Dave, Inc (DAVE): 100% Downside Possible As The Regulatory Heat Turns Up The Heat On This Lender

Key Points:

DAVE is a predatory payday lender masquerading as a consumer-friendly fintech that protects its users from excessive overdraft charges. However, the company faces several critical threats to its model.

DAVE provides “advances,” averaging ~$150 in size, to customers. To access the money immediately, customers must pay fees, and then are put into a “dark pattern” and heavily encouraged to “tip” DAVE.

To access money immediately (the need state of DAVE customers), customers pay a fee ranging from $5 to $25 on a max advance of $500. If a user pays a $5.99 express fee on a $100 advance and tips DAVE 15%, these work out to loan-shark APRs.

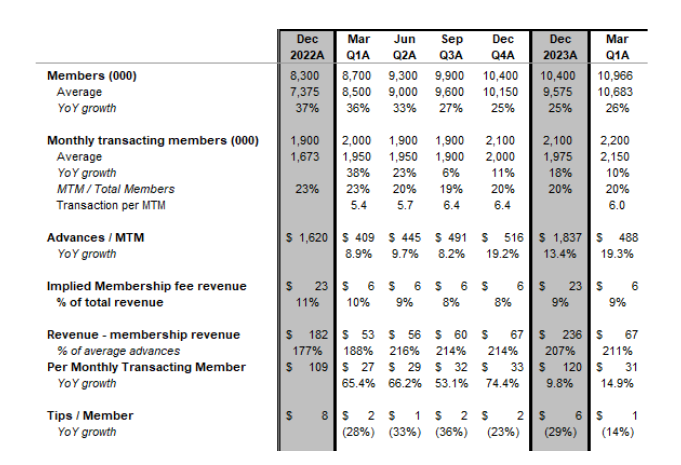

To charge such APR’s, DAVE makes tipping “optional.” Members have wised up to the tip scheme and users stop tipping over time. In Q1 2024, tips revenue grew only 8%, while processing fees and advances grew 35%. Tips per member fell 14% year-over-year.

Tipping comprised 22% of 2023 revenue. We estimate that tipping generated contribution profits of $42m. Without tipping we estimate that DAVE would have ($84M) in EBIT losses, compared to the ($42M) of losses it reported.

DAVE is reliant on a single bank partner for both its lending and neobanking business. That bank partner, Evolve Bank & Trust, was hit with a wide ranging Consent Order for its discriminatory lending processes, served as the primary banking partner for many crypto frauds, and was hacked in a ransomware attack which may lead to the dissolution of the bank.

DAVE is in the hot seat after the CFPB released trial rules interpretations against earned wage access (EWA) providers, specifically calling out tips. While Dave argued it was outside the scope of this regulation, if it looks like a duck, and quacks like a duck….

We believe DAVE is worth $0 to $10/ share, implying 70% to 100% downside.

Disclosure: Bleecker Street is short DAVE, please see our full disclosure at the end of this report.

How Dave Makes Money

Dave provides “advances” (which could be construed as “loans”) to customers (or “Members”) that average $151 apiece. This product is called ExtraCash, which Dave claims is a product to prevent bank overdraft fees.

Dave charges users fees to access this money immediately, and then offers customers the option to TIP it, with a default tip setting of 15%. There are also fees for getting cash instantly (which is the need state for Members). These fees range from $3 to $25 on a maximum advance of $500. Let’s use an example from a recent lawsuit alleging these excess fees are interest.

A member is advanced $100, is charged a $5.99 “express fee,” and tips Dave 15%. That’s $21 on a $100 advance that needs to be taken out of your next paycheck in two weeks (along with $100 to retire the advance).

For each of these advances, Dave generates nearly $11 in revenue. However, that advance is due in two weeks, generally, for a 7% return to Dave. Do the IRR math on that and you’ll find it annualizes to just under 500%.

The above-mentioned complaint alleges an annual percentage rate (APR) of 560%, which merely multiplies the two-week return of 21% by ~27 non-compounding periods in a year.

Either way, these are within the zone of rates charged by payday lenders in the United States.

Tips Are A Massive Profit Driver For Dave, The CFPB Is Taking Aim

In addition to the fees that members must pay to access money immediately, all users are taken to a screen after receiving an advance, where users are offered to tip Dave. These tips are often tied to feel good things, like providing meals to the homeless or planting trees (more on that later).

But who tips their bank, their credit card lender, or their student loan providers? The “option” is a default setting in the app wherein the Member pays a 15% “tip” on the cash advanced to them. Members are fed numerous psychological stimuli to get them to pay and let the option run (screenshot source: LA Times).

Dave gets away with this because the “tips” are technically optional, while the fees to access the money immediately are not, and immediate capital is the need state of the DAVE user.

This is called a “dark pattern.” Members can opt out of tipping Dave, but the emotional cues are strong. Many Members apparently read the contract just as carefully as most of us have read the Terms of Service pop-ups on sites like Facebook. These are people who are in a hurry to get cash, now.

Tips comprised 22% of 2023 revenue. We estimate tips generated contribution profits of $42M to the 2023 EBIT loss of $42M (so in other words, EBIT would be negative $84M without tip income).

Members also pay a monthly fee of $1 to be on the Dave platform. Dave doesn’t discuss this in detail in its SEC filings and doesn’t use the term “Membership Fee” in its most recent 10-K or in its S-1 registration statement. Our discussions with former employees indicate this is a very high margin component of revenue with very few variable costs attached. Even though this was likely over 10% of revenue at the time of the IPO and very likely the second-largest profit contributor to the company, this item is seldom discussed.

CFPB Regulation Could Destroy Dave’s Model

On July 18, 2024 the Consumer Financial Protection Bureau proposed an interpretive rule which could blow up Dave’s business model, it specifically called out “the unusual practice of workers ‘tipping’ their lender or employer.”

The CFPB’s proposed rule would treat paycheck advance products (the EWA products Dave was founded on) as a consumer loans. The CFPB specifically said “some of these products can come with fees for expedited service, subscriptions, or requested “tips.” Specifically, the CFPB believes that “tips” and other fees for expedited delivery should “meet the Truth in Lending Act’s standard for being finance charges.”

CFPB Director Rohit Chopra also specifically called out tipping in his prepared remarks, and noted that the CFPB recently sued a lender for deploying “dark patterns” in its tipping page, which resulted in consumers almost always paying at least one fee.

Dave issued a same-day response to the matter, claiming that the company’s ExtraCash product is protection from overdraft fees, not earned wage access.

“We are closely monitoring the recently proposed interpretive ruling from the CFPB around paycheck advance and earned wage access (“EWA”), a model which Dave was originally founded on, but transitioned away from beginning in 2022 due to a lack of certainty around the regulations,” said Jason Wilk, Founder and CEO of Dave. “Dave’s ExtraCash product is structured as a bank-originated overdraft with optional fees, which combats the excessive fees found at incumbent banks. As a result, we believe ExtraCash and our optional fees sit within the overdraft regulatory framework that is distinguished from EWA and paycheck advance products.”

While Dave argues that its ExtraCash product is “structured as a bank-originated overdraft with optional fees, which combats the excessive fees found at incumbent banks,” the CFPB specifically called out Dave in its list of examples of EWA providers.

And while Dave might say that its product is overdraft protection, it also specifically mentions in marketing that its product can be used to get early access to payroll.

Even a sell-side note from B. Riley, which initiated Dave as a buy in June would seem to suggest that Dave’s product should be considered an earned wage access product.

The CFPB also recently sued a lender for deploying “dark patterns” in their tipping practices, something that many argue Dave does. The CFPB argued that SoLo, another Los Angeles-based non-bank lender, was using so-called dark patterns to trick users into tipping it. The CFPB alleged:

“SoLo’s use of dark patterns ensures that almost every borrower pays a fee, in the form of a “tip” or “donation.” The CFPB is seeking, among other things, injunctions against SoLo to prevent future violations, monetary relief for borrowers, forfeiture of ill-gotten gains, and a civil money penalty. The CFPB is suing SoLo for using digital trickery to hide interest and fees on its online loans,” said CFPB Director Rohit Chopra. “SoLo has had repeated run-ins with state regulators, and we are putting a stop to their fake tipping scheme.”

Dave is extremely reliant on tipping and fees for accessing cash immediately. In Q1’24 Dave generated $74M in revenue with 81% of that revenue coming from tips and processing fees. It would be alarmist to say that could go away immediately. Anything could happen in the upcoming election, including the CFPB getting gutted. The CFPB just presented, however, a very real regulatory risk for Dave that did not exist weeks ago.

Dave was largely unaffected by the ruling, but money lender MoneyLion (ML) fell 25% on the news, and it operates a similar model to Dave.

Dave’s Charitable Donation Scheme Is Misleading: Is It A Meal Donation or $.10?

Charitable contributions as a sales incentive are a potent tool for inducing sales. Numerous states in the US have laws governing this practice, known as a Commercial Co-Venture for fundraising.

Dave’s primary non-profit of choice is Feeding America, which is one of the largest hunger and food bank charities. Feeding America has long used a (somewhat dubious) sales pitch in their own fundraising efforts that one dollar can provide ten meals to a hungry American. This ten cent figure is a portion of the overhead cost associated with managing donated food and is a laughable figure, according to several Feeding America charity and finance professionals we spoke to.

A longtime charitable giving director at one of the largest Feeding America affiliates in the nation told us in an interview that this 10 meals for $1 promotion has sadly “opened the door for shady operators” who seek to partner with the non-profit.

Dave’s commercial co-venture program with Feeding America exploits this murky value proposition. At ten cents per meal, Dave can promise a lofty-sounding donation while soliciting “tips.” Dave’s commercial contract with Feeding America promotes “one meal” per percentage point of tip at loan origination.

Dave’s average cash advance in 2023 was $152. Each percentage point of “tip” that Dave is able to solicit yields $1.52 in high margin revenues. Of that, only ten cents (or 6.5%) is allocated for donation. This plays into Dave’s “dark pattern” tricks.

Don’t take our word for it though. The Better Business Bureau (BBB) updated its “Standards for Charity Accountability” framework in 2021, with one of the major updates including specific language discouraging commercial promotions from using arbitrary non-monetary charitable carrots used for solicitation.

The BBB standard now expects commercial promotions tied to charity to disclose a percentage of sales (rather than “profits”) or a fixed dollar amount. The BBB’s justification for it is self-explanatory:

Unless informed otherwise, donors may believe that much more of the purchase is going to the charity than is actually the case. Transparency helps avoid false assumptions and misunderstandings.

Charitable donations as a vector for harmful anti-consumer practices are likewise a recent hot point for several states, with California, Tennessee and Utah all promoting new CCV regulations in 2024.

We suspect that a change to meeting new standards in-line with BBB alone would cause material harm to Dave tipping revenues and certainly profits. A ten cent donation sounds a lot less impressive than “a healthy meal” to a hungry American.

A Review Of Dave’s Financial Statements: Not a Fintech, But A Balance Sheet Lender With A Credit Problem

In 2023, Dave carried average advance assets of $114M, having made $24M advances totaling $3.6B.

Fees earned = 7.1% of advances, or 227% of average advance assets (annualized). That’s about 7-8x typical interest and fee rates on subprime credit card and auto loans.

You’d think Dave is very profitable with that sort of revenue generation. Not really. It has never generated a yearly profit post-SPAC. Credit losses have historically eaten up all pretax, pre-provision income.

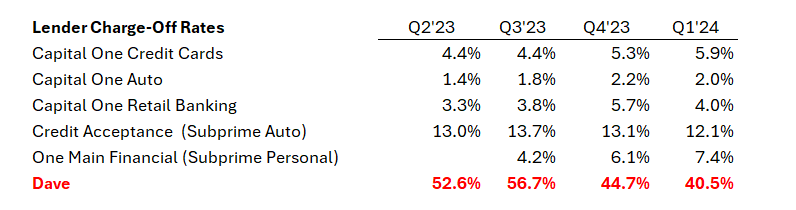

55% of advance receivables were charged off last year and credit loss provisions / revenue were 23%. That’s about 4 - 6x credit losses for subprime credit card and auto lenders.

For comparison, here are the net charge-off rates for other lenders and products lines:

Advances from Dave are typically or always secured by the forthcoming paycheck(s) of the recipient, with those liabilities coming due in 1-2 weeks.

Think of those numbers for a second. Dave can see into your bank account daily and it examines the account history for payroll transactions. One would think credit underwriting with these characteristics on a receivable coming due in two weeks or less would be effective.

To reach charge-offs of this magnitude, we believe credit losses are not at all akin to those attaching to receivables of other subprime lenders. We believe the fraud content in these receivables is sizable, but the low amount of each advance makes it untenable to pursue debtors legally.

In its most recent quarter, Dave’s credit losses ran at 41% of advance receivables (annualized). The company released reserves, so that flattered the income statement and helped to achieve positive net income (though the big credit to income was below the line).

Dave did break into profitability in Q4 2023 and then in Q1 2024 recorded $4M in pretax profit before a gain on the extinguishment of debt. That was after a 9% reduction in processing and servicing costs, a 30% reduction in advertising & marketing, and an 8% reduction in compensation costs, all in 2023. Dave can only sever its entire marketing department once, as they did in 2023, according to former employees.

While net charge-offs declined to “only” 39% (annualized) of average advance receivables in Q1 2024 vs 59% in Q1 2023, the company’s allowance for credit losses / gross advance assets reached a post-SPAC low of 14% at the end of Q1 2024 (high of 21% in Q1 2022).

Dave dumped large chunks of many departments and is on cruise control, according to former employees, with CEO Jason Wilk micromanaging strategy and operations with a very narrow body of bros surrounding him.

In our opinion, based on numerous conversations with former employees, Dave doesn’t know where it wants to take itself, as there’s little chance it leverages its base business into a wide payments platform and as its base business growth will soon be tapped out.

These moves have been necessitated in part by Members getting wise to the “Tips” trick. In Q1 2024, Tips revenue grew only 8% while processing fees and advances grew 35% YoY. Monthly Transacting Members only grew 10% YoY while Tips per member fell 14% YoY. Such a decline is a very unfavorable development for Dave and provides a good indication of the diminishing value returning customers see in this option.

Cutting advertising with receivables falling 8% QoQ in Q1 and running down credit loss reserves do not, as an income statement ensemble, paint the picture of a healthy, growing fintech.

What we do see here is fewer transacting members as a percentage of overall Member rolls. Those members who do transact are transacting more often per quarter, but there comes a point in extractive industries such as gold mining, shale drilling, and deep subprime finance where the deposits get played out. We believe there is high overlap and churn with this firm and others such as MoneyLion.

One former Dave executive told us there is massive disagreement within the company on how to escape its quickly-approaching maturity. The employee characterized internal discussions regarding Dave’s strategic direction as being riddled with “massive friction” and added there is much internal disagreement with the CEO’s desired strategy.

Having penetrated 6.5% of the US workforce, this company is approaching saturation. Addressable subprime is usually 35-40% of the US workforce, so if all subprime were addressable, the company would be at 18% penetration.

Dave’s service appeals to the deepest of subprime customers who have few liquidity choices, though. If the target market is 25% of subprime borrowers, that would indicate Dave has penetrated 70% of its addressable market.

For the coming year, the company is guiding to revenue growth of 18-25% and EBITDA margin of 8-12%. With a high level of addressable market penetration and a declining take rate as a percentage of advance volume, we believe Dave’s model is showing signs of exhaustion.

Like many fintechs, Dave inappropriately uses EBITDA as a key performance indicator and doesn’t even mention anything about net charge-offs / write-offs in its quarterly press release. It does mention delinquency rate, but that’s another vacuous indicator.

If your product, by its very nature, leads to fast defaults and charge-offs, of course delinquencies are going to be low. The cutoff for delinquency rate is 28+ days, which is 2x average loan duration.

In this business model, charge-offs are far more important than delinquencies, by orders of magnitude. It’s no wonder the phrases “charge-off” or their preferred “write-off” have not been uttered on any Dave conference call (according to Bloomberg transcript search). One former executive we interviewed indicated there is no internal agreement on credit KPIs. They also agreed delinquency rates mean little here with such a fast charge-off cycle.

What are you going to talk about, as Dave management? The 1.8% DQ rate or the 48% to 65% net charge-off rate?

This is typical of the games of SPACs of the last five years and, really, most subprime schemes of the last 30 years. They’ll tell you to look here, here, and there, but ignore key performance indicators that are totally standard across financial services companies.

A company whose highest-ever ROE was 12% (Q1 2024, before extraordinary gain) could certainly produce high returns on equity in the future and that is certainly what the current stock price demands at 451% of book value. We just don’t think a high ROE continuing well into the future is a high probability scenario. Therefore book value or a discount to it are completely tenable valuations for Dave.

Looking out five years, we think there is some probability this company gets to $425M in revenue and $3 per share in EPS, implying a 2028 ROE of 11%. If one assumes an 11% cost of equity and negative FCF to get to that continuing value / terminal value state, NPV of equity is zero.

If we stretch out the competitive advantage period another five years, the company may be worth $10 per share. That’s $10 per share if we have a crystal ball that tells us with 100% certainty this won’t be shut down, impaired by regulators, or obviated by other developments such as Earned Wage Access, or EWA.

Inside Dave, wave after wave of team firings has left decision making insular and we are told large cohorts of Dave employees feel what they are doing is extractive and morally empty. There is little trust of the CEO within the company, a former staffer told us. As Intel CEO Andy Grove observed, “Only the paranoid survive.” We see very little sense of urgency at Dave regarding a torpedo that is in the water with sonar active and warhead hot.

The terminal value risk for Dave is far higher than the stock price implies.

Based on numerous valuation approaches and a generous array of scenarios and probabilities, this is just about one of the worst risk-reward propositions we’ve seen in the fintech dumpster fire of the last five years. We are short Dave with a price target of $0 to $10 per share.

Bleecker Street Research LLC Terms and Conditions

By downloading from or viewing material on this website you agree to the following Terms of Service. Use of Bleecker Street Research LLC’s research is at your own risk. In no event should Bleecker Street Research LLC or any Bleecker Street Research LLC Related Person (as defined hereunder) be liable for any direct or indirect trading losses caused by any information on this site. You further agree to do your own research and due diligence, consult your own financial, legal, and tax advisors before making any investment decision with respect to transacting in any securities of an issuer covered herein (a “Covered Issuer”).

As of the publication date of Bleecker Street Research LLC’S report, Bleecker Street Research LLC Related Persons (along with or through its members, partners, affiliates, employees, and/or Bleecker Street Research LLCs), clients, and investors, and/or their clients and investors have a short position in the securities of a Covered Issuer (and options, swaps, and other derivatives related to these securities), and therefore will realize significant gains in the event that the prices of a Covered Issuer’s securities decline. Bleecker Street Research LLC and Bleecker Street Research LLC Related Persons are likely to continue to transact in Covered Issuers’ securities for an indefinite period after an initial report on a Covered Issuer, and such position(s) may be long, short, or neutral at any time hereafter regardless of their initial position(s) and views as stated in the Bleecker Street Research LLC’S research. One or more Bleecker Street Research LLC Related Persons have provided Bleecker Street Research LLC with publicly available information that Bleecker Street Research LLC has included in this report, following Bleecker Street Research LLC’S independent due diligence.

Research is not investment advice nor a recommendation or solicitation to buy securities. To the best of Bleecker Street Research LLC’s ability and belief, all information contained herein is accurate and reliable, and has been obtained from public sources we believe to be accurate and reliable, and who are not insiders or connected persons of the securities of a Covered Issuer or who may otherwise owe any fiduciary duty or duty of confidentiality to the Covered Issuer. However, such information is presented “as is,” without warranty of any kind – whether express or implied. Bleecker Street Research LLC makes no representation, express or implied, as to the accuracy, timeliness, or completeness of any such information or with regard to the results to be obtained from its use. Research may contain forward-looking statements, estimates, projections, and opinions with respect to among other things, certain accounting, legal, and regulatory issues the issuer faces and the potential impact of those issues on its future business, financial condition, and results of operations, as well as more generally, the issuer’s anticipated operating performance, access to capital markets, market conditions, assets, and liabilities. Such statements, estimates, projections, and opinions may prove to be substantially inaccurate and are inherently subject to significant risks and uncertainties beyond Bleecker Street Research LLC’s control. All expressions of opinion are subject to change without notice, and Bleecker Street Research LLC does not undertake to update or supplement this report or any of the information contained herein. You agree that the information on this website is copyrighted, and you, therefore, agree not to distribute this information (whether the downloaded file, copies/images/reproductions, or the link to these files) in any manner other than by providing the following link: Bleecker Street Research LLC bleeckerstreetresearch.com The failure of Bleecker Street Research LLC to exercise or enforce any right or provision of these Terms of Service shall not constitute a waiver of this right or provision. If any provision of these Terms of Service is found by a court of competent jurisdiction to be invalid, the parties nevertheless agree that the court should endeavor to give effect to the parties intentions as reflected in the provision and rule that the other provisions of these Terms of Service remain in full force and effect, in particular as to this governing law and jurisdiction provision. You agree that regardless of any statute or law to the contrary, any claim or cause of action arising out of or related to the use of this website or the material herein must be filed within one (1) year after such claim or cause of action arose or be forever barred.

Bleecker Street Research LLC Related Person is defined as: Bleecker Street Research LLC and its affiliates and related parties, including, but not limited to, any principals, officers, directors, employees, members, clients, investors, Bleecker Street Research LLCs, and agents.