SharonAI (SHAZ): The CEO Mawson Accused of Self-Dealing Now Runs a Neocloud Built on Phantom Contracts and Questionable Financing

Initial Disclosure: Funds managed by Bleecker Street are short SharonAI (SHAZ). Please see the full disclosure at the end of this report.

SharonAI's forward revenue story rests on a $1.25 billion contract with an Indian counterparty that earned $5.8 million last fiscal year. On April 1, 2026, SharonAI announced a five-year, $1.25 billion agreement with ESDS Software Solutions Limited. The contract requires ESDS to make annual payments averaging $250 million and post $140 million in letters of credit. ESDS reported $39.9 million in fiscal 2025 revenue and $69.5 million in total assets. The letter of credit obligation alone exceeds ESDS's entire balance sheet.

ESDS cannot legally service its core Indian customers from Australia. ESDS markets itself on Indian data sovereignty and serves more than 400 banking customers and government workloads subject to RBI data localization rules. ESDS's largest customer, accounting for roughly 20 percent of fiscal 2025 revenue, is Russia's Gazprombank, which has been on the U.S. OFAC SDN list since November 2024 and on Australia's Consolidated List.

Compass Point's own model discloses that ESDS contributes 76 percent of its $50 price target. The bull case's price target rests on a contract we believe cannot perform.

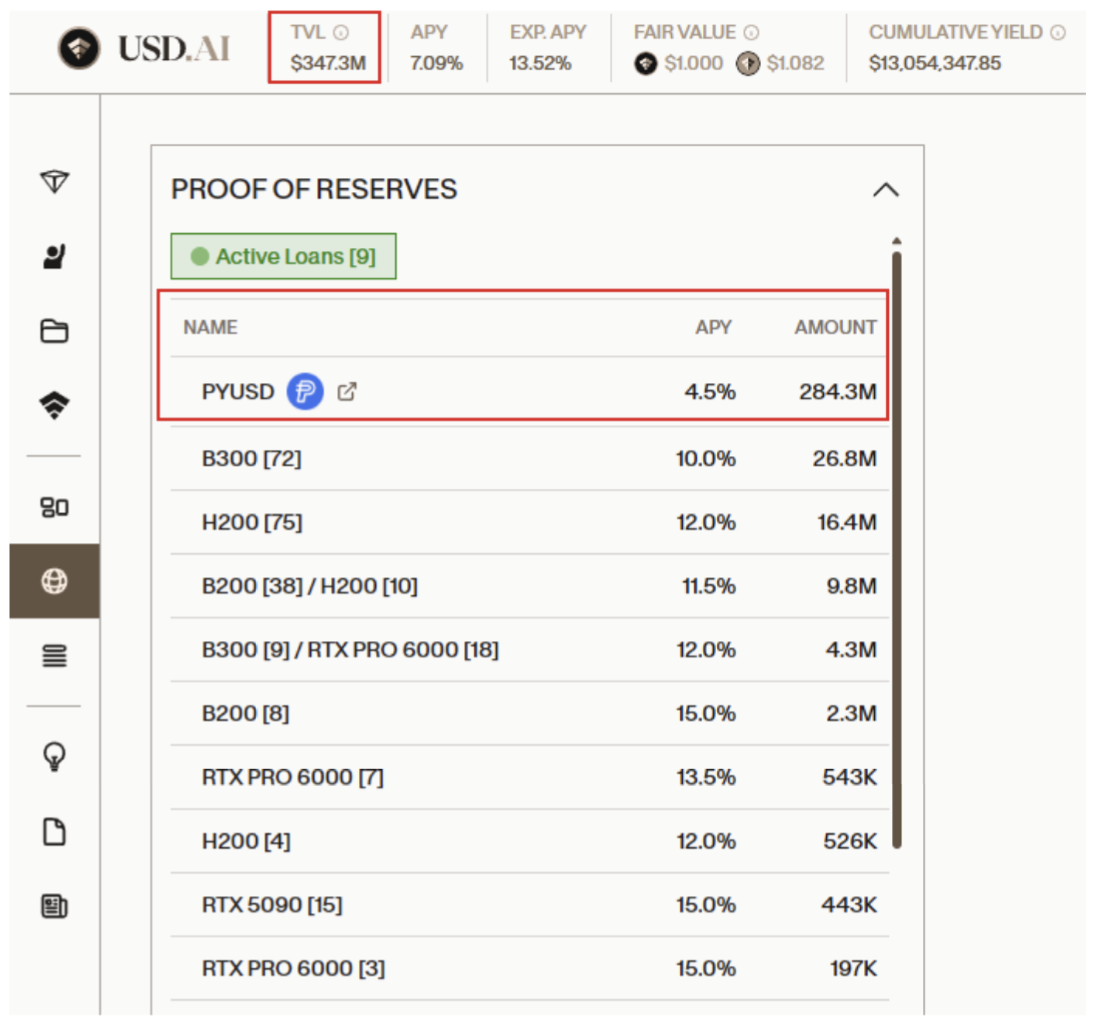

SharonAI's largest disclosed funding source has $284 million in lending capacity and has issued $1.2 billion in approvals. SharonAI's $500 million debt facility comes from USD.AI, a decentralized finance protocol launched out of private beta in the second half of 2025 by the same team behind a collapsed NFT-lending product. USD.AI's own Proof of Reserves page shows approximately $284 million of capital available for lending against $1.2 billion in approvals across three counterparties: SharonAI, a Tokyo-listed company whose primary historical business is eyelash extension salons, and a subscale Georgia bitcoin miner.

Management's $350 million convertible confirms the funding gap is real. Eighteen days after Cantor told investors SharonAI had a $795 million "war chest," SharonAI signed a $350 million convert with Oaktree at 6 percent. The convert closes only if SharonAI signs a separate binding customer contract for at least 4,068 GPUs. The founders extended their lock-ups through March 31, 2027 as a closing condition. If the ESDS contract represented bookable demand, the additional GPU requirement would be unnecessary.

CEO James Manning is running the same playbook he ran at Mawson Infrastructure. Manning's prior public company, Mawson Infrastructure Group, is suing him for allegedly routing $11.5 million through Flynt ICS, a shipping company he controlled through Vertua without disclosing his interest to the board. Mawson alleges Manning sent threatening imagery to a board member and told a third party he would "burn Mawson to the ground." Flynt ICS is now a disclosed vendor of SharonAI. Two Mawson senior personnel followed Manning to SharonAI. The same supervoting structure that entrenched Manning at Mawson has been replicated at SharonAI: 65 percent of votes against 1 percent of economics.

SharonAI's foundational acquisitions were sales by insiders to themselves. Manning, Hughes-Jones, and Leece sold their private Australian entities into the SharonAI public shell for stock they themselves valued. Vertua, a Manning-controlled vehicle, marked its DSS asset at zero on September 30, 2023. Nine months later, on June 29, 2024, SharonAI acquired DSS for $25 million in stock, paid to Manning, Hughes-Jones, Leece, and Vertua. The publicly available record does not identify a transformation in DSS's underlying business that would explain the markup.

SharonAI told investors NVIDIA was a strategic shareholder, then withdrew the statement two weeks later. The 10-K filed March 31, 2026, signed by Manning, told investors "NVIDIA is a strategic shareholder in SharonAI." On April 13, 2026, SharonAI filed a Form 8-K stating "NVIDIA Corporation was not a strategic shareholder in the Company and... does not hold any equity securities of the Company." The 10-K was not amended. The correction was filed under Item 8.01, "Other Events," not Item 4.02, "Non-Reliance on Previously Issued Financial Statements."

The Post-Effective Amendment filed April 17, 2026 registers approximately one-third of the float for resale. Among the named selling shareholders are Lucid Capital Markets, which led the February IPO and initiated coverage on April 17, 2026 with a $50 price target, and Lucid's Head of Capital Markets, who is registered to sell approximately $16.7 million of stock.

SHAZ at Face Value: "The CoreWeave of Australia"

SHAZ markets itself as "a leading Australian Neocloud" and a high-performance computing company focused on AI and cloud GPU compute infrastructure. Management frames the company as a Southern Hemisphere and Asia Pacific answer to CoreWeave, Nebius, and the U.S. neocloud cohort.

SHAZ built its own bull thesis over a compressed eight-week window, beginning with a February 2026 Nasdaq uplist and culminating in the recent announcement of a $1.25 billion contract with ESDS Software Solution.

Management claims the ability to deploy to more than 20,000 NVIDIA B200 and B300 chips, with 8,000 of those B300 units committed under the ESDS contract, as a certified NVIDIA Cloud Partner (NCP), one of three NCPs operating in Australia.

On March 31, 2026, SharonAI released its fiscal 2025 results alongside a forward outlook for 2026. The press release highlighted six capital and capacity-building milestones from the preceding six months:

A $125 million Nasdaq uplist offering completed in February 2026

A $100 million convertible note raise in December 2025

A strategic investment and up to $200 million revenue-share facility from Digital Alpha Advisors, LLC

A secured debt facility of up to $500 million from USD.AI

Expansion of expected data center capacity with partner NEXTDC from approximately 50MW to approximately 70MW

Sale of a 50% interest in the Texas Critical Data Centers joint venture for $70 million, which management characterized as "recycled capital" to accelerate its Australian GPU business

The day after it released those results, SharonAI announced the ESDS contract.

The Bull Case in Numbers: 76% of Compass Point's Price Target, 75% of Lucid's Contracted Revenue, and 100% of Cantor's $1 Billion Run Rate Depend on ESDS.

Cantor Fitzgerald initiated April 8, 2026 with a $40 price target. Cantor projects $1 billion of annualized revenue by year-end 2026, anchored by the ESDS contract generating roughly $60 million per quarter beginning Q3 2026, and cites $795 million of available capital. That figure includes the full $500 million USD.AI facility as if it were entirely available and drawn. The note sent shares 20% higher on the day.

Compass Point initiated April 22, 2026 with a $50 price target via a segment-level sum-of-the-parts. Its own SOTP discloses that ESDS contributes $37.90 of the $50 target, or 76 percent. Compass Point's CY27E revenue forecast of $376 million is roughly 60 percent below the Street consensus figure of $931 million, a gap Compass Point attributes to "Street giving SHAZ credit for capacity not yet under contract."

Their latest financing is also contingent on a customer contract….

The $1.25 Billion Contract: SharonAI's Anchor Customer Earned ~$5.8 Million Last Fiscal Year

“While a new name for many, it is our view that ESDS can be classified as a high-quality counterparty. The agreement gives SharonAI its first, large, contracted revenue base and gives lenders and equipment providers a concrete contract to finance against as the next build cycle moves forward.” - Compass Point April 22, 2026 Initiation

"…contracted customer offtake agreements provide the financial assurance necessary to secure GPUs at scale and to support underwriting of significant debt facilities, with the 'take or pay' structure providing minimum levels of revenues." - SharonAI 10-K

On April 1, 2026, SharonAI announced the signing of a five-year, $1.25 billion AI cloud infrastructure agreement with ESDS Software Solutions Limited (ESDS). The contract stipulates that SharonAI (SHAZ) is to deploy and operate a cluster of approximately 8,200 NVIDIA B300 GPUs in an Australian data center. SharonAI’s stock surged 30% upon announcement, and since then current coverage and sell-side forecasts depend on the ESDS deal being realized.

If this customer were to disappoint, current projections would be at risk of collapse: ESDS dominates near-term revenue assumptions across all three sell-side models, ~75% of Cantor Fitzgerald’s contracted capacity (~15MW out of 20MW), and ~90% of Compass Point’s next twelve months revenue ramp. SharonAI's forward revenue story hinges on ESDS performing under the $1.25 billion, five-year contract.

ESDS Software Solution is a Nashik, India-based private cloud and data center operator running Tier III facilities across four Indian cities: Nashik, Navi Mumbai (Airoli), Bengaluru, and Mohali. The company has twice filed to go public but has yet to launch an offering.

ESDS filed its first draft prospectus in September 2021, targeting approximately ₹12–13 billion, or ~$130 million, then withdrew it, citing “unfavorable market conditions”. ESDS refiled in March 2025, and eventually settled on a downsized ₹7.2 billion offering, or ~$76 million, this time. Even if the second IPO attempt does succeed, we do not believe ESDS has the ability to support the SHAZ contract.

As per ESDS’s 2025 Annual Report, for the fiscal year ended March 2025, ESDS generated ₹3.7 billion in consolidated revenue, or just $39.9 million. EBITDA was ₹1.5 billion, or ~$16.3 million. Net Profit was ₹543 million, or approximately ~$5.8 million. Across the three most recent fiscal years, ESDS's cumulative net profit totaled approximately ₹454 million, or ~$4.8 million, inclusive of losses in FY2023 and modest profits in FY2024 and FY2025.

ESDS has not earned, in its entire recent operating history, even 2 percent of what it has now committed to paying SHAZ in a single year. The SHAZ contract obligates ESDS to annual payments averaging approximately $250 million. That figure is roughly 6.3 times ESDS's entire fiscal 2025 revenue and approximately 43 times its fiscal 2025 net profit. The estimated annual commitment would represent almost ~5,200% of their recent cumulative historical Net Income.

Even if ESDS's second IPO were fully successful, it would raise approximately 6 percent of the total contract value. ESDS would need to complete roughly sixteen IPOs of this size to fund the contract.

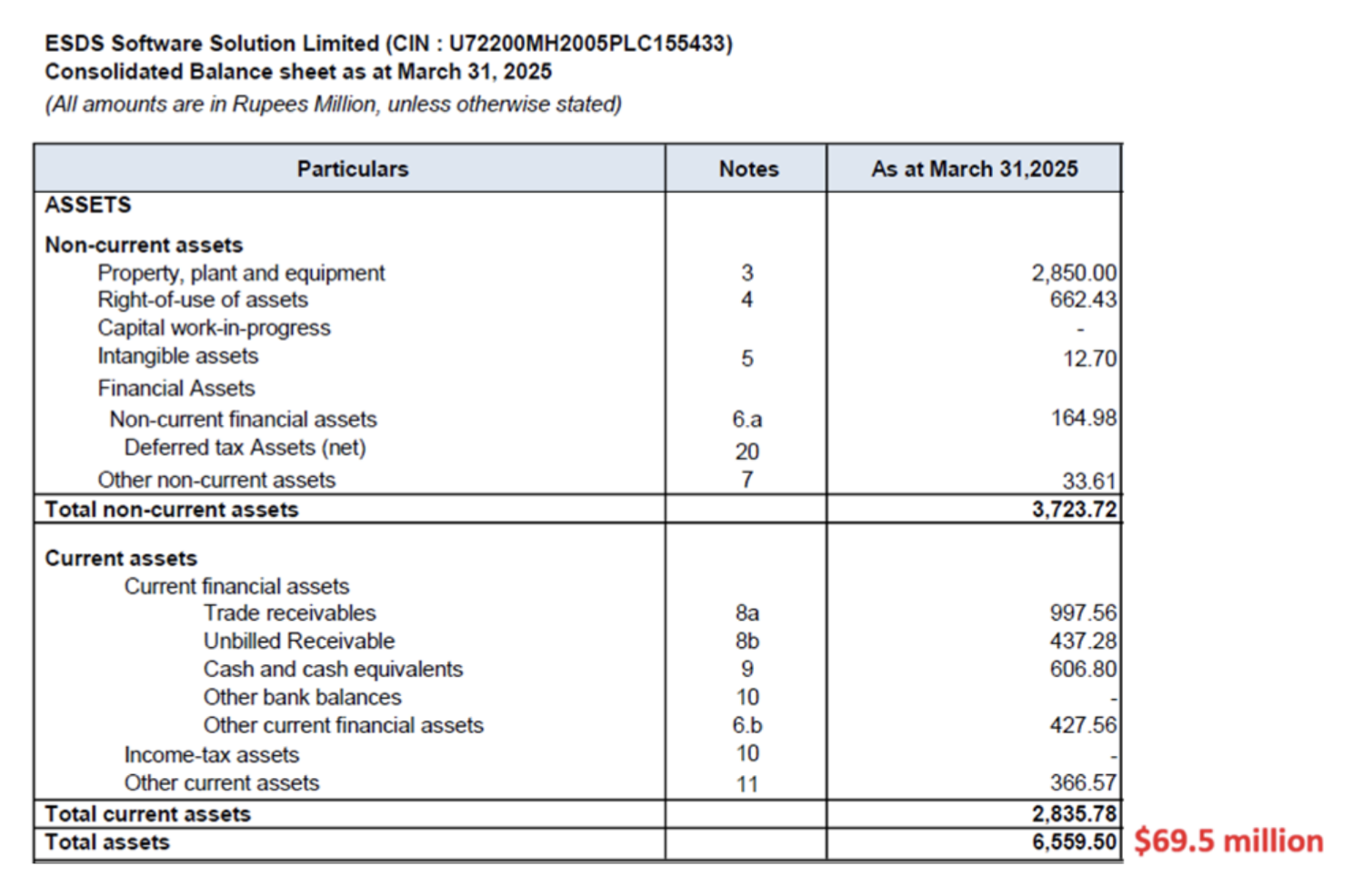

ESDS’s balance sheet raises the same question. The SHAZ agreement requires ESDS to post $140 million in letters of credit. Based on ESDS's fiscal 2025 disclosures, this figure exceeds its total assets of ~₹6.6 billion, or ~$69.5 million. We do not believe there is any realistic path for ESDS to collateralize an obligation of that size:

ESDS Software Solution’s Balance Sheet as of 3/31/25, showing ~$69.5 million in total assets

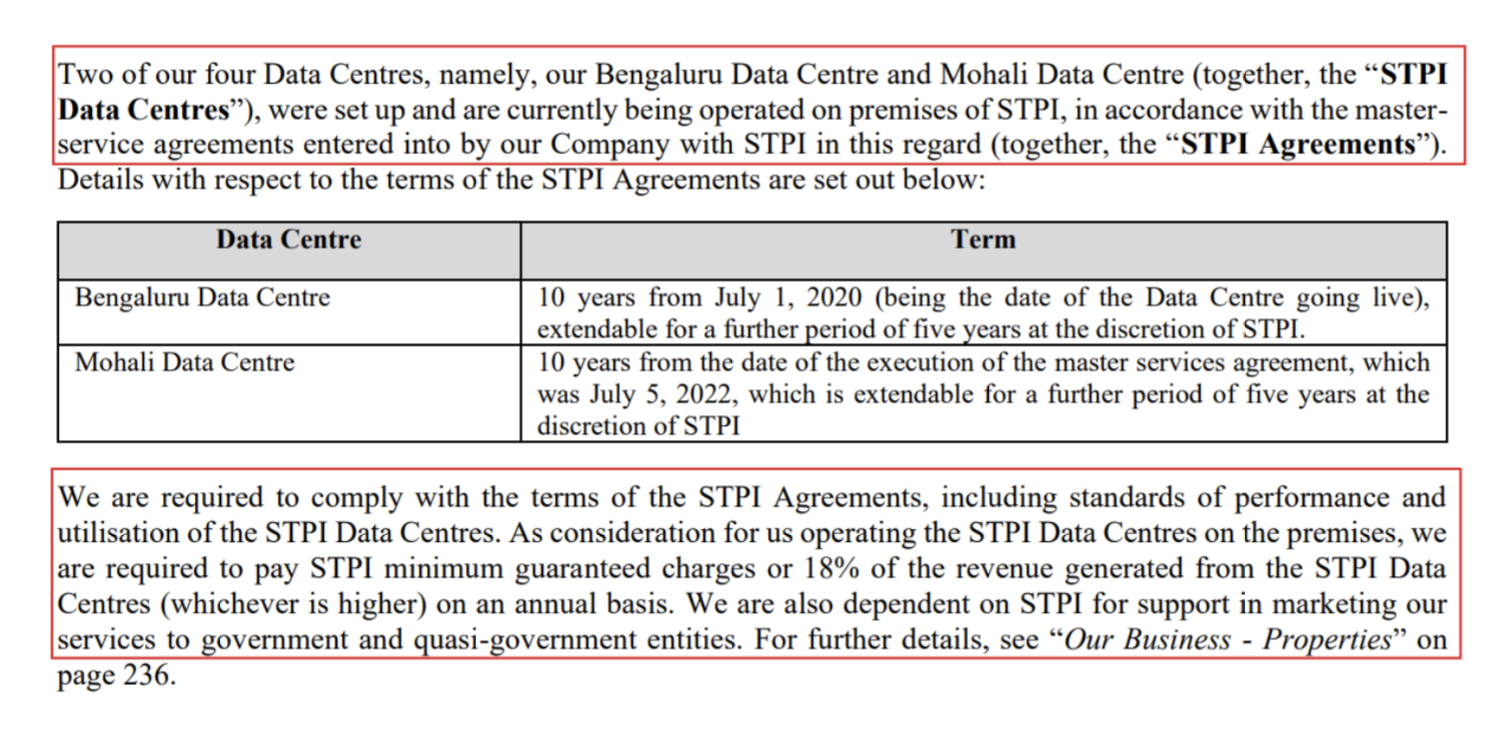

The total capacity of ESDS's existing data centers is relatively small. In a November 2024 interview with Entrepreneur India, Piyush Somani, ESDS's CEO, disclosed that ESDS operates approximately 7MW of total data center capacity across its four Indian facilities, and that his stated ambition was to grow that to 14-20MW over the next one to two years.

As of April 2026, these core new capacity buildouts seem to have fallen short as their FY25 annual report and website still only lists four primary data centers; and among these cities, two of the four datacenters are established on government premises and include revenue sharing agreements per their prospectus:

A 2024 profile of Somani claims that “he has successfully expanded ESDS Group to 19 nations across APAC, Europe, the Middle East, the Americas, and Africa.” As far as international operations extend, we found ESDS’s non-domestic footprint and customer base to consist largely of a lossmaking subsidiary in the United Arab Emirates; a Delaware subsidiary with no revenue (AOC-1 of FY25 Report); and ESDS’s largest customer, sanctioned Russian financial services business Gazprom Bank.

Under the contract with SHAZ, ESDS would be drawing on more than twice the data center capacity it currently operates worldwide, on a continent where it has no footprint, no disclosed customers, and no existing regulatory relationships. Regardless of its reasons for announcing a deployment in Australia, ESDS does not resemble a company on the verge of supporting $250 million a year in payments.

What Was ESDS's Strategic Rationale for Signing This Contract?

The apparent financial impossibility of the contract is only half of the problem. The deeper issue is that the contract makes no strategic sense for ESDS on its own stated terms. ESDS's entire commercial identity is built on Indian data sovereignty.

In the 2024 Entrepreneur India interview, ESDS Chairman and CEO Somani shared: "Customers should host their data in Indian data centers so that they get to use Indian IP addresses, Indian encryption, and contracts are executed by Indian companies so that the law of the land is applicable."

This messaging has remained consistent, as just five days after Sharon AI announced the $1.25B signed ESDS contract - Somani posted on LinkedIn: “It is estimated that over 70% of India’s data is stored and processed on infrastructure owned by global players… Now imagine a future where 100% of India’s critical data is stored within the country, running on Sovereign platforms and governed by Indian policies.”

ESDS's corporate marketing is built on the same nationalistic foundation. From various recent corporate blog posts to the Company's Sovereign Cloud page, ESDS warns customers that "data hosted in India on foreign cloud platforms can still be accessed under external laws like the U.S. CLOUD Act" and that "using foreign-governed infrastructure exposes mission-critical workloads to potential surveillance, access requests, and service disruption." The homepage asks prospective customers directly: "Which side are you on, an Indian expert with 20+ years of experience or an expansive MNC [multinational corporation]?"

Just recently in November 2025, ESDS also announced the launch of their own “GPU-as-a-Service” offering with a domestic portfolio of NVIDIA and AMD chip clusters - referring to it as “India’s Sovereign AI Infrastructure” in its marketing videos.

Statements and service offerings like these raise the question of why ESDS is pursuing such a transformative deal, one it apparently cannot fund, in a foreign jurisdiction, in a new market, with infrastructure from another player.

A review of ESDS's customer base reveals that those customers may not even be able to use this capacity.

In an interview with Enterprise IT World dated October 2021, ESDS stated: "ESDS has the largest number of banking customers in India, including more than 400 cooperative banks, district cooperative central banks, and small banks. ESDS is also a market leader in hosting in Government Cloud applications.”

These customers are subject to mandatory data localization. The Reserve Bank of India's (RBI) April 2018 circular on Storage of Payment System Data requires that "the entire data relating to payment systems operated by [providers] are stored in a system only in India. This data should include the full end-to-end transaction details." The RBI takes enforcement seriously. The central bank indefinitely barred Mastercard from onboarding new domestic customers in July 2021 for data localization violations, and similarly restricted American Express and Diners Club. Indian government workloads under MeitY empanelment and STQC certification face equivalent constraints. The customers ESDS has spent decades signing up on the explicit promise that their data stays in India cannot legally use compute located in Australia.

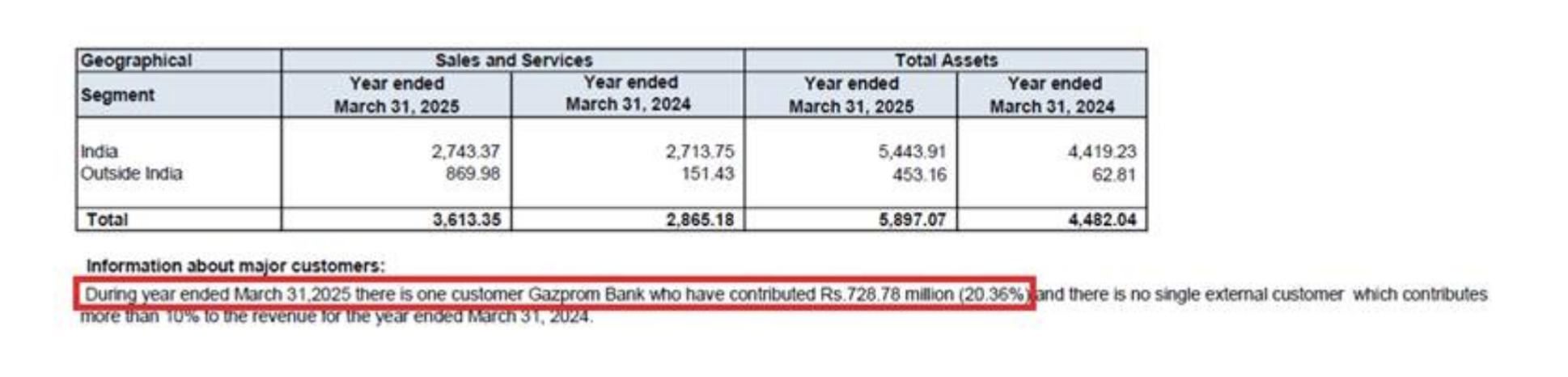

ESDS’s top customer also cannot do business in Australia, either, but this is because Australia and the United States have sanctioned it. In FY2025, ESDS generated ~20% of its revenue, or ~₹728 million rupees (~$7.7 million), from Gazprom Bank. This amount constitutes almost all of its YoY sales growth and international revenue:

ESDS’s silence around the SharonAI deal raises further questions. Somani has not made any public statements on a contract that, if performed, would multiply ESDS's revenue six-fold. His X (formerly Twitter) account, which is active, makes no mention of the SHAZ contract. ESDS's LinkedIn and X accounts, which similarly highlights Indian conference appearances and other events ESDS is involved with, also makes no mention of the contract.

The press release quotes SHAZ CEO James Manning but contains no quotes from any ESDS executive. Tweets by Somani after the contract was signed continue to focus on touting sovereign Indian data.

SHAZ’s Largest Announced Funding Comes From USD.AI… Which Has “Approved” $1.2 Billion in Facilities to a Japanese Eyelash Extension Company, a Bitcoin Miner in Georgia, and SHAZ.

“With any neocloud business, access to capital is extremely important given how capital-intensive the business is. Thus far, SHAZ has: raised $125m from its February IPO, raised a $100m convertible note, and raised $70m from the sale of assets in Texas. It has also secured a $500m debt facility with USD.AI… we estimate that SHAZ has access to ~$795m. While this is sizable, it is ultimately a fraction of what SHAZ will need should it be able to build out its cloud platform to over 1 GW.” Cantor Fitzgerald, April 8, 2026 Initiation, Overweight, $40 PT

On January 22, 2026, SHAZ announced the financing arrangement, stating that USD.AI had "approved a debt facility of up to $500 million for SharonAI, a subsidiary of the company, subject to execution of definitive documentation." In its April 8, 2026 initiation, Cantor Fitzgerald told investors that SHAZ has "access to ~$795m" in available capital. Cantor's breakdown: $125 million from the February IPO, $100 million from the December 2025 convertible note, $70 million from the sale of Texas Critical Data Centers (TCDC), and $500 million from a debt facility with an entity called USD.AI.

Over 60% of Cantor’s number comes from the USD.AI debt facility.

USD.AI is not a bank. It is not a private credit fund. It is a decentralized finance protocol launched out of private beta in the second half of 2025 by a Delaware entity called Permian Labs, which raised a $13 million Series A in August 2025. The protocol issues two primary crypto tokens, USDai and sUSDai along with a governance token, and lends the proceeds to AI hardware operators against GPUs tokenized on-chain as "GPU Warehouse Receipt Tokens."

USD.AI is operated by Permian Labs, a Delaware corporation founded in 2021 by David Choi (CEO), Conor Moore (COO), and Ivan Sergeev. The Permian Labs team's prior product was MetaStreet, an NFT-collateralized lending protocol that launched in 2021 and continued operating through 2024.

USD.AI is not a new business. It is the same team that pivoted from a collapsed NFT-lending sector to an AI-themed lending sector. The codebase, the founders, the venue, and the financial mechanics are all recycled.

In the USD.AI protocol itself, the Total Value Locked (TVL), in essence the value of deposits or capital available for lending, was effectively zero in early June 2025. It crossed $250 million in early September 2025 and approximately $675 million by January 2026 per DeFiLlama. As of the January 22, 2026 announcement date of the SHAZ facility, the protocol's total balance sheet was roughly the same size as the single $500M facility it had approved for SHAZ.

However, since the announcement the protocol’s TVL has quickly declined to less than $350 million as of April 2026, inclusive of existing GPU loans, and per USD.AI’s own Proof of Reserves page currently only holds ~$284 million of capital available for lending.

The counterparty that all three sell-side initiations took at face value as being able to fund $500 million of SHAZ's capital needs is a one-year-old on-chain credit experiment - whose entire balance sheet is currently less than their single “approved” debt facility.

However, SHAZ is not the only recently founded neocloud relying on USD.AI for hundreds of millions of dollars of debt funding.

The Same $500 Million ‘Approval’ Has Been Issued to Tokyo-Listed Eyelash Company and a Subscale Georgia Startup

The press release announcing the SHAZ facility states that USD.AI has approved 'more than $1.2 billion in guidance and non-recourse facilities' across all counterparties.

In December 2025, USD.AI announced that it had approved a $200 million GPU financing facility with Quantum Solutions.

Quantum Solutions is a Tokyo-listed company with a ~$32 million USD market cap. It was originally founded in 1999, and its public filings describe it as a company engaged in "system solutions and eyelash care businesses," with operations spanning EV development, system consulting, gaming content, and "management of eyelash extension stores."

In July 2025, Quantum Solutions announced it was pivoting to a Bitcoin treasury strategy, targeting accumulation of 3,000 BTC. CEO Francis Zhou said the goal was to make the company "Bitcoin-first." Quantum Solutions is now USD.AI's $200 million GPU financing counterparty in Japan.

Quantum Solutions shares are down 85 percent from their post-pivot highs and 75 percent since the USD.AI facility was announced.

SHAZ’s $500 Million Approval Mirrors Agreement With QumulusAI, A Subscale Startup in Georgia

Three months before SHAZ announced its $500 million USD.AI facility, another former bitcoin miner mid-pivot to AI announced a structurally identical deal.

QumulusAI is, like SHAZ, is a bitcoin mining business repackaged as an AI infrastructure company. Per its S-1, the company traces to two Georgia entities: WAHA Technologies and SPRE Commercial Group. WAHA "specialized in blockchain managed services." SPRE focused on "data center assets and operations." The two rolled up into Global Digital Holdings in December 2022.

QumulusAI has been hunting for public-market access since early 2025. After an initial failed reverse-merger attempt, the Company renamed itself and pursued a direct listing under the proposed ticker QMLS. A direct listing raises no capital. Its primary function is to make insider shares freely tradable. On September 25, 2025, QumulusAI appointed Mike Maniscalco, the former Applied Digital CTO, as Chief Executive Officer. The $500 million USD.AI facility was announced two weeks later, on October 9, 2025.

QumulusAI’s actual operating business is small. Per the S-1/A, QumulusAI generated approximately $11.8 million of revenue in 2025, and operates "more than 1,120 GPUs" across three colocation sites in Georgia, Missouri, and Kansas City. The $500 million USD.AI facility was more than forty times the company's trailing twelve-month revenue.

The QumulusAI facility was announced six months ago. The Company directly references it in its latest April 2026 S-1/A as a $500 million Credit Facility it has drawn on for $4.3 million in February 2026. SHAZ is the third documented customer of that product: reliant on a facility with ~$284 million of available lending capital against $1.2 billion of announced approvals, a ~76% deficit, across three counterparties and unable to support the standalone SHAZ facility due to a lack of reserves.

$350 Million Convertible Confirms the Funding Gap Is Real

On April 26, less than three weeks after Cantor Fitzgerald told investors SharonAI has access to a $795 million war chest, SharonAI signed a definitive agreement for $350 million of 6.0% convertible senior notes, due in 2031. The financing was led by Oaktree Capital, with participation from Two Seas Capital. Lucid Capital was the sole placement agent.

The transaction confirms what the analyst war-chest math obscured. SharonAI ended fiscal 2025 with $71 million of cash. It raised $125 million on Nasdaq in February and announced a $70 million Texas Critical Data Centers sale in March. It has now agreed to take an additional $350 million from a credit shop at 6% with a 20% conversion premium and a maximum dilution of 8.7 million shares. The convert is expected to close on our about April 30, conditioned on SharonAI’s entry into a binding customer contract for a minimum of 4,068 GPUs in connection with a project named “Sydney S6.” Furthermore, as reported by the Financial Review, SharonAI is seeking an additional $200M raise as part of an ASX listing.

The convert is expected to close on or about April 30, conditioned on SharonAI entering a binding customer contract for a minimum of 4,068 GPUs in connection with a project named "Sydney S6." Separately, the Australian Financial Review reported on April 28 that SharonAI is seeking an additional $200 million raise in connection with a planned ASX listing.

An additional condition of the deal was that the founders extend their lock-up through March 31, 2027.

The Mawson Playbook: SHAZ's CEO Has a Documented Pattern of Self-Dealing and Threatened to Burn His Last Company to the Ground

James Manning, currently Chairman and CEO of SHAZ, previously founded and led Mawson Infrastructure Group (MIGI), a cryptocurrency mining and digital infrastructure company, from its predecessor Cosmos Capital’s founding in 2019 through when he stepped down as CEO of Mawson in May 2023. As with Sharon, the company was launched by reverse-mergering a U.S OTC stock with an Australian firm controlled by Manning. His departure from Mawson, and the events that followed, are extensively documented in federal court and SEC filings that establish an alleged pattern of undisclosed related-party transactions, deliberate information control, and retaliation against corporate oversight.

During his tenure as CEO, Manning constructed a network of affiliated entities through which he routed Mawson funds. The central node was Vertua Ltd, a publicly listed company on a junior exchange in Australia in which Manning is a significant shareholder and director. Beneath Vertua sat multiple operating entities that transacted with Mawson while Manning's interests in them went undisclosed:

Flynt International Cargo Solutions received over A$11.5 million from Mawson between 2021 and 2023 for shipping services the company alleges it did not need. Manning did not disclose his financial interest in Flynt ICS to Mawson's board, nor did he seek board approval for these payments. It was not until late 2023, shortly before his departure as a director, that Manning admitted ownership of Flynt ICS through Vertua's acquisition of the company. When the Mawson board requested details in writing, Manning refused.

First Equity Advisory and First Equity Tax, both owned by Vertua, provided financial and tax advisory services to Mawson. Manning was a director of both entities at the time of the transactions, which Mawson alleges were unnecessary and displaced independent third-party advisors.

Additional entities receiving payments from Mawson under Manning's direction included Defender Asset Management and Manning Motorsports. Mawson's court filings state that Manning's "improper related-party transactions and self-dealing are believed to be substantial and extensive."

Mawson Sued Manning's Vertua Alleging He Negotiated a Lease Between Two Companies He Controlled, Then Invoiced Mawson for Power the Property Was Incapable of Delivering

On March 16, 2022, Mawson's wholly-owned subsidiary Luna Squares LLC entered into a five-year lease for a property in the City of Sharon, Pennsylvania. The landlord was Vertua Property, a wholly-owned subsidiary of Vertua Limited. James Manning was at that time CEO and a director of Mawson and was simultaneously a director and significant shareholder of Vertua. Manning was on both sides of the transaction.

Mawson disclosed the lease in its Form 10-Q for the quarter ended March 31, 2022, in language signed by management. The 10-Q stated that "James Manning, our CEO, a director and a significant shareholder is also a director of Vertua Ltd and has a material interest in the Sharon lease as a large shareholder of Vertua." Mawson's Audit Committee, as disclosed in the same 10-Q, "compared the rent and terms to other arms' length leases we have entered into and formed the view the rent is in line with the market for similar properties." and the directors, other than Manning, were "made aware of the material facts as to Mr. Manning's interest in the lease and authorized us in good faith to enter the lease after determining the lease to be fair to us."

The 10-Q disclosed the economic terms. Base rent in the first year was $240,000, or $20,000 per month. Variable rent was set at "$500 to $10,000 per month" per megawatt of power, "depending on power energized and whether it is available."

The lease was structured around a planned power upgrade. Mawson submitted applications to FirstEnergy, the regional utility, to upgrade the existing transmission lines on the site from 69 kVA and 138 kVA to 40 MVA and 80 MVA respectively. FirstEnergy's load studies, attached as exhibits to Mawson's October 17, 2024 legal complaint, determined that the upgrades were feasible but would require system modifications taking 14 to 18 months to complete. Until those upgrades were finished, the site could support only its existing 69/138 kVA load, less than 0.2 percent of the megawattage the lease's variable rent provisions contemplated.

The Pennsylvania complaint and its exhibits show that Vertua nonetheless began invoicing Mawson an additional $45,000 per month for 90 megawatts of power that the property was not capable of delivering. The $45,000 figure is consistent with the lease's $500-per-MW variable rent provision applied to 90 megawatts. The dispute is therefore not over the rate Vertua charged, but over the quantity of power Vertua billed for. FirstEnergy's load studies establish that the property could not deliver the megawattage that quantity reflected.

The complaint further alleges that Vertua's own subsequent load studies confirmed FirstEnergy's findings, and that Vertua continued invoicing Mawson at the same rate after those findings were known. Across 21 months of invoicing, Vertua overcharged Mawson approximately $925,000 for power the site was physically incapable of supplying. When Luna ceased payments, Vertua terminated the lease and, on April 5, 2024, entered the property without notice or court order and changed the locks. Mawson alleges in the complaint that the lockout caused the collapse of an active commercial agreement with Bitfarms, another publicly traded bitcoin miner that had been in negotiations to become a Luna customer.

Mawson and Luna Squares sued Vertua Property in the Court of Common Pleas of Mercer County on October 17, 2024, alleging breach of contract, wrongful eviction through lockout, overbilling, and tortious interference.

The litigation matters not just for the $925,000 in overcharges, but for what it shows about the disclosed-and-approved related-party process at Mawson. The lease was disclosed in a 10-Q, presented to the Audit Committee, and approved on the express finding that the rent was at market. Eighteen months later, with FirstEnergy's load studies in the record and the property unable to support a fraction of the contracted megawattage, Vertua continued invoicing Mawson for the same unmet capacity.

W Capital Advisors (the fund that later led the involuntary bankruptcy petition against Mawson), Vertua, and Defender Asset Management all shared the same registered address. The registered office for W Capital was previously listed at First Equity Tax's address. Darron Siegfried Wolter, W Capital's Director and Secretary, simultaneously served as CEO of Vertua Opportunities Fund, board member of Vertua, and CEO of Defender Tourism Fund. Court filings describe Wolter as having been affiliated with the Manning family for decades.

Manning negotiated a loan from W Capital to Mawson personally. Other Mawson directors and senior executives were allegedly never permitted to participate in or engage directly with W Capital. W Capital has claimed that Manning promised it at least 1.5 million restricted stock units in Mawson; the company states it has no authorized documentation supporting this commitment.

As Mawson's board and audit committee began investigating Manning's related-party dealings, Manning's response was apparently to obstruct the proceedings. In mid-2023 and again in January 2024, the board formally requested that Manning clarify under oath whether he or related entities held interests in W Capital and its affiliates. Manning refused. In March 2024, Mawson's outside Australian counsel delivered a comprehensive report on Manning's related-party transactions with preliminary discovery requests. Manning again refused to respond.

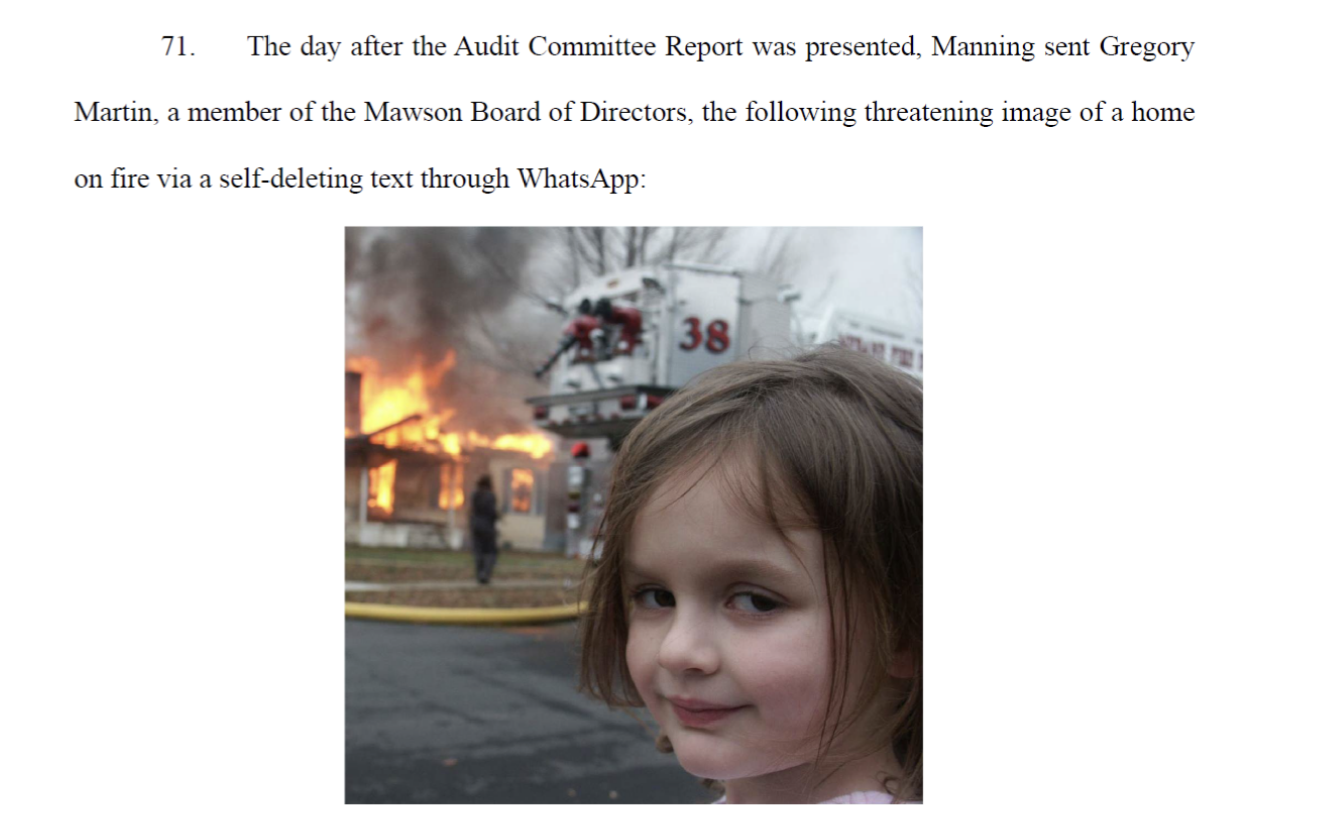

The most revealing moment is documented in Mawson's board minutes from August 17, 2023. Manning informed the board that "he was unwilling to attest to his own related party transactions." Chairman Greg Martin asked Manning to explain how he believed he was properly fulfilling his fiduciary duties. Manning said he would take the question on notice. He resigned six days later.

Following his departure, Manning's posture shifted to active hostility. Mawson's court filings allege that Manning sent a well known meme of a home on fire to board member Greg Martin. Manning told a third party he intended to "burn Mawson to the ground." He explicitly threatened to force Mawson into involuntary bankruptcy if demands for compensation were not met.

Source: Case No. 24-12726-MFW, Bankr. D. Del.

On December 4, 2024, W Capital and two other Australian creditors appeared to carry out Manning’s threat, filing an involuntary Chapter 11 petition against Mawson in the U.S. Bankruptcy Court for the District of Delaware (Case No. 24-12726). The petitioning creditors were W Capital Advisors, Marshall Investments MIG, and Rayra Pty Ltd. Rayra's participation was particularly suspect: it had purchased A$50,000 of Marshall Investments' claim at par just three days after Mawson sued Manning-affiliated Vertua Property in Pennsylvania, and Mawson had never had any prior interaction with the entity. The petitioners did not produce their assignment agreement, required to be filed with the petition, for sixteen days, despite multiple requests from Mawson's counsel.

A U.S. Bankruptcy Judge found sufficient basis to question whether the involuntary petition was filed in bad faith, stating there was "enough smoke" to warrant heightened scrutiny. She ordered the petitioning creditors to post a $1.5 million bond and assessed $204,000 in contempt fines for violating the automatic stay by continuing parallel liquidation proceedings in Australia. The petitioning creditors subsequently moved to dismiss their own petition, and on October 21, 2025, the court dismissed the involuntary petition with prejudice, expressly preserving Mawson's right to pursue attorneys' fees, costs, damages, and punitive damages. Mawson filed an adversary complaint on December 30, 2025, alleging the coordinated campaign caused a one-day market capitalization loss of approximately $23 million.

Manning Has a Documented History of Overpromising at His Public Companies. At Mawson, He Guided to Bitcoin Mining Capacity He Never Came Close to Delivering

Manning's guidance history at Mawson followed a persistent pattern of overpromising and underdelivering. Through 2022 and into 2023, he repeatedly set aggressive capacity targets for Mawson's Bitcoin mining business, each one more ambitious than the last, and Mawson never reached any of them.

In January 2022, Manning told investors Mawson's self-mining operation was running above 1.0 exahash (the industry's standard measure of Bitcoin mining throughput) and would scale to 5.0 exahash by early Q1 2023. In March 2022, with self-mining at approximately 1.35 exahash, Manning upgraded the guide to 5.5 exahash by early Q1 2023. By October 2022, Manning broadened the framing to combine self-mining and hosting capacity, and adjusted the story again, guiding to 4.5 exahash by Q1 2023 but with 8.0 exahash by Q4 2023.

Mawson met none of these targets. By the time Manning stepped down as CEO in May 2023, Mawson had not reached any of the capacity targets he had publicly committed to just weeks earlier, on either the self-mining or combined basis, with less than two thirds of the Q1 2023 targets reached.

We believe the same pattern is unfolding at SharonAI today. Manning is currently telling Wall Street that SharonAI will have approximately 70 megawatts of capacity by the end of Q1 2027. The company has roughly 2 megawatts connected today. Delivering on guidance would require SharonAI to deploy 35 times its current operational footprint in approximately eight months, in a market where NVIDIA's Blackwell GPUs are reportedly backlogged by 3.6 million units, with allocation likely flowing first to established hyperscaler operators.

Manning has promised hypergrowth before. He did not deliver then, and we do not believe he will deliver now.

The Mawson Cash Cycle: Raise, Order, Underdeliver, Offload

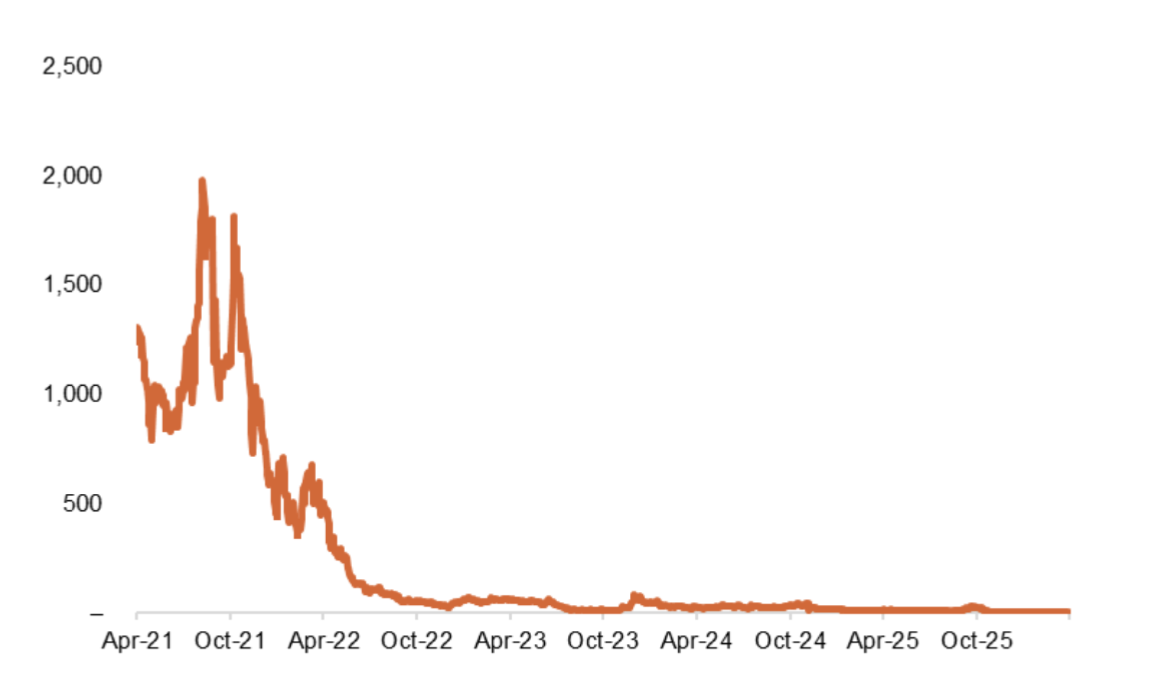

We believe other aspects of the Mawson pattern are being repeated at SharonAI. Mawson raised approximately $100 million from public market investors in 2021 against pledges to purchase industry-leading bitcoin mining hardware (does this sound familiar yet?). Mawson never took delivery of the full quantity it ordered, sold a substantial portion of what it did receive at steep discounts, and pivoted away from the underlying business before the equipment had been on its balance sheet long enough to generate the promised revenue.

In 2021 Mawson raised approximately $100 million across three separate financings: a $20 million pre-IPO convertible note, approximately $40 million in a PIPE financing in August 2021, and a $40 million IPO completed in September 2021. Each round was marketed to investors on the same premise: that Mawson would use the proceeds to purchase next-generation ASIC miners, primarily from Canaan (CAN), and scale rapidly toward 5.0 exahash by early 2023, and become a leading bitcoin miner.

On February 5, 2021 a Mawson subsidiary entered into a Long-Term Purchase Contract with Canaan for 11,760 next-generation Avalon A1246 ASIC Miners, with a total purchase price of $33.9 million. On August 9, 2021, Mawson entered into a second Long-Term Purchase Contract with Canaan for an additional 17,352 next-generation Avalon A1166 and A1246 miners at an average unit price of $4,908, for a total purchase price of $73.6 million. Combined, Mawson disclosed approximately $107 million in committed Canaan purchase orders for 29,112 miners across the two contracts.

James Manning was ebullient in Mawson’s Q3 2021 Earnings Call that November:

“We are in a strong position to not only deliver the 3.35 exahashes contracted to date, critically, we have the underlying infrastructure in place to take this to 5 exahashes and beyond. As previously disclosed, we have now purchased over 40,000 ASIC Bitcoin Miners, which get the 3.35 exahashes by Q2 2022. We’ve purchased over 200 modular data centers and over 100 transformers. This provides us with the infrastructure to scale beyond 5 exahashes.”

Mawson did not receive what it reported as ordered. Mawson's 2021 10-K disclosed that Canaan delivered 8,232 miners in 2021, with $30,799,440 paid against the contract that year.

In Mawson's Q2 2022 10-Q, management disclosed that the second Canaan order had been fulfilled at 11,000 miners, 4,000 fewer than the 15,000 ordered. Despite the shortfall, Canaan refunded only $0.3 million.

In total Mawson paid ~$5,250 on average for 19,232 miners. This was roughly half the 40,000 miners management previously claimed to have purchased on the Mawson Q3 2021 earnings call. You’ll never guess where the miners they did get ended up.

In July 2022, only months after receiving its final Canaan shipment, Mawson management inexplicably decided to exchange 2,144 of its premium ASIC miners for a 33 percent equity stake in Tasmanian Digital Infrastructure ("TDI"), an Australian bitcoin mining venture. By the time Mawson filed its 2023 10-K, the entire TDI investment had been written off. Mawson was no longer mining bitcoin in any meaningful capacity at that site. TDI also seems to have vanished with little trace after early 2023.

Two of the Mawson executives who participated in the TDI site visit, Nicholas Hughes-Jones and Tim Broadfoot, are now senior officers at SharonAI. Hughes-Jones is one of the three Manning-affiliated insiders who sold SAIPL and DSS into the SharonAI public shell. Broadfoot is SharonAI's CFO.

Also in 2022, Mawson sold an additional 6,468 ASIC miners to CleanSpark for approximately $9 million. Combined with the TDI exchange, Mawson disposed of 8,612 miners for an implied average recovery of approximately $1,050 per unit, an 80 percent discount to the average price Mawson had paid months earlier.

Mawson Long-Term Stock Chart

The Same Cycle Has Now Begun at SharonAI

SharonAI has raised approximately $325 million across the December 2025 convertible note, the February 2026 IPO, and the Texas Critical Data Centers sale. Per management's forward outlook, those proceeds are committed against pledges to deploy more than 20,000 NVIDIA B200 and B300 GPUs by year-end 2026, an approximately 35x increase over SharonAI's roughly 2 megawatts of currently connected operational footprint. Manning has previously marketed exponential business growth, based on premium hardware purchase orders, only for investors to be left with incomplete orders, unaccounted cash drain, and jarring business pivots.

SharonAI's Insiders and CEO Are Recreating the Mawson Playbook: Same Entities, Same Insiders, Same Related-Party Structures

The same entity that Mawson identified at the center of Manning's alleged self-dealing scheme appears as a vendor in SharonAI's own SEC filings. The same two individuals who served in senior roles at Mawson now sit alongside Manning at SharonAI with supervoting control. And the same pattern of undisclosed-interest transactions that the Mawson board tried to investigate has been recreated at SharonAI, this time with formal disclosure but the same economic substance.

In its January 2025 court filing, Mawson alleged that Manning caused the company to pay approximately A$11.5 million to Flynt International Cargo Solutions for shipping services Mawson "did not need," without disclosing his financial interest in Flynt. Manning was alleged to have concealed his ownership of Flynt, held through his Vertua vehicle, until late 2023, and to have refused to provide the board with documentation when asked.

Flynt is now a disclosed vendor of SharonAI. The Certain Relationships and Related Person Transactions section of SharonAI's prospectus states plainly: "During 2024, the Group paid storage services expense to Flynt ICS Pty Ltd ('Flynt'). Flynt is a subsidiary of Vertua Limited and affiliated to the Group through common ownership by James Manning. For the year ended December 31, 2024, the Group paid Flynt $167,638 in services expenses."

The key fact is that the same entity Mawson accused Manning of using to funnel out A$11.5 million is doing business with the company Manning now runs. The board that approved this arrangement is a board Manning controls, alongside two individuals who followed him from Mawson and Vertua.

SharonAI's Foundational Acquisitions Were Definitionally Self-Dealing

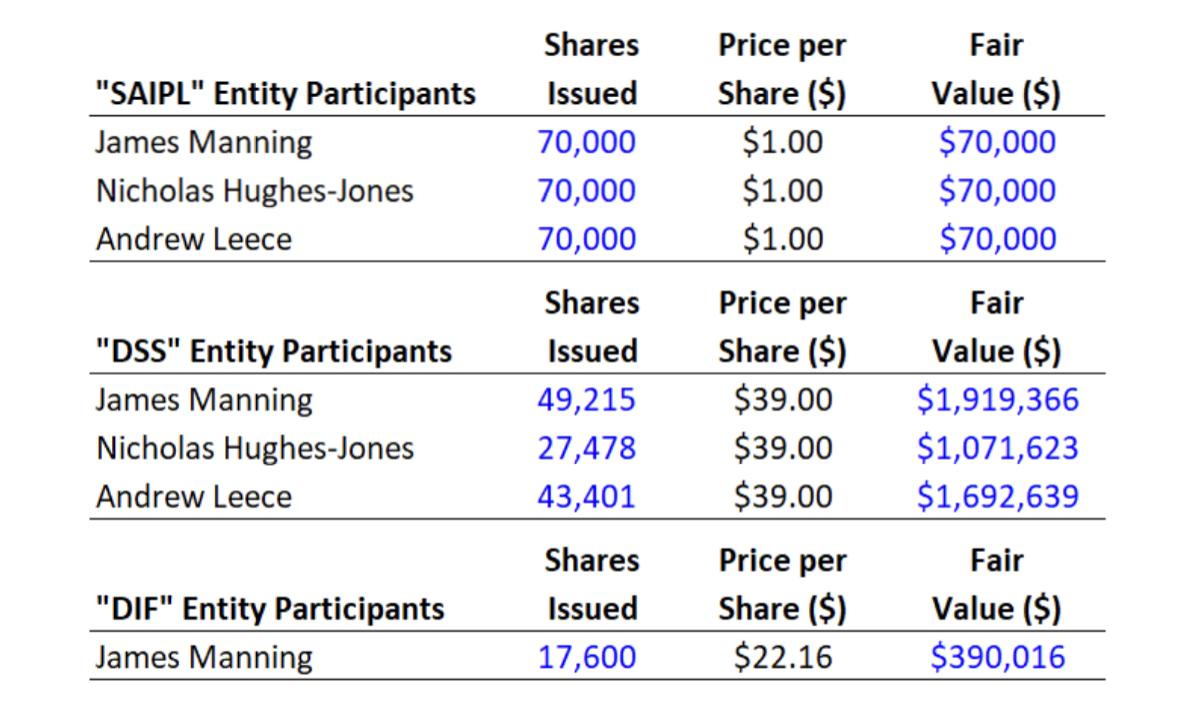

SharonAI was incorporated in Delaware on February 15, 2024. Within approximately four months, it had acquired the two Australian entities that now constitute its operating business, SAIPL and DSS. In both transactions, the selling shareholders were Manning, Nicholas Hughes-Jones, and Andrew Leece. Additionally, Manning was a unitholder of the Digital Income Fund (DIF), a separate Australian entity whose assets were also sold into SharonAI upon its liquidation.

The prospectus discloses the three sellers receiving SharonAI shares for their stakes, summarized below:

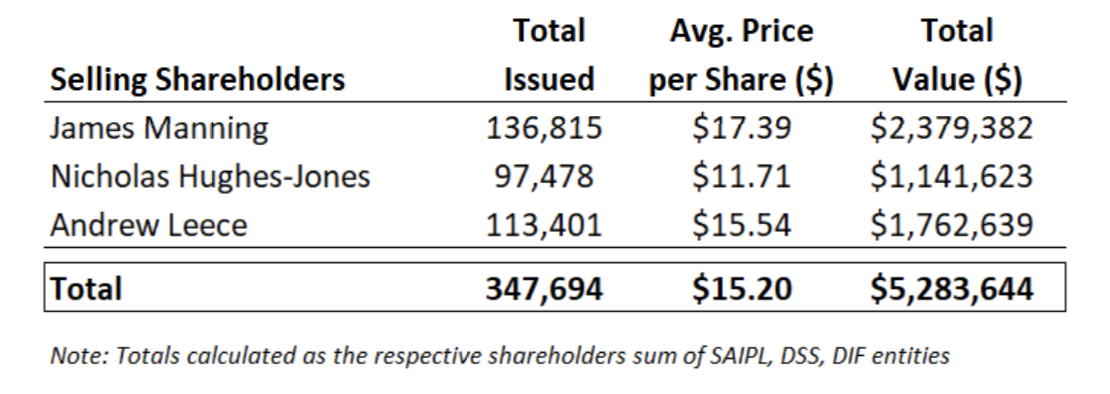

Adding up the disclosed consideration, insiders got $5.3 million in SharonAI stock: Manning received ~$2.38 million across SAIPL, DSS, and DIF. Hughes-Jones received ~$1.14 million, and Leece received ~$1.76 million:

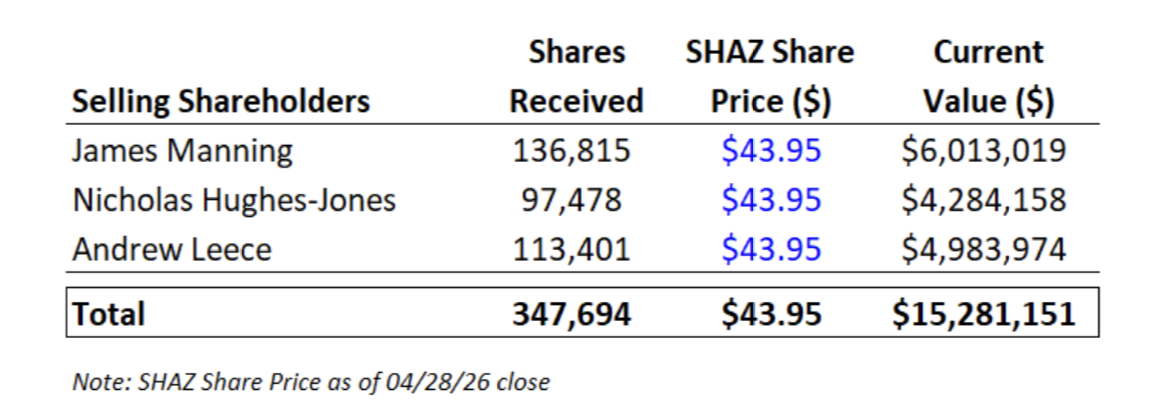

Those shares today are worth ~$15.3 million between the three principals:

These were not arm's-length acquisitions. SharonAI had no independent directors, no operating business, and no meaningful cash when the three insiders sold their private Australian entities to it in exchange for stock whose fair value they themselves, as the controlling shareholders, determined.

SharonAI's $25 Million Acquisition of DSS Was a Round-Trip Through a Manning Vehicle That Marked the Same Asset at Zero Nine Months Earlier

James Manning has been Managing Director and CEO of Vertua Limited since 2013, a position he has held continuously throughout his tenure as CEO of Mawson Infrastructure Group from March 2021 to May 2023 and his current tenure as Chairman and CEO of SharonAI.

Manning's role at Vertua is disclosed in Vertua's annual reports and management page, and on SharonAI's biographies page. Manning is also a Vertua shareholder through Manning Capital Holdings Pty Ltd, which Vertua's FY2022 annual report identifies as "a shareholder of the Group and a related party." Vertua is the holding vehicle through which Manning operates a network of related entities including Defender Asset Management (which Manning chairs), Fiducia Property Group, the Vertua Opportunities Fund, and First Equity Advisory and First Equity Tax. Vertua's registered address is the same address Mawson's court filings identify as shared by W Capital Advisors and Defender Asset Management.

When Vertua marks an asset on its balance sheet, Manning marks it. When SharonAI buys an asset from Vertua, Manning is on both sides of the transaction.

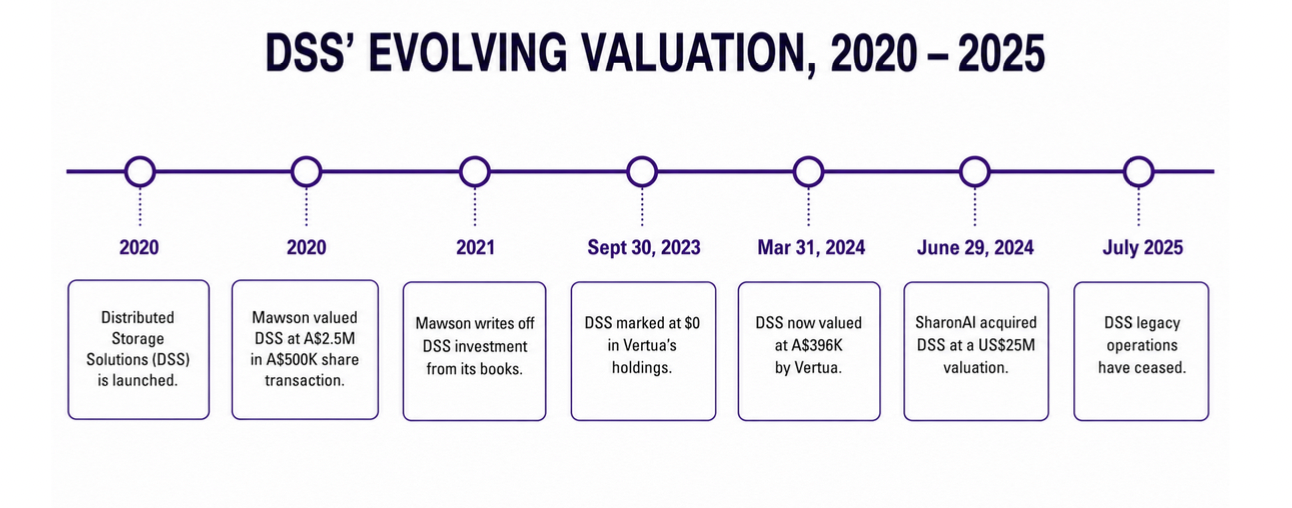

The clearest single example of how the Mawson playbook has been transplanted to SharonAI is the June 2024 acquisition of Distributed Storage Solutions (DSS). On July 9, 2024, SharonAI issued a press release announcing it had "acquired Distributed Storage Solutions Ltd ('DSS') for US$25M." The release described DSS as bringing "strategic relationships with Lenovo and Nvidia, as well as a highly experienced operational team with over 15 years of data center operations and energy infrastructure management experience." The transaction consideration was paid entirely in SharonAI common stock, valued by SharonAI itself.

The recipients were the three insiders selling DSS into the shell: Manning, Hughes-Jones, and Leece, plus Vertua. Per SharonAI's prospectus disclosures, Manning received approximately $1.92 million in SharonAI stock, Hughes-Jones received approximately $1.07 million, and Leece received approximately $1.69 million. Vertua received $677k.

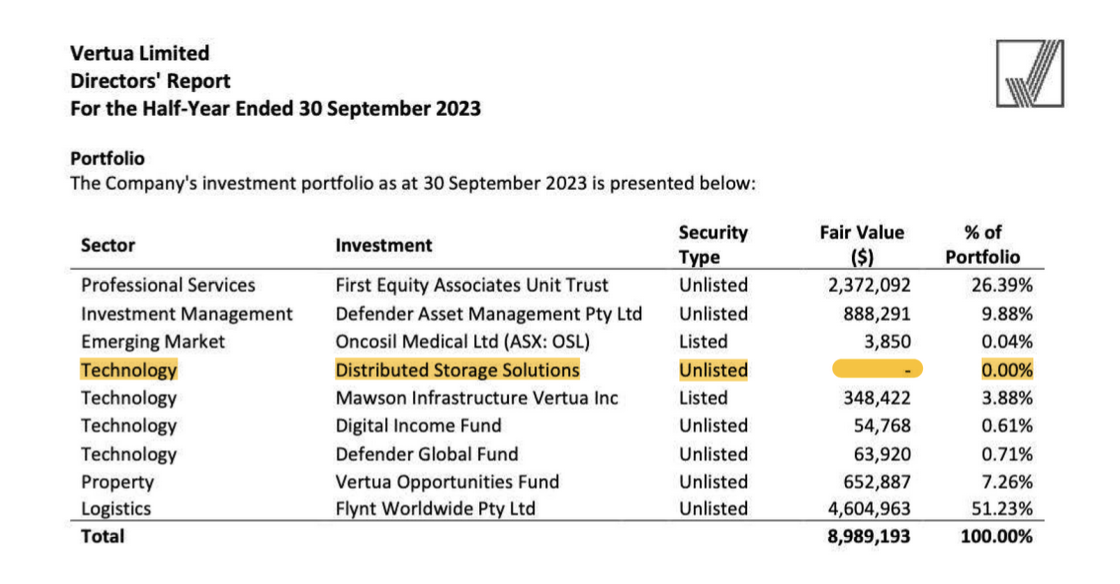

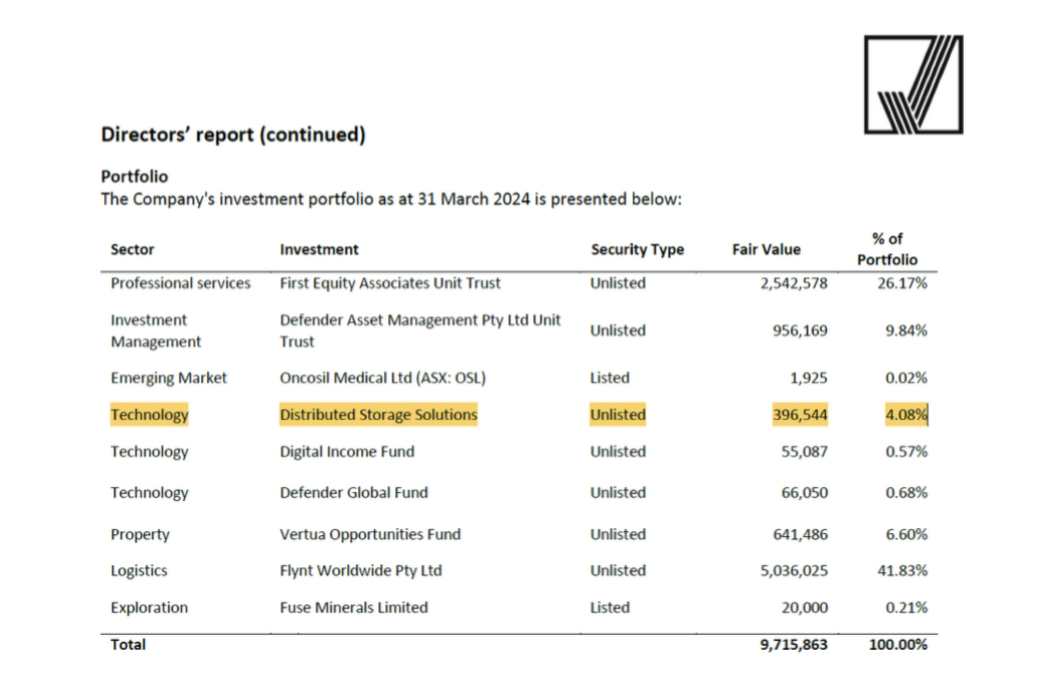

Per Vertua's own filings as of September 30, 2023, Vertua valued DSS at $0:

Then, as of March 31, 2024, Vertua had marked DSS at A$396k:

Ultimately, on June 29, 2024, SharonAI acquires DSS at a US$25 million valuation, handing Manning and Vertua an ~860% return:

In nine months, an asset Manning's own public vehicle had marked at zero was sold to a different public shell Manning controlled at a $25 million valuation. The buyers and sellers were the same people. SharonAI had no independent directors, no operating business, and no independent valuation of DSS at the time of the acquisition.

The relevant question is what changed about DSS's underlying business in the nine months between Vertua's zero mark and the $25 million sale. The publicly available record does not identify a transformation. DSS was, per third-party coverage of the SharonAI acquisition, "an Australian Filecoin storage provider." Filecoin is a decentralized storage protocol whose token had declined approximately 80 percent from its early 2022 peak by mid-2024. The Filecoin storage business does not rely on NVIDIA GPU infrastructure or Lenovo enterprise hardware in any economically meaningful way; it relies on commodity storage and the Filecoin protocol's reward economics.

What did change in that nine-month window was the existence of SharonAI itself. SharonAI was incorporated in Delaware on February 15, 2024. Within four months, it had acquired SAIPL on April 29, 2024 and DSS on June 29, 2024 from the same three Manning-affiliated insiders, in transactions valued by those insiders themselves. The DSS valuation moved from zero to $25 million in lockstep with the existence of a buyer the sellers controlled.

The July 9, 2024 acquisition press release marketed the DSS purchase as bringing "strategic relationships with Lenovo and Nvidia" to SharonAI. By June 9th, 2025 SharonAI had made the decision to cease participation in operations in the DSS business, the Filecoin ecosystem, to focus on GPUs.

Summarizing all of the above, we see the Mawson-to-Vertua-to-DSS arc is a closed loop:

Manning ran Mawson. Manning runs Vertua. Vertua marked DSS at zero in September 2023. Manning, Hughes-Jones, and Leece incorporated SharonAI in February 2024. SharonAI acquired DSS from Vertua and the three principals in June 2024 for $25 million in stock the buyers themselves valued, paid to themselves.

Insiders Cash Out Via Additional Consulting Agreements for the Same Individuals

In addition to their equity consideration and executive compensation, Manning and Hughes-Jones have layered consulting agreements on top of their employment:

Manning Group Office Trust, a Manning-controlled entity, receives AUD$334,500 annually, approximately $211,000, from SharonAI for "commercial opportunity development, discovery of future data center sites, future data center acquisition and construction advisory, transaction advisory services and key relationship introduction and development." This is in addition to Manning's AUD$200,000 CEO base salary.

Inbocalupo Consulting, a Hughes-Jones entity, receives AUD$133,800 annually, approximately $84,000, for "business development services", in addition to his employment compensation.

Broadfoot Group, controlled jointly by SharonAI's CFO Timothy Broadfoot and his wife Mrs. Broadfoot, receives AUD$111,500 annually, approximately $80,000, for "Chief Financial Officer support and executive assistant services to the CFO." In other words, the CFO himself is engaged through a consulting entity rather than directly as an employee. The CFO's wife is also included in that entity's scope of services. This is the officer who signs SharonAI's financial statements.

To summarize:

The same CEO who was accused under oath of routing $11.5 million AUD through an entity he secretly controlled to enrich himself at his last public company is now running SharonAI.

That same entity, Flynt ICS, is disclosed as a vendor of SharonAI.

The same CEO controls SharonAI alongside two other individuals who followed him from his prior companies, via a supervoting class that gives them 65% of the votes against only 1% of the shares.

Every one of SharonAI's "foundational acquisitions" was a sale by those same three insiders of entities they owned into the public shell, for stock they themselves valued.

The CEO, the Head of Business Development, and the CFO all receive additional consulting fees through entities they control, on top of their employment compensation.

The Mawson board took three years to unwind what was happening and eventually sued Manning for it. SharonAI's public investors have been exposed to the same structure since the SPAC closed, with the same CEO, the same affiliated entities, and now a supervoting structure that prevents them from voting him out.

SharonAI Misrepresented Its Relationship With NVIDIA in Its 10-K and Was Forced to Correct It Two Weeks Later

On March 31, 2026, SharonAI filed its 10-K for the fiscal year ended December 31, 2025. The filing, signed by CEO James Manning, told public market investors that "NVIDIA is a strategic shareholder in SharonAI."

The filing was submitted the same day SharonAI announced the $1.25 billion ESDS contract and published its forward outlook to investors. The representation that NVIDIA was a strategic equity holder, deployed alongside the announcement of a transformative customer contract and addition of up to 70MW of compute in the next twelve months, formed a single coordinated package presented to the public market on a single day.

The representation was not true. Thirteen days later, on April 13, 2026, SharonAI filed a Form 8-K under Item 8.01, signed by Manning, stating:

"SharonAI Holdings, Inc. (the 'Company') is hereby correcting a statement included in its Annual Report on Form 10-K for the fiscal year ended December 31, 2025, and filed on March 31, 2026 ('Form 10-K'), which stated that 'NVIDIA is a strategic shareholder in SharonAI.' That statement was included in error. NVIDIA Corporation was not a strategic shareholder in the Company and as of the date of this Current Report, NVIDIA Corporation does not hold any equity securities of the Company."

NVIDIA was not a strategic shareholder when the 10-K was filed. NVIDIA had never been a strategic shareholder. The 10-K was not amended. The single representation that NVIDIA was a strategic equity holder was withdrawn in isolation, two weeks after a market that had been told otherwise had absorbed and traded on the announcement.

The misrepresentation tells investors something specific about how management characterizes the NVIDIA relationship when no one is checking. SharonAI is a certified NVIDIA Cloud Partner (NCP), a technical designation it shares with two other Australian operators. NCP status confers access to reference architectures, technical guidance, and customer referral channels. It does not confer equity. It does not confer capital. It does not automatically confer priority allocation, despite management claiming “Preferential GPU Access”, in a Blackwell market reportedly backlogged by 3.6 million units, where NVIDIA likely allocates first to established hyperscalers or buyers with the largest purchase orders and firm financing.

SharonAI's own 10-K describes the certification as having been earned in December 2024 by "completed testing using older models of NVIDIA GPUs to demonstrate that it could successfully deliver HPC use cases under NVIDIA reference architecture." That is the actual relationship. A vendor relationship, validated on prior-generation hardware, shared by two competitors in the same country.

The Cash Out Begins: Lucid Initiated Coverage With a Buy on the Same Day SHAZ Filed to Register One-Third of the Float for Resale, With Lucid Itself Among the Sellers

On April 17, 2026, Lucid Capital Markets initiated coverage of SharonAI with a Buy rating and a $50 price target. The same day, SharonAI filed a Post-Effective Amendment (POS AM) to its January 2026 resale registration statement, naming the specific selling shareholders and the share counts each was registering. The SEC declared the registration effective on April 21, 2026, and the named sellers are now free to sell into the market.

Lucid is among them. Lucid Capital Markets is registered to sell 41,667 shares, worth approximately $1.5 million at current prices. Lucid's Head of Capital Markets, John Lipman, is registered to sell 465,343 shares, worth approximately $16.7 million. Lipman's position originated in his prior role as co-CEO of Roth CH Acquisition Co., the SPAC that merged with SharonAI in December 2025. Lucid's own initiation report discloses that the firm has received investment banking compensation from SharonAI and expects to receive further compensation within the next three months.

In other words, the bank that led the Nasdaq uplist initiated with a Buy on the same day its own Head of Capital Markets registered his entire SHAZ position for resale, while disclosing it expects to be paid more banking fees by the company in the coming weeks.

The April 26 Oaktree convert extended the founders' own lockups, Manning, Hughes-Jones, and Leece, through March 31, 2027 as a closing condition. The non-founder insiders, including the Roth CH SPAC sponsor and the selling shareholders named in the April 17, 2026 Post-Effective Amendment, are not covered by the extension. The founders kept themselves locked up.

Conclusion

SharonAI's public life has spanned four months. In that time, the company has announced a $125 million Nasdaq uplist, a $500 million debt facility from a one-year-old DeFi protocol with $284 million of lending capacity, a $200 million revenue-share facility from Digital Alpha that has not been executed, a $1.25 billion customer contract with an Indian counterparty that earned $5.8 million in fiscal 2025, and a $350 million convertible note from Oaktree that closes only if SharonAI signs a separate binding contract for at least 4,068 GPUs.

Three sell-side firms have initiated Buy ratings on price targets that imply a roughly $3 billion enterprise value. One of those firms is a selling shareholder in the same Post-Effective Amendment.

None of this is a new pattern for James Manning. At Mawson Infrastructure Group, the same CEO guided Wall Street to capacity targets he never delivered, allegedly routed $11.5 million through entities he did not disclose, refused to attest to his own related-party transactions, and now faces allegations in federal court that he orchestrated a bad-faith involuntary bankruptcy against the company he had founded. Two Mawson senior personnel now sit alongside Manning at SharonAI. Flynt ICS, the entity at the center of the Mawson allegations, is a disclosed vendor at SharonAI. The supervoting structure that entrenched Manning at Mawson has been replicated at SharonAI, with the founders holding roughly 65 percent of the votes against 1 percent of the economics.

We believe the ESDS contract cannot perform. We believe the USD.AI and Digital Alpha facilities will not be executed on the terms announced. We believe the sell-side models built on these assumptions will require material revision. The Oaktree convert tells us management agrees: if the announced facilities and the announced contract were sufficient to fund the build, SharonAI would not have signed a $350 million senior unsecured note at 6 percent with a 20 percent conversion premium and a 4,068-GPU closing condition.

The founders, Manning, Hughes-Jones, and Leece, extended their own lockups to March 31, 2027 as a condition of the Oaktree convert. The non-founder insiders, including the Roth CH SPAC sponsor, Lucid, and the other selling shareholders named in the April 17, 2026 Post-Effective Amendment, did not.

We are short SharonAI.

Terms of Use

Use of reports prepared by Bleecker Street Research LLC (“BSR”) and this website is subject to and governed by the below Terms of Use (the “Terms”). The Terms govern all reports published by BSR (each a “BSR Report”) and supersede any prior Terms of Use governing the access and use of this website and BSR Reports, which you may download from this website. By downloading, accessing, or viewing any materials on this website, you hereby agree to the following Terms.

Bleecker Street and Its Related Parties

BSR is under common control and affiliated with Bleecker Street Capital LLC (“BSC”), Bleecker Street Capital Management LLC (“BSCM”), and affiliated funds, including but not limited to Bleecker Street Minerva LP (“Minerva”) and Bleecker Street Partners LP (“BSP”) (collectively, BSC, BSCM, and affiliated funds, including Minerva and BSP, are referred to herein as “BSC”). BSR is an online research publication that produces due diligence-based reports on publicly traded securities, and BSC and BSCM are investment advisers registered with the U.S. Securities and Exchange Commission. The reports on this website are the property of BSR. BSR and BSC, collectively with their respective affiliates and related parties, including, but not limited to any principals, officers, directors, employees, members, clients, investors, consultants and agents, are referred herein to as “Bleecker Street”, “us”, or “we”.

BSR is a for-profit journalistic organization that researches and provides opinion journalism about issues of concern to the general public, including about the securities of public issuers. BSR finances its journalism through a non-traditional revenue model where it earns revenue from positions that BSC takes in the securities of issuers on which BSR reports. This business model requires Bleecker Street to take material financial risk, which our partners have exposure to. To manage risk, we must close open positions as we deem prudent. We do not provide “price targets” for securities, although we may express our subjective opinion of the value of a security, which differs from a price target in that we neither know nor claim to know how the market might value such security. We therefore typically do not hold, and provide no assurance that we will hold, a position in a reported-on security until it reaches a price target, nor do we necessarily hold, or provide any assurance that we will hold, positions in securities until such securities reach the price that reflects our opinion of value. Many factors enter into investment decisions aside from opinions of the value of the security, including without limitation, borrow cost, “short squeeze” potential, risk sizing relative to capital and volatility, reduced information asymmetry, the opportunity cost of capital, client expectations, the ability to hedge market risk, our perception of the efficacy of market regulators and gatekeepers, our perception of the resource imbalance between us and any Covered Issuer (defined below), and our subjective perceptions. Therefore, you should assume that upon publication of a report, we will, or have begun to, close a substantial portion – possibly the entirety – of our positions in the Covered Issuer’s securities.

Reports Are Solely Attributable to BSR

The BSR Reports on this website are opinion journalism. On this website and through the BSR Reports, BSR is providing its journalistic opinions about issues of concern to the general public. You understand and agree that the opinions, information, and reports set forth on this website are attributable only to BSR, which bears sole responsibility for the information on this website and content of the BSR Reports; provided, however, that persons affiliated with Bleecker Street have provided BSR with publicly available information that BSR has included in the BSR Reports and on this website, following BSR’s independent due diligence.

Website and Report Use Is at Your Own Risk

Any and all use of BSR’s research and BSR Reports is entirely at your own risk. Neither BSR nor BSC is liable for any losses or damages you may incur as a result of your use of this website, including but not limited to any direct or indirect trading losses you may incur as a result of any information on this website, any BSR research, or any BSR Report. You agree to do your own research and due diligence with respect to any information on this website, and to consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities of an issuer discussed on this website (a “Covered Issuer”).

BSC’s Trading Practices and Positioning with Respect to Covered Issuers

As of the time and date of each report, BSC (defined below) is short the securities of, or derivatives linked to, the securities of the Covered Issuer, unless otherwise stated in the report. BSC therefore will realize significant gains in the event that the prices of a Covered Issuer’s securities decline. Upon the publication of each report, we may cover, and typically will cover, a substantial majority of our short positions. BSC’s covering its short positions upon the publication of a report is not a reflection of a lack of conviction in any opinions or the facts presented on this website or in any BSR Report. Rather, the act of covering BSC’s short positions upon the publication of a BSR Report is intended solely to manage risk in a prudent manner, consistent with the obligations of a fiduciary of our investors’ money. BSC are likely to continue transacting in the securities of Covered Issuer for an indefinite period after a report on a Covered Issuer, and we may be net short, net long or neutral positions in the Covered Issuer’s securities after the initial publication of a report, regardless of our initial position and views herein.

Notice to UK Residents

If you are in the United Kingdom, you confirm that you are accessing research and materials as or on behalf of: (a) an investment professional falling within Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”); or (b) high net worth entity falling within Article 49 of the FPO (each a “Permitted Recipient”). In relation to the United Kingdom, the research and materials on this website are being issued only to, and are directed only at, persons who are Permitted Recipients and, without prejudice to any other restrictions or warnings set out in these Terms of Use, persons who are not Permitted Recipients must not act or rely on the information contained in any of the research or materials on this website.

No Recommendation or Solicitation; No Warranties

All information and opinions on this website and in BSR Reports are for informational purposes only. You understand and agree that no information on this website or in any BSR Report is investment advice or a recommendation or solicitation to buy securities. In any given BSR Report, BSR is solely articulating its reasons at the time of publication for the positions it may have in the securities of a Covered Issuer. To the best of BSR’s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities of a Covered Issuer or who may otherwise owe any fiduciary duty or duty of confidentiality to the Covered Issuer. However, such information is presented “as is,” without warranty of any kind, whether express or implied. BSR makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition, and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets, and liabilities. Such statements, estimates, projections, and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond BSR’s control. All expressions of opinion are subject to change without notice, and BSR does not commit to update or supplement any BSR Report or any of the information contained therein.

All Materials Copyrighted; Permitted Sharing

The information on this website, including but not limited to BSR Reports, are copyrighted and the intellectual property of BSR. You agree not to distribute any of the information on this website, whether as a downloaded file, a copy, an image, a reproduction, or a hyperlink to such file, in any manner other than by providing the following hyperlink: bleeckerstreetresearch.com. If you have obtained research published by BSR in any manner other than by downloading a file from the foregoing link, you hereby are on notice of these Terms, agree to these Terms, and agree not to use such research in a manner inconsistent with these Terms.

You further agree that you will not communicate or distribute the contents of BSR Reports and any other information on this site to any other person unless that person has agreed in writing to be bound by these Terms. You understand and agree that if you access this website, download or receive the contents of BSR Reports or other materials on this website as an agent for any other person, you are binding your principal to these Terms.

Limitation of Liability; No Special Damages

Bleecker Street shall not be liable for any claims, losses, costs, or damages of any kind, including direct, indirect, punitive, exemplary, incidental, special or consequential damages, arising out of or in any way connected with this website or the BSR Reports. This limitation of liability applies regardless of any negligence or gross negligence of Bleecker Street. You accept all risks in relying on the information and opinions in any report on this website.

Governing Law; Jurisdiction; Arbitration

You agree that any dispute between you and Bleecker Street arising from or related to these Terms, the information on this website, or any BSR Report shall be governed by the laws of the State of New York, without regard to any conflict of law provisions. You knowingly and independently agree to submit to the personal and exclusive jurisdiction of the state and federal courts located in New York, New York and waive your right to any other jurisdiction or applicable law. You agree that any dispute between you and Bleecker Street arising from or related to these Terms, the information on this website, or any BSR Report shall be brought exclusively in binding arbitration conducted in New York, New York by JAMS, before a single arbitrator, under the applicable JAMS rules. You agree that you waive the right to a trial by jury in any action or proceeding in any jurisdiction between you and Bleecker Street.

No Waiver; Validity

The failure of Bleecker Street Research LLC to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to the foregoing governing law and jurisdiction provision.

One-Year Limitations Period

You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to the use of this website or the material herein must be filed within one year after such claim or cause of action arose or be forever barred.