Gevo (GEVO): Fuel Me Once…

Key Points:

GEVO claims to have technology that allows it to turn inedible field corn into isobutanol, which can be a blendstock for sustainable aviation fuel (SAF) and other premium fuels. More simply, GEVO claims it can turn corn into jet fuel.

GEVO went public in 2010 after acquiring and retrofitting a production facility in Luverne, Minnesota. At the time GEVO said it would produce 10,000 barrels of SAF per day by 2012 and 60,000 by 2020. Instead GEVO effectively mothballed the plant in 2022.

In 2021, GEVO introduced its Net Zero 1 (NZ1) plant, in Lake Preston, South Dakota. The plant was to be financed by 2022 and fully operational by 2024.

After going through several different iterations of financing plans - and facing delisting - GEVO announced it would pursue funding through a Department of Energy (DOE) loan. As of 2024, all of GEVO’s hopes for financing NZ1 hinged on the DOE loan.

On October 16, GEVO announced it secured a $1.46 billion conditional loan from the DOE. While the DOE made clear that this was a “conditional commitment”, GEVO management has made representations that the loan is more likely to happen than it really is. We think regulations are clear: a conditional commitment is not binding if the DOE does not want to fund the loan. GEVO has said the loan would close no earlier than 2025, which means the Trump administration will be the one to fund or reject it.

We believe a Trump DOE is much less likely to approve the loan, as the DOE’s multibillion-dollar loan program is known to be in Trump’s crosshairs. We believe that failure to close the loan would cause a funding crisis for GEVO, and would likely result in massive shareholder dilution. And even assuming the loan is still a go, the other conditions still likely crush GEVO’s equity.

The EU Commission, Non-partisan think tanks and International Civil Aviation Organization have all criticized the sustainability claims of any and all ethanol derived sustainable aviation fuel. We suspect this form of “greenwashed” fuel will be avoided by international airlines as a result.

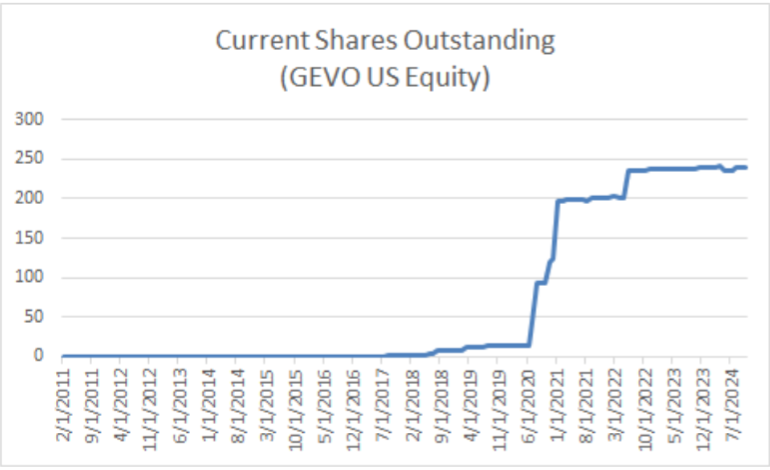

GEVO has a long history of promotional activity with little to show for it: the company has lost money in every quarter since going public. GEVO has generated minimal revenue, while shares outstanding have ballooned 1,269% since the IPO.

We are short GEVO shares, and think shares will soon give back the rest of their recent gains as shares are crushed by further dilution.

Initial Disclosure: Funds managed by Bleecker Street Capital, LLC are short Gevo, Inc. (GEVO). Please see the full disclosure at the end of this report.

Introduction

GEVO, Inc. (GEVO) calls itself a “growth-oriented, carbon abatement company with the mission of solving greenhouse gas emissions.” To further this goal, GEVO has been, for ~20 years, attempting to develop and commercialize a process that turns “residual starch from inedible field corn” into sustainable aviation fuel (SAF). More technically phrased, GEVO has a process that converts isobutanol into a blendstock for various hydrocarbon products, primarily jet fuel.

GEVO’s main product since going public in 2010 has been selling this carbon abatement story. Things have not gone well. GEVO has gone from partnership to partnership, and delay to delay. It has never achieved a profit in any of the 52 quarters since going public, and it has been able to generate only minimal revenues. The only things that have consistently grown are shares outstanding (up 1,269% since IPO) and executive compensation.

While we will explore below the full history of GEVO’s over-promising and not delivering at all, the brief version is that GEVO went public with a story that it would convert an ethanol refinery into a SAF production facility. This facility was to be generating 60,000 barrels of SAF per day in 2020. GEVO never generated meaningful revenue from the facility and mothballed it in 2022, citing a history of losses.

GEVO then pivoted to what they are calling a Net Zero 1 (NZ1) plant, to be built in South Dakota. Announced in 2021, and supposed to be operational in 2024, GEVO’s NZ1 plant went through a host of different financing options. After GEVO failed to raise the private capital it had talked about getting, GEVO finally turned to the Department of Energy (DOE) loan program.

GEVO received a $1.46 billion conditional commitment from the DOE in October. GEVO has represented that receiving the actual loan money is just a matter of execution from here, but we believe the Trump administration can simply decline to fund the loan. And the DOE loan program is one that has been in Trump’s crosshairs for a while.

On a conference call regarding the DOE loan, GEVO CEO Patrick Gruber was asked if a Republican win in the presidential election would “jeopardize” the loan. He responded that the “conditional commitment survives administrations,” which doesn’t answer the question.

In an additional blow to GEVO, North Dakota voters rejected a pipeline law that was necessary to fast-track a key component of NZ1, carbon capture and sequestration (CCS). CCS is so important to NZ1 that GEVO had previously threatened to move its plant if this pipeline wasn’t built. Perhaps out of desperation, GEVO spent $210 million in September to acquire energy assets in North Dakota that include CCS; but the North Dakota assets don’t qualify for the DOE loan. This acquisition will cause net cash to dwindle to an estimated $38 million, shrinking GEVO’s options as it continues to struggle to get NZ1 financing over the line.

For these reasons, GEVO is now entirely reliant on the conditional commitment from the DOE turning into a funded loan, and we think this is much less likely under the incoming administration. As such, we are short shares of GEVO.

GEVO’s History: Long On Promotion, Short on Revenue, Cash Flow

Founded in 2005, GEVO has a long history of promotional activity around whatever happens to be hot in the markets and no history of making money: it has lost money every quarter since it went public in 2010.

When GEVO IPOed, it was touting a letter of intent (“LOI”) with United Airlines to provide 10,000 barrels a day of renewable jet fuel produced from GEVO’s isobutanol product to be developed in a former ethanol plant in Luverne, Minnesota that GEVO acquired around the time of its IPO.

GEVO said at the time it would begin providing 10,000 barrels per day in Q4 2012, and “contemplated” a ramp up for 30,000 barrels per day in 2015, and 60,000 per day in 2020.

Luverne was the previous shiny object for GEVO before NZ1, and anyone contemplating the success of GEVO with NZ1 should study Luverne. Luverne was built out at small scale to support ~1 million gallons of isobutanol production a year. GEVO sold some of this to customers, and talked about scaling up the plant to support 17, 20, and 30 million gallons of capacity. But the plant consistently generated gross losses. Gradually GEVO shifted Luverne to ethanol production only, seemingly in an effort to make money, but gross losses continued and GEVO eventually halted ethanol production.

In 2021, GEVO management brought NZ1 to the forefront and stopped talking about expanding Luverne production. In Q2 2022, GEVO suspended operations and the plant remains effectively idle with a “history of operating losses.”

But stock promotions run on hope, and in 2021 GEVO had changed course. It was now going to build a greenfield facility in South Dakota to build its corn-to-jet-fuel vision for the future. The plant was called Net-Zero 1 (NZ1), and was supposed to be fully funded in 2023 and operational by 2025. Of course, that has not happened.

Instead, just like in its first iteration, GEVO has missed deadlines and seen losses continue to pile up. We will first explore how GEVO got here, and then discuss what we think will happen with the conditional DOE loan.

Just a Few of GEVO’s Broken Promises and Exaggerations Over the Years

GEVO’s NZ1 Journey…

Since its announcement, the NZ1 plant, like everything GEVO has done, has been plagued by delays.

In November 2020, GEVO claimed to have “term sheets” from equity investors and a “clear view” on debt structure for a $700mn three-site jet fuel deal. However, by January 2021, this story, too, went out the window. GEVO abruptly changed course and announced its plans for a standalone jet fuel plant called Net Zero 1 (NZ1) due to start operating in early 2024. We believe that this new project came about because GEVO was unable to land a deal under its original plan. Even with that reset of expectations, GEVO has repeatedly failed to meet its timelines for NZ1, burning cash and what was left of its credibility amid struggles to attract partners and funding.

When it unveiled NZ1, GEVO was flush with cash from a recent equity raise and claimed it was a year away from landing investment. CEO Patrick Gruber teased a financing in the works, stating that “this [Gevo’s cash balance] means that strategics approach us differently now. We expect that if and when we work with strategics, we'll be able to make a more balanced deal… Several parties are in discussion with us. No, we can't give more detail at this point.” He implied closing would be quick: “We’d expect to close a bond deal in the first half of 2022… or it could be less than a year from now.” Furthermore, GEVO stated it had enough capital to finance not just all of the equity for Net Zero 1, but to take “pretty significant positions” in a future Net Zero 2 and 3 plant, according to Gruber:

“At the CEO level, I just simplify it and say, we're doing 100% of the equity in Net-Zero 1 unless someone makes us one helluva sweet deal. And then in which case we'd share that cash flow stream. Now remember, we're greedy. We view that cash flow stream as roughly $100 million a year of EBITDA at the project level. And so why would we share it?”

However, by February 2022, timelines and basic technological parameters of the plant had changed. GEVO abruptly altered Net Zero 1’s planned jet fuel production to use an ethanol process licensed from another company, Axens, rather than using isobutanol. GEVO then stated that debt funding would not close before Q1 2023, nor would the plant be operational before 2025. By then, GEVO’s stock, which previously ran up on the NZ1 announcements, had fallen as progress failed to materialize.

In May 2023, as GEVO blew through its NZ1 development and financing timelines yet again, CEO Patrick Gruber attempted to quell investor fears by touting a deal with ADM and Phillips 66 to license Axens’ ethanol-to-jet fuel technology for payments to GEVO of up to $125 million. Gruber stated that “[w]e do expect payments to begin as early as late 2023, and they last approximately 5 to 7 years”; however, no such revenue has materialized.

With a significantly lower cash balance, GEVO has also shifted to talking about a licensing model for NZ1, which will involve selling off the majority or all of the equity in the plant. In May 2023, the company claimed to be undergoing an equity due diligence process with “a number of premier infra funds”, but no funding has emerged. Around this time, GEVO effectively staked its whole future on the outcome of the DOE loan, claiming that such a loan would be “the right approach”. It appears the company may not have had a choice, as CEO Gruber stated in June 2023 that private lenders would have offered interest rates of 10-18% for NZ1, which we view as a damning assessment of GEVO’s capabilities.

And recently, the same bullish announcements that have driven GEVO’s stock price up appear to be just another example of poor execution. In September 2024, the company revealed that it was spending $210mn on the acquisition of Red Trail Energy’s North Dakota ethanol plant and carbon capture and sequestration (CCS) well. This strikes us as a mediocre business on its face, and moreso at the nosebleed price GEVO paid. Red Trail has been running since 2007 and generated just $10mn of EBITDA in the last twelve months, while the CCS project required only $30 million of construction loans. GEVO’s motivation for buying the plant, we believe, is desperation. GEVO’s CCS partner, a company called Summit Carbon Solutions, has so far been unable to get approval for its carbon pipeline, suffering another defeat in a South Dakota ballot measure this Tuesday. Meanwhile, the Red Trail site sits approximately 400 miles away from GEVO’s NZ1 site, and Red Trail itself is not even eligible for the DOE loan GEVO is trying to secure.

Facing Delisting, GEVO gets an apparent lifeline in the form of a Conditional DOE Loan.

After a decade and a half of missed projections, losses, and minimal revenue, is this conditional DOE loan commitment the panacea for GEVO’s long-suffering shareholders? No, we think not. The loan commitment is more conditional than management has made it out to be.

On a call regarding the prospective deal, which GEVO expects to close in 2025, CEO Patrick Gruber was asked if a Republican win in the presidential election would “jeopardize” the loan. He responded that “the conditional commitment survives administrations”, which didn’t answer the question: does the conditional commitment force a hostile DOE to fund the loan? We believe the regulation that governs the Department of Energy’s Loan Programs Office is clear that the conditional commitment is not binding. If a loan applicant meets the terms set out by the conditional commitment, then the regulation states the DOE Secretary “may” agree to fund the loan:

“When and if all of the terms and conditions specified in the Conditional Commitment have been met, DOE and the Applicant may enter into a Loan Guarantee Agreement.” (emphasis ours)

We think a Trump DOE can easily opt for a “may not”, and kill the prospective loan.

Apart from this shakiness, meeting the conditional requirements is no easy matter. GEVO’s project is years out from consummation, as noted in the DOE press release:

While this conditional commitment indicates DOE’s intent to finance the project, DOE must complete an environmental review, and the company must satisfy certain technical, legal, environmental, commercial, and financial conditions before the Department can decide whether to enter into definitive financing documents and fund the loan guarantee.

Conditional DOE Funding Could Spell Significant Shareholder Dilution

As with battery materials projects in the US, GEVO’s prospective funding is from the Title 17 Clean Energy Financing Program. The expectation of a $1.46 billion loan commitment as well as the implicit Government endorsement of the underlying technology and business prospects for the Net-Zero 1 project has culminated in a current equity valuation of $400 million for GEVO.

As highlighted in our report on Lithium Americas (LAC), the underlying Title 17 regulations prohibit the government from funding more than 80% of a project’s cost.

Most of the projects generally receive loans in the range of 50-70% of total project cost. While GEVO has discussed getting much of the project construction costs reimbursed, it is unclear if it will be through the government loan, or project equity investors. Regardless, GEVO’s financials, even with the conditional DOE loan, are strung out.

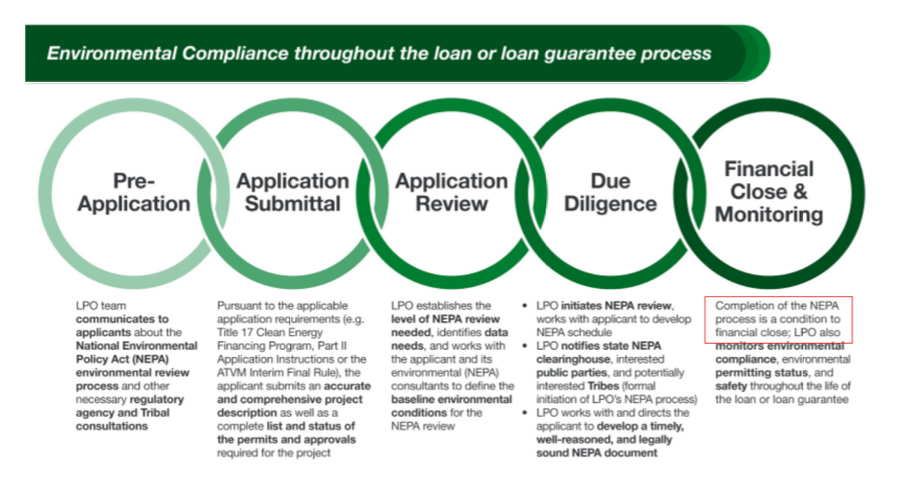

A Lengthy Environmental Review Is Required Prior To Project Funding

Title 17 loans are subject to NEPA as a subject Government action under the law, with the DOE explicitly noting in guidance that:

“Prior to financial close of a Title 17 loan guarantee, projects must complete the appropriate environmental review pursuant to NEPA.”

The DOE office does not have any NEPA documents on file for Gevo and our research indicates that a 1-2 year Environmental Assessment (EA) or 2-4 year Environmental Impact Statement (EIS) would be required for a facility of this size and complexity.

Management has not discussed this regulatory requirement, which we believe could add years to the timeline suggested by the company.

In the latest GEVO corporate presentation the company lists a 24 month construction time and a second half of 2024 start date.

For historical context, the DOE has approved just one “alternative fuel” NEPA review under its funding programs. The Abengoa Biorefinery was Selected for DOE financing of the $685 million project in February of 2007. The NEPA Environmental Impact Statement (EIS) was finalized via a Record of Decision (ROD) in January 2011, four years later. The facility began operations in October 2014. Parent Company Abengoa filed for bankruptcy in March 2016.

Recent Insider Selling From GEVO Executives, Despite The Coming Conditional DOE Loan News

Additionally, GEVO’s chief marketing officer sold shares on November 5.

Conclusion

GEVO shares have already declined precipitously from the highs, but we think this trend will continue. Insiders have been cashing out all year, and GEVO will need to raise a lot more money on its own to satisfy the conditions of this loan. Many of the other companies that have received these conditional DOE commitments have done massive offerings into the stock price run-ups after these announcements. We think GEVO will likely do the same. That assumes that the incoming administration does not simply change course on what it wants to fund.

GEVO has been long on hope and short on actual results. GEVO is the global leader in offtake agreements, with volumes several times higher than many global megacorps. Yet these agreements seem to never turn into real results. We believe the latest excitement around GEVO is unwarranted, and that it will soon unravel.

Bleecker Street Research LLC Terms and Conditions

By downloading from or viewing material on this website you agree to the following Terms of Service. Use of Bleecker Street Research LLC’s research is at your own risk. In no event should Bleecker Street Research LLC or any Bleecker Street Research LLC Related Person (as defined hereunder) be liable for any direct or indirect trading losses caused by any information on this site. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities of an issuer covered herein (a “Covered Issuer”).

As of the publication date of Bleecker Street Research LLC’S report, Bleecker Street Research LLC Related Persons (along with or through its members, partners, affiliates, employees, and/or Bleecker Street Research LLCs), clients, and investors, and/or their clients and investors have a short position in the securities of a Covered Issuer (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the prices of a Covered Issuer’s securities decline. Bleecker Street Research LLC and Bleecker Street Research LLC Related Persons are likely to continue to transact in Covered Issuers’ securities for an indefinite period after an initial report on a Covered Issuer, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in the Bleecker Street Research LLC’S research. One or more Bleecker Street Research LLC Related Persons have provided Bleecker Street Research LLC with publicly available information that Bleecker Street Research LLC has included in this report, following Bleecker Street Research LLC’S independent due diligence.

Research is not investment advice nor a recommendation or solicitation to buy securities. To the best of Bleecker Street Research LLC’s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities of a Covered Issuer or who may otherwise owe any fiduciary duty or duty of confidentiality to the Covered Issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Bleecker Street Research LLC makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition, and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets, and liabilities. Such statements, estimates, projections, and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Bleecker Street Research LLC’s control. All expressions of opinion are subject to change without notice, and Bleecker Street Research LLC does not undertake to update or supplement this report or any of the information contained herein. You agree that the information on this website is copyrighted, and you, therefore, agree not to distribute this information (whether the downloaded file, copies/images/reproductions, or the link to these files) in any manner other than by providing the following link: Bleecker Street Research LLC bleeckerstreetresearch.com The failure of Bleecker Street Research LLC to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to the use of this website or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.

Bleecker Street Research LLC Related Person is defined as: Bleecker Street Research LLC and its affiliates and related parties, including, but not limited to, any principals, officers, directors, employees, members, clients, investors, Bleecker Street Research LLCs, and agents.