducted in New York, New York by JAMS, before a single arbitrator, under the applicable JAMS rules. You agree that you waive the right to a trial by jury in any action or proceeding in any jurisdiction between you and Bleecker Street.

No Waiver; Validity

The failure of Bleecker Street Research LLC to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to the foregoing governing law and jurisdiction provision.

One-Year Limitations Period

You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to the use of this website or the material herein must be filed within one year after such claim or cause of action arose or be forever barred.