Cellceutix (CTIX): A December To Remember May Turn Into A 2015 To Forget

CTIX has made numerous misleading statements in the past.

CTIX has been promoted by an unregulated Swedish entity.

CTIX is burning around $5M cash per quarter and only has $7M in cash on hand from the most recent quarter.

December to remember may turn into an 2015 to forget for Cellceutix investors who have been enjoying a run-up in the stock price on the back of several promotional press releases. "Cellceutix expects December to be a momentous month in its history," read one press release on November 24th, 2014.

A series of events have helped propel CTIX shares to a $500 million valuation. Investors and traders would be wise to look deeper than these recent events into this company's history.

Cellceutix (CTIX) entered the market through a reverse-merger with a company called Econoshare, Inc. In December 2007, the company acquired Cellceutix Pharma, Inc. which was a privately owned Delaware company that was incorporated just six months prior to being acquired. Between its incorporation in July and the reverse merger in December 2007, Cellceutix Pharma acquired the rights to six pharmaceutical compounds. The company said at the time that it would spend the majority of its time and resources on Kevetrin. According to the filing:

The Company will initially spend most of its efforts and resources on its anti-cancer compound, Kevetrin, for the treatment of head and neck cancers. This compound is furthest along in in-vivo studies in small animals. Based on the results, the Company has decided to advance it along the regulatory and clinical pathway.

Since then CTIX has added several other drugs to its pipeline. From a recent presentation, these are CTIX's drugs.

Brilacidin

CTIX acquired Brilacidin out of bankruptcy from PolyMedix. Here is the press release announcing the deal. CTIX paid $2.1 million in cash and included 1.4 million shares in the deal. At the time CTIX was trading around $2/ share, bringing the total acquisition price to $4.9 million. In the press release, CTIX said:

This is a transformational development for our Company and shareholders; adding the assets of PolyMedix for a tiny fraction of what we believe the company is truly worth," said Leo Ehrlich, Chief Executive Officer at Cellceutix. "We are very excited about instantly having a strong antibiotic franchise to complement our already robust pipeline that now contains 18 compounds. We intend to quickly advance Brilacidin into a Phase 2b clinical trial, a drug that we believe could one day compete with drugs like Pfizer's Zyvox, which generated $1.35 billion in sales in 2012. The acquisition, which includes laboratory equipment and other furnishings that we are confident cost in excess of $1 million, makes us an even more formidable company.

In the press release, CTIX touted that they were also acquiring laboratory equipment and other furnishings, in which they were "confident cost in excess of $1 million." While that may be technically true, it is somewhat misleading. It doesn't matter how much PolyMedix paid for the assets, because CTIX's press release does not take into account depreciation, a very real cost for medical and laboratory equipment. According to the last 10-Q filed by PolyMedix before CTIX acquired PolyMedix had $749,000 in "Office furniture and lab equipment" as of September 30, 2012.

And since CTIX acquired these assets almost an entire year later, this does not factor that additional depreciation. PolyMedix's accounts show accumulated depreciation of $1.2 million, meaning that PolyMedix did indeed cost more than $1 million, but again what it cost does not matter as much as what the equipment is worth after depreciation. I believe it is misleading for CTIX to reference the dollar amount that the assets cost originally and not what PolyMedix thought they were worth in their last 10-Q.

In a more recent presentation from a Rodman and Renshaw event, CTIX continued with the somewhat misleading statements about PolyMedix and that deal. Below is the slide which I believe is misleading.

First of all, the slide says that "Cellceutix Acquired PolyMedix." This is not true. Cellceutix acquired the assets of PolyMedix out of bankruptcy. But it sounds better to say that you acquired another company instead of saying you acquired the assets from a failed company. The press release that CTIX issued at the time tells the true story: "Cellceutix Acquires PolyMedix Assets From Bankruptcy Court, Gains Ownership of Two Clinical Stage Drugs, Multiple Compounds, and Equipment Assets."

And then CTIX seems to try to suggest that they acquired a company with a $227 million market cap, but wait - that was before bankruptcy. And also that the company had and an "Outperform rating." An outperform rating does not mean anything. CTIX tries to sweep under the rug that they bought the assets from a failed company for $4.9 million and try to make it look like they acquired a much larger and successful biotech company.

Kevetrin

Kevetrin is CTIX's anti-cancer drug. According to CTIX, Kevetrin has "consistently shown activity as good or better than standard chemotherapeutic therapies, given at approximately equitoxic doses. Kevetrin has demonstrated potent anti-tumor efficacy against various carcinoma xenograft models: lung, breast, colon, prostate and squamous cell carcinoma, and in a leukemia tumor model." This is an overview of the drug from a slide from CTIX's presentation at the Rodman & Renshaw conference this past September.

Source: CTIX Website

On January 20th, CTIX put out a press release claiming that a spleen lesion disappeared in a patient with Stage 4 Ovarian Cancer on a CTIX clinical trial. The press release read:

Cellceutix Reports Spleen Lesion 'Disappears' in Patient With Metastatic Stage 4 Ovarian Cancer in Clinical Trial of Anti-Cancer Drug Kevetrin

CTIX stock went up nearly 25% that day as traders and investors were enamored with the headline. The press release continued, saying:

[CTIX] is pleased to report the near complete disappearance of a metastatic lesion in the spleen of a Stage 4 ovarian cancer patient who was enrolled in the Company's Phase 1 clinical trial of anti-cancer drug candidate Kevetrin™ being conducted at Harvard Cancer Center's Dana-Farber Cancer Institute and Beth Israel Deaconess Medical Center. According to information supplied by the hospital, the patient, who successfully completed three Kevetrin 3-dose cycles before discontinuing the trial, experienced increased energy, while scans showed a reduction in the amount of peritoneal fluid (ascites) during treatment with Kevetrin. Subsequent to the second and third Kevetrin cycles, scans showed the spleen lesion to be essentially undetectable and the patient's disease to be clinically stable."

So CTIX's star patient has actually dropped out of the trial. I contacted Cellceutix about this and promptly received a response from Mr. Ehrlich. He cited the press release, saying:

The patients in our trial are incredibly sick, have often run the gamut of approved treatments and subject to constant therapy modification to address the greatest area of need at the given moment. That's an everyday practice in oncology, especially when a drug regimen, such as the strict protocol with the Kevetrin trial where dosing levels and intervals absolutely cannot be changed. We are not privy to the minutiae underscoring any physician's decisions in a trial, but we interpret the stabilization of the cancer as allotting the physician an opportunity to modify treatment to improve the patient's quality of life, an opportunity that potentially may have not been there without Kevetrin."

The Stock Promotion

I found some evidence of potentially fraudulent firms engaging in the promotion of CTIX stock in 2014. It is important to note that I found no connection between these entities and the company, however, I still believe it is a red flag. In January of 2014, the Swedish Finansinspektionen (the Swedish Financial Supervisory Authority) put out a warning to investors about dealing with unregulated firms. The company in question here is Dyman Associates, which according to their very vague description on their website, "is a Merger and Acquisition Advisory Firm that has been dealing with middle-sized organizations for numerous years in the acquisition and purchase of various businesses."

This note accused Dyman Associates of not being authorized and specifically mentioned Cellceutix as a company that Dyman was promoting through phone calls.

Dyman Associates has not received authorisation from Finansinspektionen and therefore is not entitled to provide financial services in Sweden. Finansinspektionen has not received any notification of cross-border activities from other EEA countries.

Representatives from Dyman Associates contact Swedish investors through unsolicited telephone calls and offer them to buy holdings of shares in a American OTC companies such as Cellceutix.

History of Management

An article that originally appeared in INDIA New England raised questions about some of the claims that CTIX President Krishna Menon had exaggerated some of his past. This article by "Pump Terminator" on NNVC, where Mr. Ehrlich was CFO from 2005 to 2007, made some interesting observations.

"routine fact-checking by INDIA New England soon revealed that the story of Krishna Menon contained many false claims and exaggerations" - India New England Article

We noticed this story was no longer on India New England's website and some claim it was taken down because it was false. We called India New England and here is what we were told about the article's accuracy: "All entirely true, no question. The only reason we took it down is the editor is no longer with us and this story caused quite a stir, and we grew tired of all the phone calls when the editor who wrote it doesn't even work here anymore."

I contacted Mr. Ehrlich about this and his response was that the story was removed from the website and that should cause one to be more skeptical of it, which is a fair point. Although it would appear that Pump Terminator has contacted INDIA New England and that they still stand by the story. Mr. Ehrlich also highlighted that since the article appeared, CTIX has risen 10 times.

The same article from Pump Terminator also highlighted several other discrepancies.

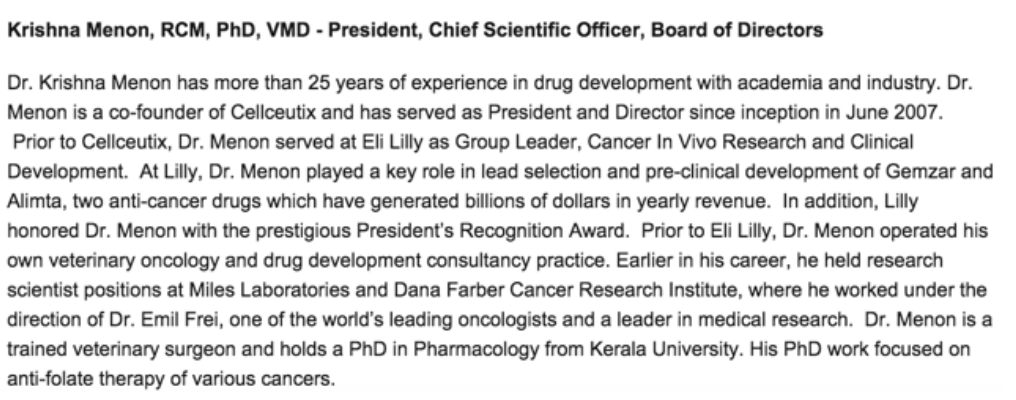

Amazingly we found even more examples of conflicts in what Menon has publicly said. In his NNVC management biography he claims "a PhD in Pharmacology in 1984 from Harvard University2" and yet in the CTIX management biography (where he is President) he claims "a PhD in Pharmacology from Kerala University3". We don't see how Menon can be telling the truth in both statements.

Note: The links from the Pump Terminator article now lead to different pages but here is a screenshot from the NNVC website accessed via the Wayback Machine that shows Dr. Menon saying that he received his PhD from Harvard University.

And then here is Dr. Menon saying he received his PhD from Kerala University, from the CTIX website.

Summary

CTIX has been burning about $5 million in cash a quarter and with only $7 million in cash as the last 10-Q, I don't see how CTIX can last much longer without doing a dilutive capital raise. That, combined with all the other issues, could make 2015 a year to forget for CTIX shareholders.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.